2022 Oil Outlook & DUC Dilemma

2022 Oil Outlook & DUC Dilemma

(Important Disclaimer at the Bottom)

2022 is looking promising for the oil and gas industry on several fronts. Un-economic “ESG” mandates by investment allocators and increasingly unfriendly policy and regulations are restricting the availability of capital and suppressing development activity. Insufficient exploration and production activity is depleting reserves. And despite the prevailing “green transition” narrative, demand continues to rise inexorably. Ironically, divestment and virtue signalling policymaking has intensified at a time where an energy crisis of epic proportions is already well underway, with natural gas prices in Europe sitting near $200 / barrel of oil equivalent after briefly running higher than $350!

The effects of all-time high gas prices in Europe, Asia and elsewhere are reverberating across the globe. Mandated blackouts have already been seen in Kosovo and parts of China, and various other cities like Berlin have seen spontaneous blackouts. And fertilizer and other energy intensive product production is being curtailed, despite the critical role fertilizers play in the food chain and the modern economy.

As Bison has previously discussed, natural gas used to produce ammonia—a primary input for fertilizer used to grow crops—and so higher prices drive food inflation. Ammonia factories in Europe are shutting-in now unprofitable operations, and farmers are delaying fertilizer purchases, which is driving down food production [1]. Few appreciate this, and in conjunction with pandemic-related global supply chain disruptions, the situation may worsen.

Gas prices have gone so high that LNG cargoes are now being diverted away from Asia towards Europe, which is likely to exacerbate the situation in the gas-hungry eastern hemisphere:

While industry bears and pundits had cited bountiful OPEC+ spare capacity as the potential cure to the energy crisis in Europe, it is becoming abundantly clear that said spare capacity is markedly lower than advertised, and so the world can’t look to OPEC+ to solve the supply crisis. Bison was early to make this call in September last year, and despite major pushback, this view is slowly seeing broader acceptance.

