2023 Outlook & Buying The Seasonal Sale in Oil & Gas Equities

2023 Outlook & Buying The Seasonal Sale in Oil & Gas Equities

(Important Disclaimer at the Bottom)

Source: Twitter

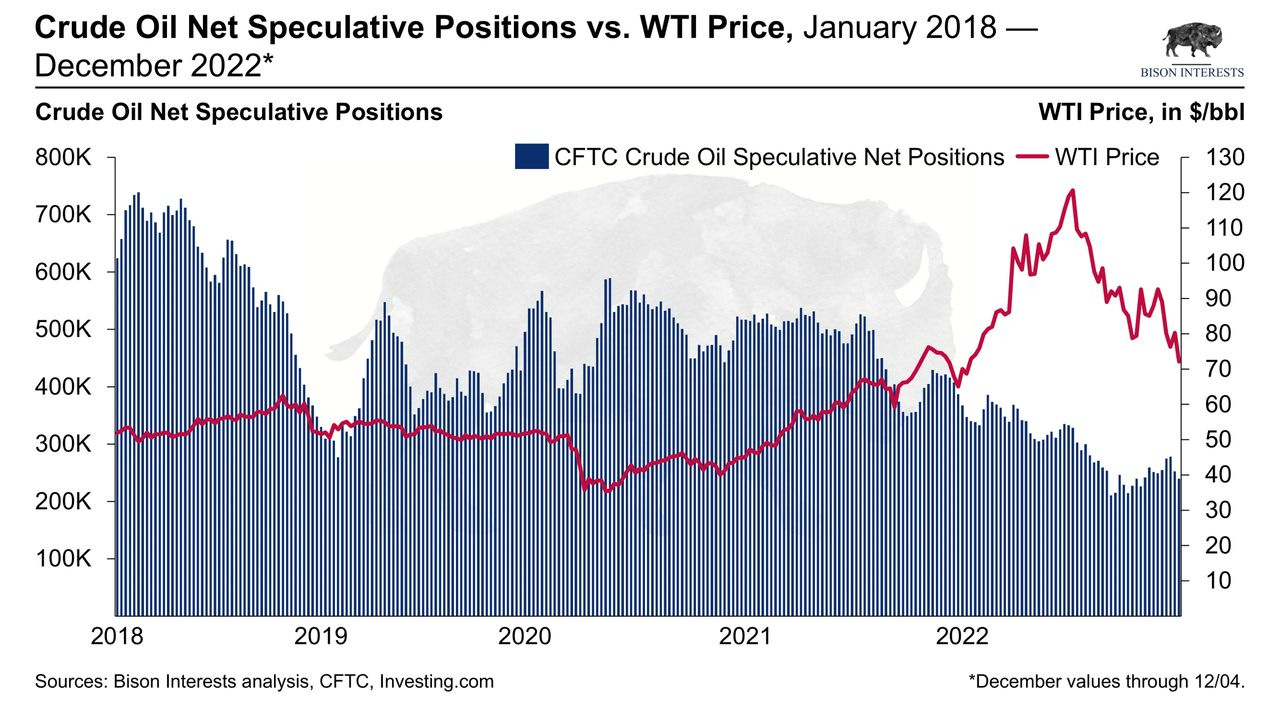

There’s been quite a selloff in oil the past few months. Ironically, many of the same market participants who were excited about oil and gas prices and equities this spring and summer have turned bearish—price drives narrative. Persistent negative coverage in the media and declining net interest in oil in the commodities futures markets illustrate this bearish sentiment:

As the volume and intensity of negativity increases—and is further reflected in the price of oil and associated equities—so does the potential for outsized investment returns. This move in oil may be overdone here, and the equities remain intrinsically cheap even at $70/bbl WTI. There are signs oil market fundamentals are improving despite falling prices: supply continues to languish, demand is rebounding, and inventory levels are low. This is a promising setup for oil prices and related equities to recover in 2023.

