2021 Midcon Update

2021 Midcon Update

(Important Disclaimer at Bottom)

Strength at Conway

Bison released our first white paper on the mid-continent region in November 2020, in which we shared our observations and analysis on the shifting local supply dynamic and the likely sustainability of improved local pricing. Our publication of this report raised some questions, as we are a value focused investment fund, not a macro research shop. However, this research was pivotal in the multi-hundred percent return for an investment we made in Sandridge, which was heavily exposed to the area. And we shared that investment thesisaround the same time as we shared our white paper.

In the first midcon white paper, we observed that falling production and inventory had caused a supply shift at the Conway Hub, Kansas: the hub was becoming undersupplied and local realized prices were rising. And our analysis indicated that the rising local price trend would continue. In the time since, regional and local prices for NGLs have risen, supported by these improved fundamentals. And last week, we saw U.S. wholesale propane prices at Conway rise to a 6-year high, breaking 100 cents per gallon.1

Source: @JavierBlas

Before we dive into the details behind this recent price surge and our outlook for the year ahead, we’d like to draw attention to how remarkable the gains at Conway Hub are. Conway prices in January 2020 were at 39.75 cents, before falling to 20.5 cents near the beginning of the pandemic.(2) On November 3rd, the day we posted our midcon white paper, the Conway prices were at 53 cents. Fast forward to last Wednesday (January 20th, 2021) where the price of propane at Conway surged to 98 cents, a 45-cent (or nearly 85%) increase from November 3rd.

While Conway prices did not remain at a premium to Mont Belvieu for long, it is impressive that the Conway-Belvieu spread remained relatively tight throughout this rally (between 2 and 4 cents). Both hubs saw their prices hovering in the 45-55 cent-range for months, before both steadily climbed to above 85 cents over the course of December 2020. These gains were material, especially for companies exposed to this uplift in local natural gas and NGL pricing (see: Sandridge Trounces Market). While we saw the early signs leading to the local strength in pricing, we did not expect the rare combination of supply-side factors that caused the more recent supply crunch.

A Bullish Environment

We can look to a few main factors responsible for the increase in prices recently, according to LPGas magazine.(3,4) While some of these factors have individually contributed to the strength in Conway pricing over the last few months, the simultaneous occurrence of these forces led to the more recent price surge:

1. Rise in Crude Prices: Historically, the price of propane at Conway tracks with crude oil prices, and crude has risen from $36.00 to $53.30 between November 2020 and now. This is a $16.80 increase in price, or a 46% increase. While the gain in crude is one proponent of the recent strength at Conway, propane has far outpaced crude’s gains in the last month. This would indicate propane prices are getting more support from their own fundamentals, which brings us to…

2. Propane Exports and Strong Interest from Asia: The most impactful support for propane fundamentals comes from strong exports this winter. According to LPGas, propane exports have averaged 71,000 barrels per day (bpd) more for 2020 than in 2019. For the fourth quarter of 2020, propane exports averaged 137,000 bpd higher than in the same period in 2019.(4) A key factor in export demand this winter season has been very strong interest from foreign buyers, amidst the recently developing Asian energy supply crisis and spiking JKM prices. The Far East market was at $1.21 per gallon or a 43-cents-per-gallon premium to Mont Belvieu LST in early January.(5) This large premium has kept export economics favorable and as long as export demand remains strong, there is likely to be continued pressure on inventory and support for propane prices.

3. Crude Inventory Decline: The EIA releases weekly updates on U.S. oil and gas inventory and reported a 6.729 million-barrel draw on U.S. propane inventory in its most recent release. This draw eclipses the five-year average draw of 1.4 million barrels for the first week of the year and far exceeded industry expectations of a 4.13-million-barrel draw.(6) After the draw, U.S. propane inventory was at 15.756 million barrels (or 19.3%) below where it was at the end of week one last year.