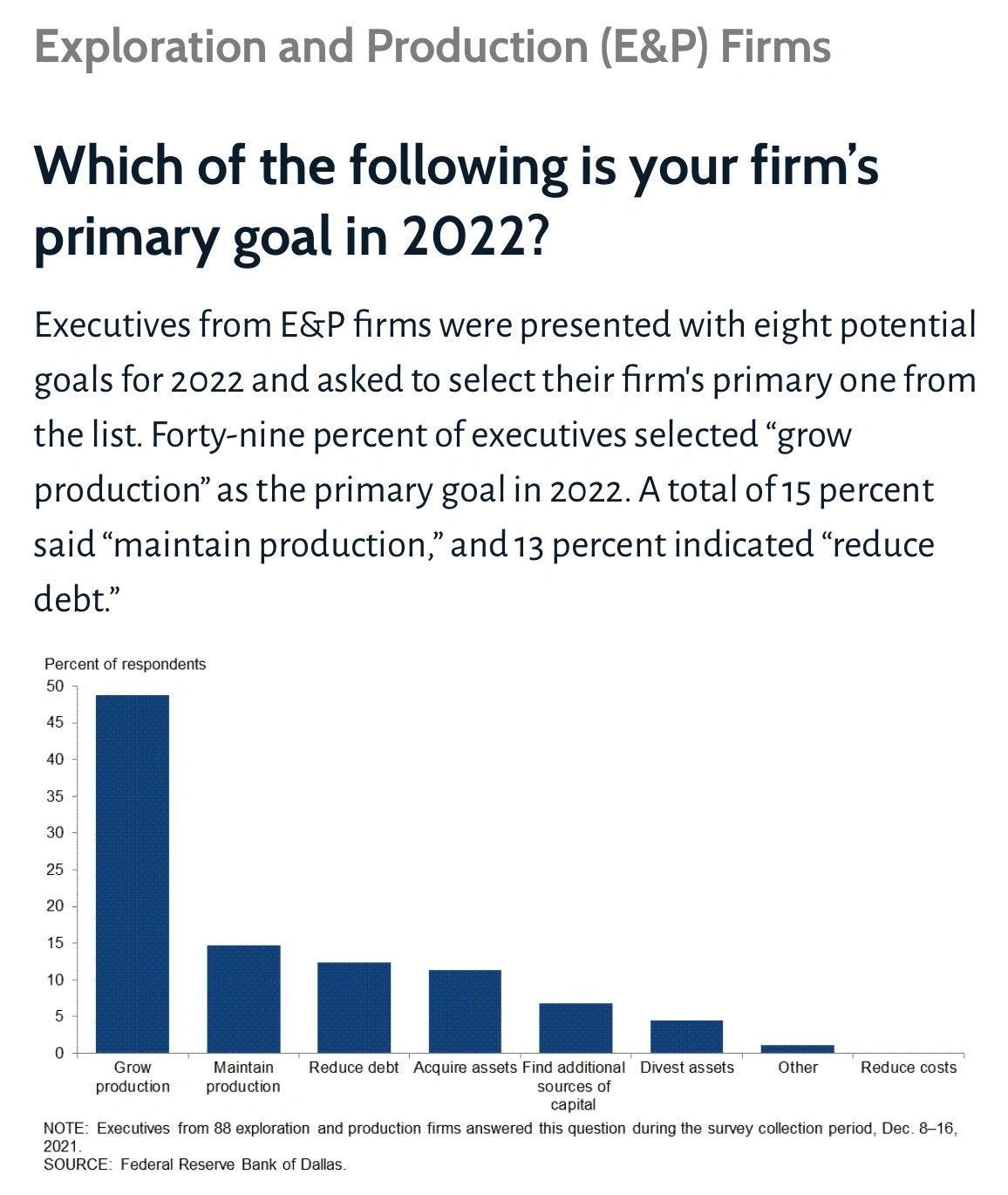

These factors, combined with lower/declining production growth and structurally higher oil demand, are promising contributors to even higher oil prices in 2022 and beyond. Narrative and sentiment are following price, with oil and gas company management teams warming up to the idea of new drilling in 2022:

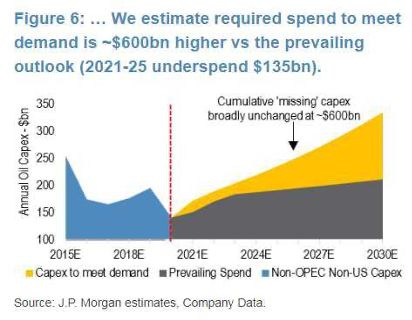

While historically this would galvanize new production and eventually lower prices, the scale and duration of under-investment may now require years of much higher activity to be resolved, and there is limited capital availability due to ESG-driven divestment. Oil directed capital investment worldwide has been too low for years now, and the higher oil prices and much higher world natural gas prices we’re seeing may be an early manifestation of a much larger issue:

Aside from OPEC+ and international non-OPEC production issues, US production is unlikely to recover to pre-pandemic levels without substantially higher levels of drilling and development activity. A major factor is the “DUC Dilemma,” which we address below.

The DUC Dilemma: Diminishing Inventory is an Underappreciated Risk to Oil Production

With oil fundamentals strong and prices rising, US oil production recovery challenges remain under-appreciated. Drilling activity remains low versus 2019 levels, and even lower versus pre-2014 oil crash levels. The industry has also seen substantial turnover of highly skilled and experienced labor, coming after numerous rounds of layoffs in 2014 onwards. Industry veterans are becoming increasingly hard to replace, particularly as the oil and gas industry falls out of favor with new college graduates and an aging workforce retires:

With comparatively few new wells being drilled, the inventory of drilled uncompleted wells (DUCs) is being rapidly depleted as the industry compresses working capital to meet higher-than-expected post-pandemic demand with proportionately smaller budgets. A steady inventory of DUCs is necessary to maintain output over time; in the current environment, this inventory simply isn’t being replenished fast enough.