Bison 2023 Outlook

Supply

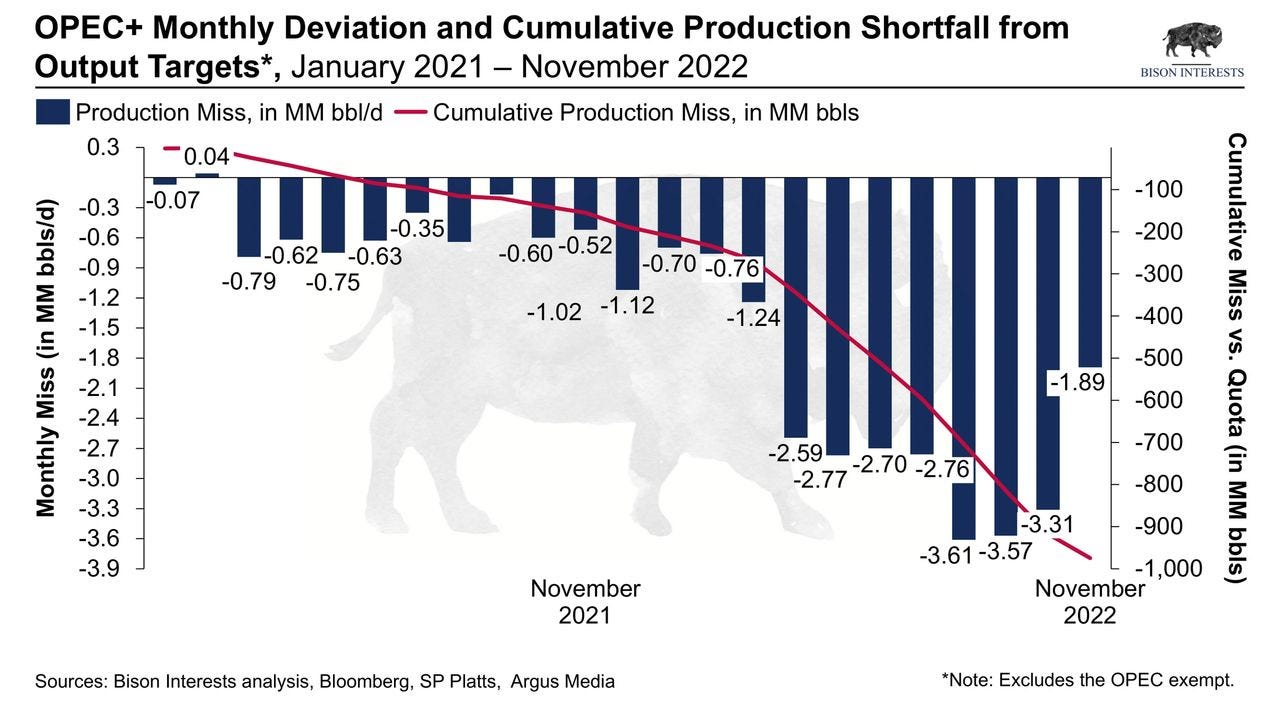

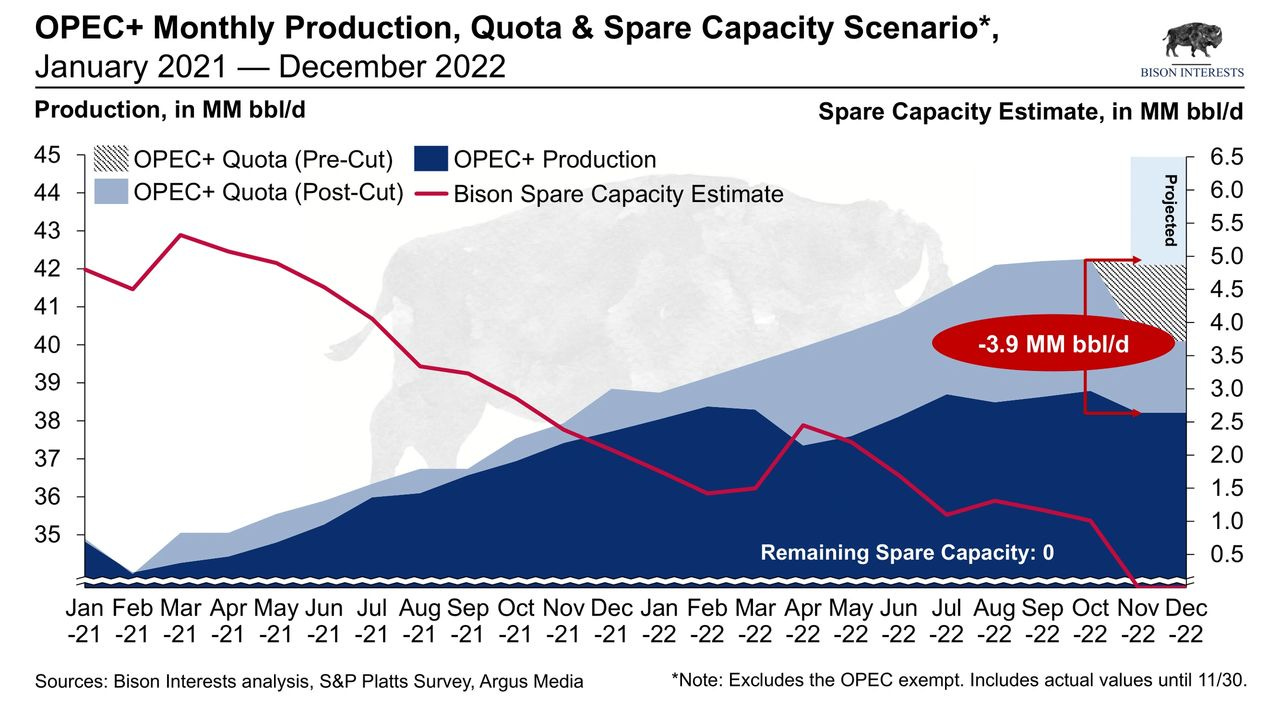

Oil supply is strained both in OPEC+ and non-OPEC countries. OPEC+ is nearly out of spare capacity, as we first predicted in September 2021. Many smaller OPEC+ producers have been struggling to meet production quotas for some time now, while output from the few producers who have some spare capacity may also be on the decline. In aggregate, OPEC+ has repeatedly missed its quotas for more than 2 years now—even after a 2MM bbl/d cut—and total OPEC+ total production levels may be topping out for now:

In consideration of these quota misses and lower global oil prices, OPEC+ may be incentivized to cut production further here—a move which could reverse the negative momentum in oil prices entirely on its own, absent a significant global economic downturn. And even if OPEC+ maintains its production quota, it is likely it will continue to struggle to meet it, which may result in a 3.9MM bbl/d market shortfall from pre-cut expectations:

Sanctions against Russia are also intensifying, which may curb its output in 2023. Insurance bans on Russian tankers carrying crude for EU firms, a price cap of $60/bbl on Russian oil, and outright bans on Russian crude imports to Europe have already come into effect, affecting more than two-thirds of Russian oil exports to the EU [1]. These may lead to declining exports for Russia despite some willing buyers in Asia. Reportedly, Russian crude exports fell by 0.5MM bbl/d so far in December, and with limited means to get its oil to market, analysts predict Russian output is likely to fall by 1.4MM bbl/d in 2023 [2].

North American oil production is also struggling to grow. Years of underinvestment in oil exploration, development, and infrastructure, driven by anti-fossil fuel policy and shifting investor preferences, have contributed to production growth below consensus expectations. This is aided by persistent shortages of labor, drilling rigs, and other oil field equipment critical to production.