Production Decline

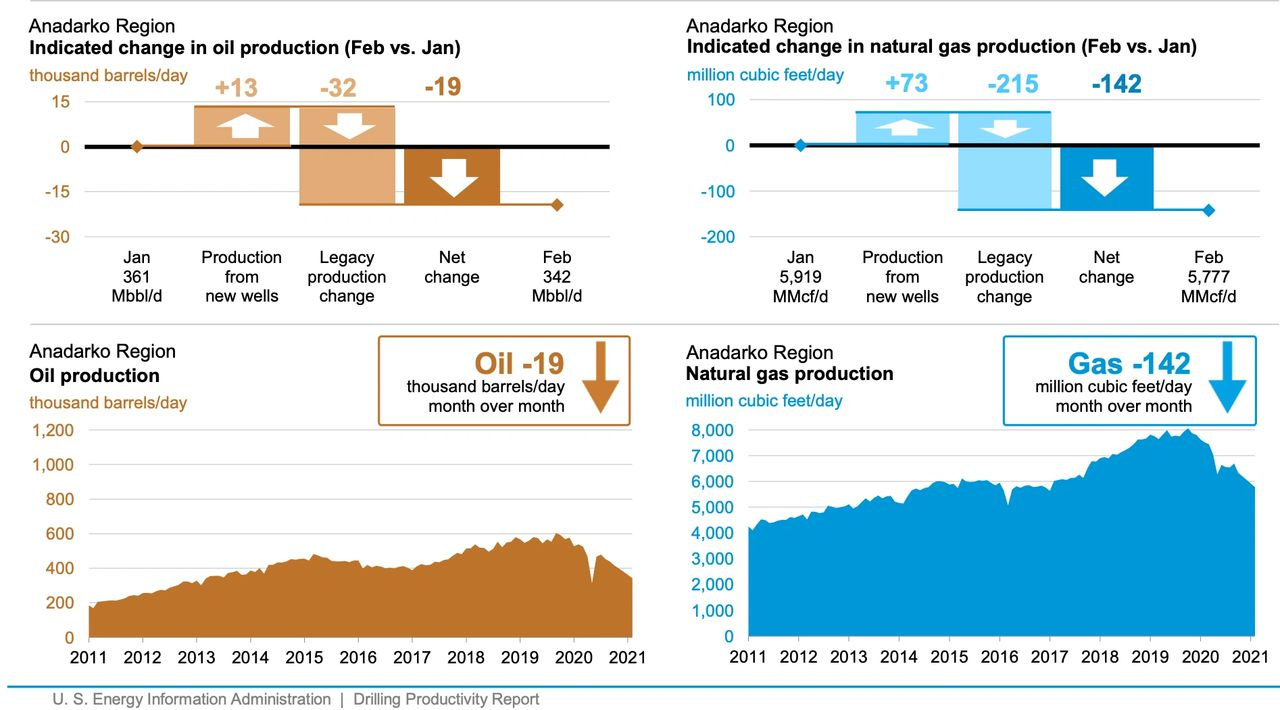

The broader outlook for midcon supply is not optimistic either. Since our update in November, production levels fell further below 2020’s fourth quarter levels. According to the EIA, Anadarko region oil production for January 2021 is estimated at 361 thousand barrels per day (Mbbl/d), and is forecast to fall in February 2021 to 342 Mbbl/d. This is below November 2020’s production of 404 Mbbl/d and materially below 2020’s peak. In terms of Anadarko natural gas production, there is an expected drop of 142 million cubic ft per day from 5.9 Bcf/d in January to 5.7 Bcf/d in February.

Forecasts indicate that production will not materially increase in the region this year, and this trend could continue into 2022. Our view is that prices have not been high enough to justify investment in sustaining production levels. Pioneer Natural Resources CEO Scott Sheffield agrees, stating “the Permian could add 100,000 or 200,000 b/d per year, but the rest of the U.S. is going to decline,” citing Oklahoma’s SCOOP/STACK plays and the Niobrara-DJ Basin, among others as declining.(7) Mr. Sheffield stated he expects U.S. crude oil production to remain relatively flat near 11 million b/d for years to come with any upticks in Permian Basin output coming at the expense of other shale basins.

Outlook and Price Forecast

The factors we outlined above as they relate to production are expected to continue until stronger prices support investment returning to the region. While the winter season is coming to an end soon, energy demand remains on a cautiously optimistic trend as widespread vaccinations campaigns continue, business activity and travel demand returns. Propane exports are forecast to grow in 2021 but at a less intense pace, according to the EIA.

While prices may not sustain at current levels, forecasts expect 2021 to be a strong year for natural gas and NGL markets. According to the EIA’s Jan 2021 Short Term Energy Outlook, EIA forecasts the Henry Hub price will increase from $2.00 per million British thermal units (MMBtu) in 2020 to $3.01/MMBtu in 2021 and to $3.27/MMBtu in 2022. We can expect higher crude oil prices in early 2021 as well, driven by inventory draws and stronger natural gas prices throughout this year. CME futures for Conway and Mont Belvieu are stronger than what we saw in the second half of 2020 as well.

Source: CME (1/21/2021)

Conclusion

The latest price surge at Conway and the midcon region can be attributed to the effects of three major supply-side shifts: the amount of natural gas production, levels of natural gas in storage, and volumes of natural gas imported and exported. The EIA wrote that “because of natural gas supply infrastructure constraints and limitations in the ability of many natural gas consumers to switch fuels quickly, short-term increases in demand and/or reductions in supply may cause large changes in natural gas prices, especially during the wintertime.”(8) While this may explain short term price movements such as the recent Conway propane price move, fundamental shifts have led to our more bullish outlook over the next couple of years.

That said, the Biden-Harris presidential transition has introduced additional regulatory risk and uncertainty to our outlook. The Biden administration recently announced it is temporarily blocking any new leasing or drilling permits on U.S. federal lands for 60 days.(9) Based on historical precedent, we expect this is the first but not the last measure from the new administration to restrict drilling on federal lands. Additional executive orders and regulations could add more severe restrictions. Companies in the industry with significant amounts of federal acreage exposure are EOG (EOG), Exxon (XOM), Murphy (MUR), Devon (DVN), and Occidental (OXY). This is relevant to midcon because additional federal land drilling regulations, restrictions, or bans could shift drilling away from federal lands to mid-continent oil and gas fields.

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Sources:

https://www.lpgasmagazine.com/fundamentals-point-to-higher-propane-prices-this-winter/

https://www.lpgasmagazine.com/fundamentals-point-to-higher-propane-prices-this-winter/

https://www.lpgasmagazine.com/propane-prices-on-a-rally-this-winter/

https://www.lpgasmagazine.com/fundamentals-point-to-higher-propane-prices-this-winter/

https://www.eia.gov/energyexplained/natural-gas/factors-affecting-natural-gas-prices.php

https://www.lpgasmagazine.com/protecting-margins-when-propane-prices-rise-rapidly/