DUCs exist because a shale well is brought onto production in two distinct phases, each requiring different specialized crews and equipment (pardon the simplification): 1) the well is first drilled using a drilling rig, and 2) the well is then stimulated to production, or “completed,” using a frac spread. A DUC is a well that has been drilled but has not yet been completed (thus the DUC acronym: Drilled Un-Completed). When the rate of drilling outpaced completions, DUC inventories rise; and conversely, when completions outpace drilling, they draw down. Since the onset of the pandemic, well completions have raced ahead of new drills, and DUC inventory has been rapidly depleted. Note the pace of drilling vs completions below:

Availability of Capital & DUC Inventory

DUC inventory levels are inextricably linked to industry capital cycles. When capital is abundant producers tend to boost investment and increase drilling relative to completions, and so DUC inventory rises. When capital is scarce producers prioritize well completion over new drilling, allowing them to maintain production levels with less capital – so long as there are DUCs left to be completed.

In the aftermath of the oil price shock from the initial wave of Covid lock-downs and the Saudi/Russian oil price war, E&P’s have been exercising capital discipline. Accordingly, the cash flow generated in this high-price environment has largely been used to fund debt paydown, dividends and share repurchases, rather than investments in new development.

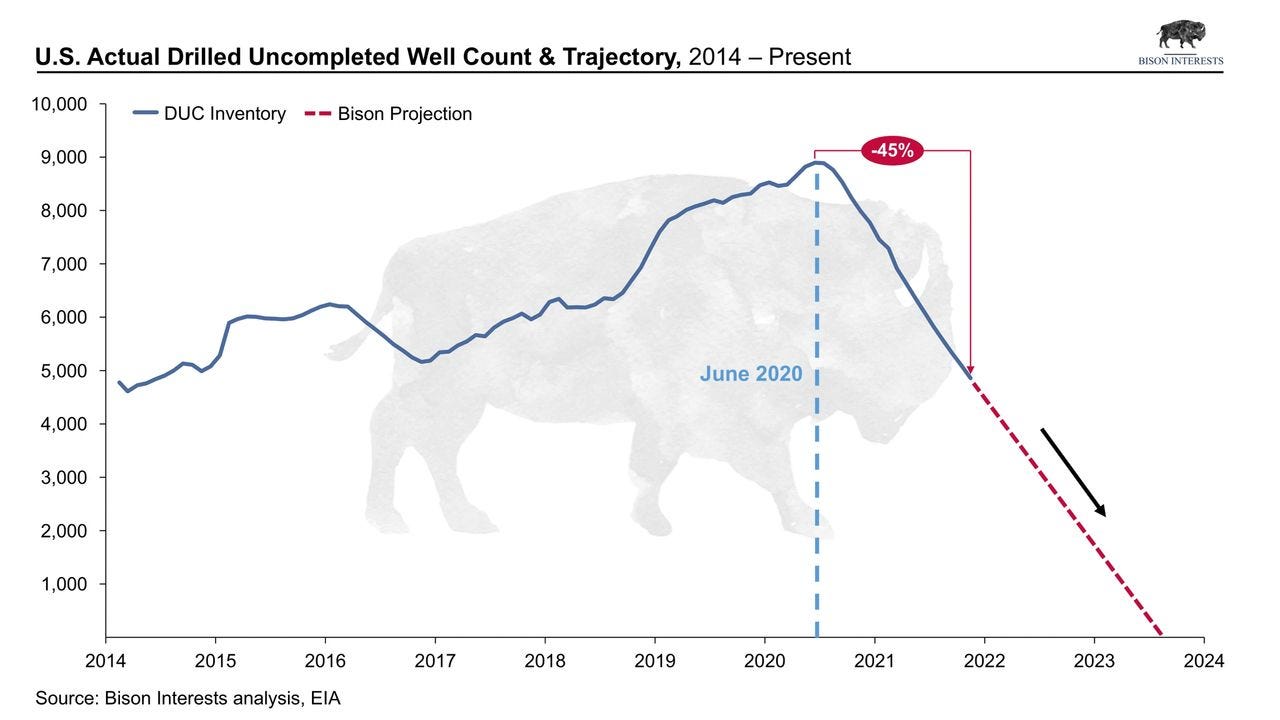

Production has been able to rise modestly since pandemic lows despite this capital discipline because producers have been able to complete wells they had previously drilled. Consequently, DUC inventory in the US has fallen dramatically, and without substantially increased drilling, the inventory of DUCs may reach dangerously low levels by mid-2023:

US oil production may grow less than expected as the industry depletes its inventory buffer and loses flexibility to increase production in response to rising demand. This simple shift from drilling to completion is obviously unsustainable, and absent a material change, may result in disappointing production and higher prices.

Compounding problems for producers, DUC inventory shortages may actually be worse than reported. Historically, 95% of wells drilled have been completed within 2 years; DUCs older than 2 years are considered “dead” and the probability they are completed falls drastically [2]. The inventory of live DUCs likely to be completed is likely overreported, as most conventional sources fail to make this important distinction:

Shale Dynamics & The Importance of DUC Inventory

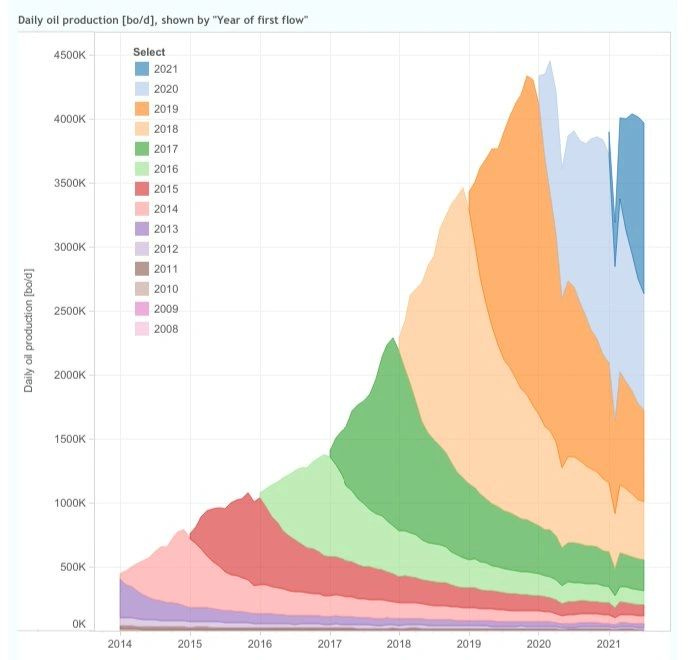

DUCs are a form of oilfield working capital. A steady supply of DUCs is needed to maintain and grow production levels, avoid operational delays, and importantly, to offset production declines from existing wells. This is particularly true for US tight oil plays, which tend to reach peak production exhibit steep declines in production within the first year, as illustrated in this chart showing annual shale production “wedges:”

Source: Shale Profile

Unconventional wells in the most prolific shale plays tend to exhibit a 70% decline in the first year of production and another 30% in their second year. On average, it takes 8-10 years for decline rates to level off around 10% [3]. Over 70% of US oil production comes from this steep, rapid production decline shale, implying that substantial drilling activity is necessary just to hold production flat, let alone grow output [4]. In the context of these high annual decline rates, the current rapid pace of depletion of DUC inventory is unsustainable. Absent a reversal soon, US oil production growth could stall out, and production could fall.