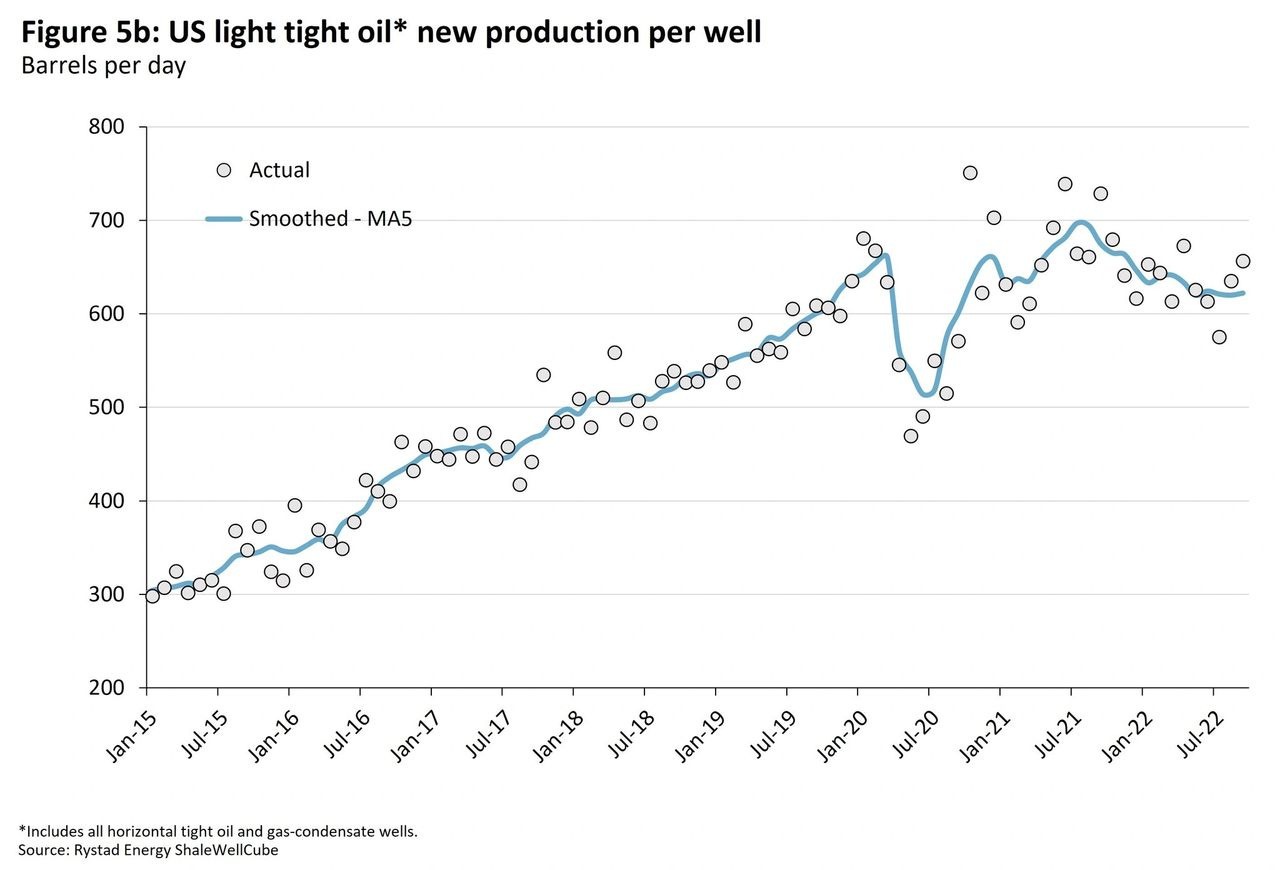

As a result of this underinvestment in production along with the depletion of the best wells, shale production in the U.S may struggle to exceed prior highs. U.S. shale will likely continue to deliver some incremental production, but may disappoint expectations as well productivity has been declining:

Demand

The most important near-term catalyst for oil is the lifting of Covid lockdowns in China that is currently underway. While it is notoriously difficult to predict policy decisions and paths (particularly in China), widespread demonstrations against China’s zero-Covid policy (and the dissemination of videos of these protests on notoriously tightly controlled Chinese social media) seem to have led to the removal of most Covid testing and quarantine requirements [3].