Drilling Rigs and Frac Spreads: Equipment Levels as a Leading Indicator of Inventory

The supply of rigs and frac spreads used for well drilling and completion can be a leading indicator of DUC inventory changes. Because frac spreads complete wells faster than rigs can drill them, there is an optimal equipment ratio needed to maintain a steady level of DUC inventory. While over the last 5 years this ratio has averaged 0.47, it currently sits at 0.53 as the frac spread count has increased relative to rigs, which coincides with the post-pandemic period in which DUC inventory has been falling:

How Does This Get Resolved?

Because the ratio of drilling rigs to frac spreads is good predictor of changes in DUC inventory, we sought to determine how many rigs would need to be added, or conversely, how many frac spreads would need to be removed, to keep DUC inventories from falling. We ran this analysis using two calculation methods, and we present our methodology and findings below:

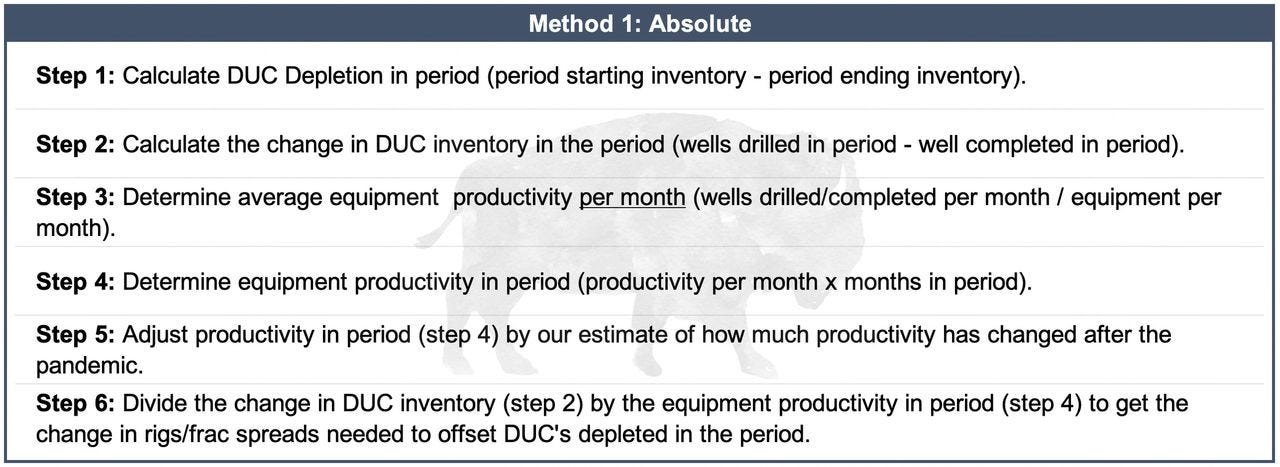

Method 1: Absolute

The objective of this analysis was to determine how many rigs/frac spreads would need to be added/removed to replace DUCs depleted over the time period examined. The steps of this analysis are outlined below:

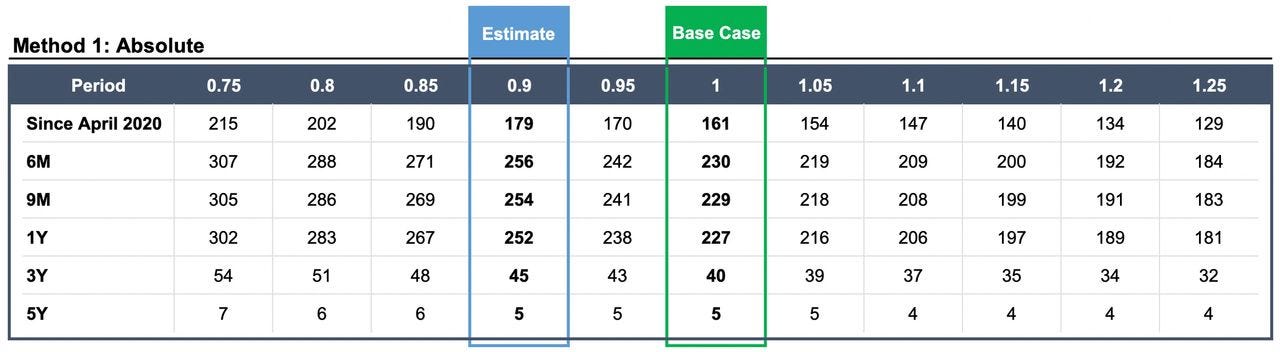

After conducting this analysis, in which we assumed rig productivity has declined 10% after the pandemic, we estimate that the industry would need to add ∼180 rigs or remove ∼45 frac spreads to restore DUCs depleted since April 2020:

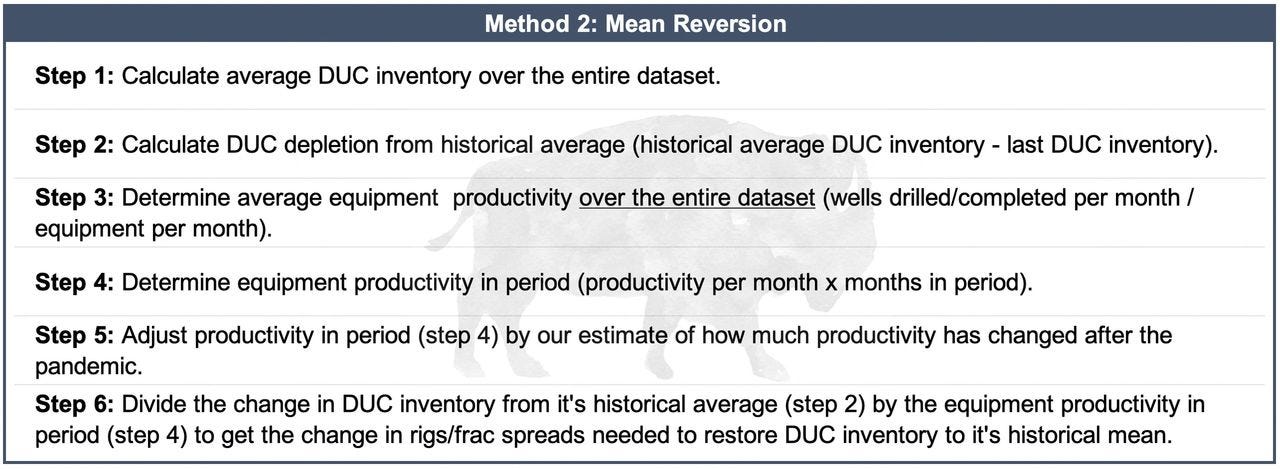

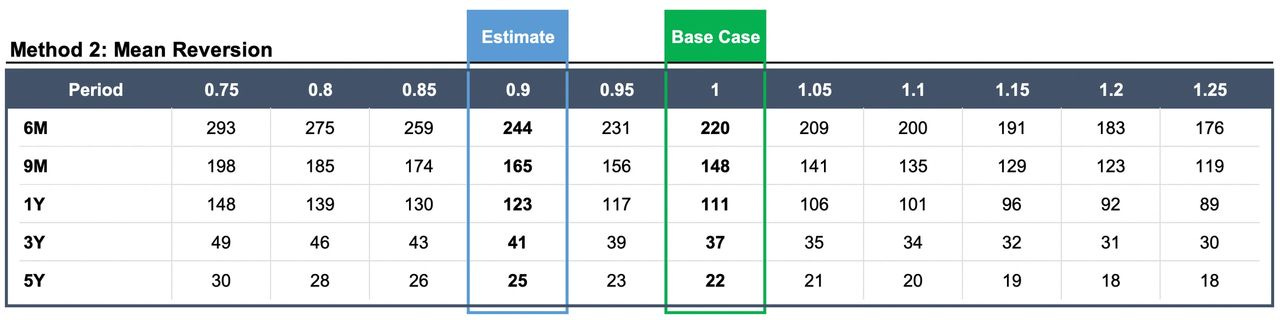

Method 2: Mean Reversion

In this analysis, we determine how many rigs and/or frac spreads need to be added or removed to flatten DUCs depleted from their historical mean within the time period in question. Intuitively, if we wanted to flatten DUCs within a shorter time period, we would need to add/remove more pieces of equipment. The steps of this method are outlined below:

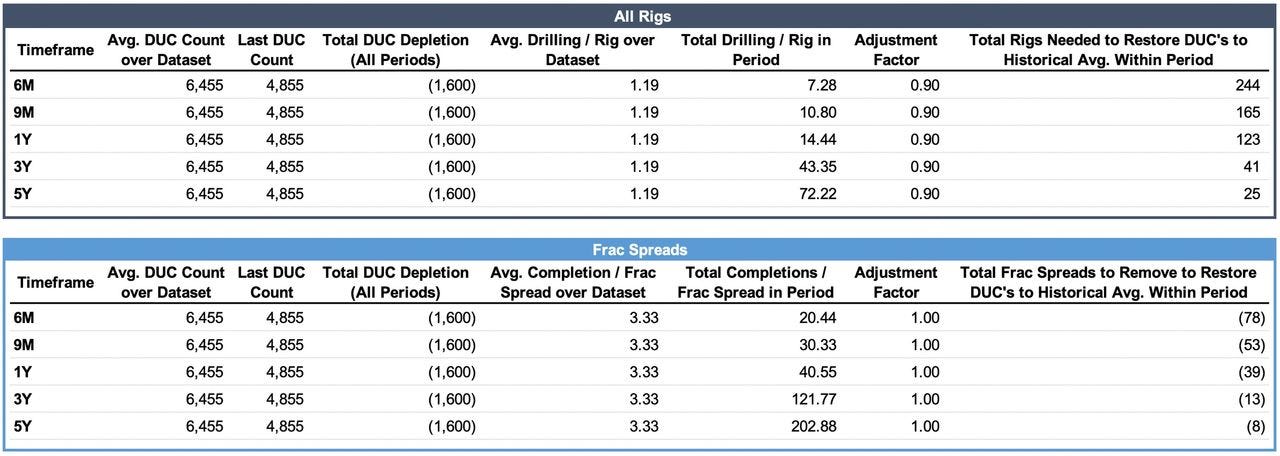

After conducting this analysis, we estimate that the industry would need to add ∼240 rigs within or remove ∼80 frac spreads within one year to flatten DUC inventory to its historical average of 6455.

Sensitivities to Adjustment Factors

These analyses required us to make assumptions about the relative productivity of new rigs being brought online. We have reason to believe that new rigs being added are not as productive as already operating rigs, due to lead time to ramp up activity and “green” crews lacking training and experience. To maintain conservatism, we assumed new rigs would be 10% less productive than existing ones, although this figure may be overly optimistic. We ran a sensitivity analysis to see how our estimate would change at different levels of assumed productivity:

Implications & 2022 Outlook

This total number of rigs required to keep DUC inventory from falling under both methods is a material increase over the existing total rig count, which currently sits at 588 as of January 2022 [5]. This has meaningful implications for likely US production, as there is substantial lead time needed for rigs to be refurbished and/or re-activated, transported to the appropriate well pad and to then begin drilling. Additionally, severe labor and supply shortages may exacerbate the problem even if the equipment could otherwise be supplied on time. Ultimately, we anticipate that the rig count may not reach necessary levels for the reasons above, and almost certainly not in 2022. US production may continue to underwhelm expectations, potentially sending oil prices higher.

Sources

[1] Source: The Guardian

[2] Source: Journal of Petroleum Technology

[3] Source: Journal of Petroleum Technology

[4] Source: Reuters

[5] Source: Baker Hughes

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.