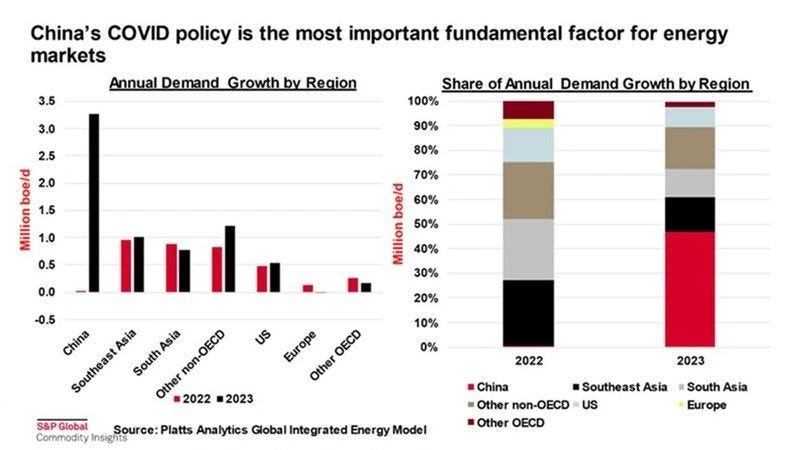

The resumption of Chinese economic and industrial activity, as well as incremental travel, implies 2-3MM bbl/d of oil demand just to recover to 2019, pre-covid levels. And this doesn’t account for the longer-term demand growth trend or “catch up” demand from over a billion people locked down for years. Some analysts are forecasting that that Chinese de-confinement could add up to 3.3MM bbl/d of oil demand, more demand growth than the rest of the world combined, and jolt prices higher [4]:

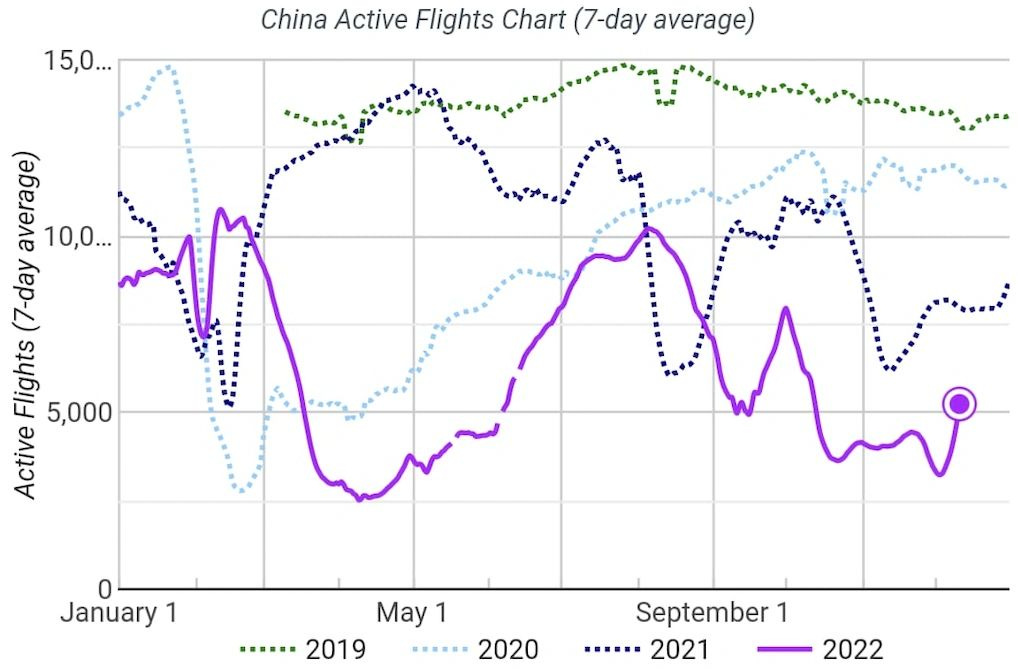

China active flights continue to rebound off dramatic lows—an important signal for gauging incremental oil demand and a broader, early indication of rebounding economic activity in China. The below charts show day over day changes in the number of flights in China, with a 7-day lag, and were taken on December 8 and 13, respectively. The number of active flights in China has nearly doubled from early December lows, and may quickly return to the pre-lockdown levels of 10,000+ per day:

Source: Airportia

The U.S. has released nearly 180MM barrels of crude oil from the strategic petroleum reserve (SPR) to lower gasoline prices for consumers. U.S. commercial + SPR oil inventories are now at levels not seen since the mid 1980’s:

Historically, the change in U.S. oil inventories has been a leading indicator of oil prices. While SPR releases have had a modest impact on gasoline prices, they may ironically lead to much higher prices in the future, as there is much less oil in reserve to address actual emergencies or supply disruptions. Oil equities appear to be reflecting these improving fundamentals ahead of the oil price itself, as indicated by the recent divergence between the ETF's USO and XLE:

Opportunity in Small Cap E&Ps

With the backdrop of improving oil market fundamentals, we continue to find small-cap oil and gas equities particularly compelling. As we addressed in Small-Cap E&Ps: Compelling Opportunity, these have materially underperformed both large-cap peers and the broader market indices since the prior cycle oil market high, despite strong current financial and operating performance. This offers compelling potential upside to “catch up” in a sustained bull market:

Small cap oil & gas equities continue to trade at a material discount to larger cap peers on relevant metrics, despite compelling fundamentals. With prices having fallen recently, this valuation differential has widened, making the opportunity even more compelling.

Opportunity in Oil Field Services

We continue to find opportunity in oil field services equities, a thesis we briefly addressed in Important Off-The-Run Metrics Indicate More Oil Opportunity Ahead. Like small cap oil and gas equities, oilfield services equities have been laggards despite strong recent financial and operating performance, and they too have significant upside potential from a “catch up”:

Following Russia’s invasion of Ukraine, and with some parts of the world facing critical shortages of oil and potential blackouts, sentiment is slowly improving for the development of oil & gas assets in the near term, both to prevent runaway inflation and to secure threatened energy supplies. In North America DUC inventories have been depleted, necessitating more drilling rigs and related services to complete and tie in the same number of wells, as we discussed in the 2022 Oil Outlook & DUC Dilemma:

In the face of challenged supply and dwindling domestic inventories and DUC counts, we are seeing a resurgence in oil and gas drilling and exploration activity—which had been muted since the last cycle ended in 2014. In this environment, companies that provide drilling rigs, pressure pumping and completion equipment and crews, and other essential oil field equipment to E&Ps may outperform.

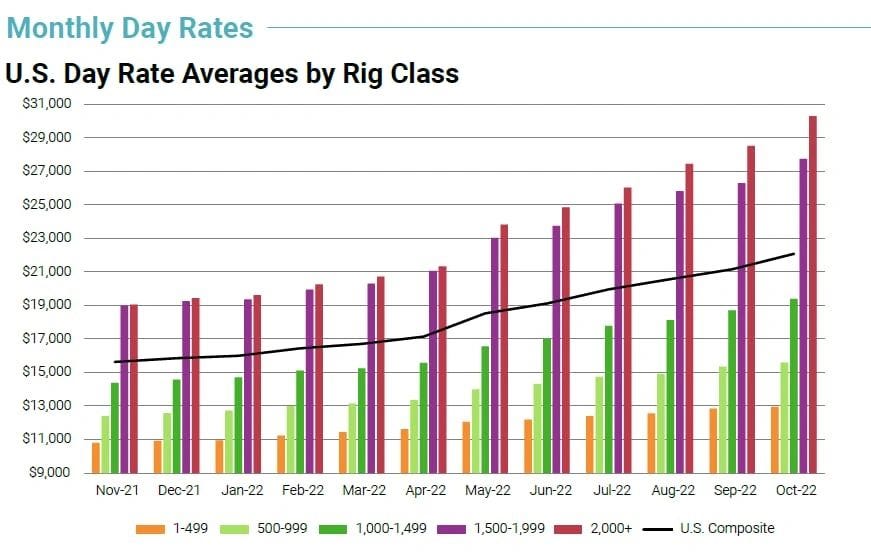

Drilling rig counts are already picking up in the U.S. and elsewhere, and there is considerable tightness in the space due to underinvestment in the sector following the previous down cycle. Day rates for drilling rigs have been on the rise, and as a result, E&Ps have already seen considerable cost inflation while rig provider profitability has been rising:

Source: Enverus

There are several indications that rising day rates are likely to persist in 2023. There is considerable tightness in the supply of drilling rigs available, as many are already locked into medium-term contracts. In some instances, E&Ps willing to pay higher rates are still unable find the necessary rigs, resulting in production delays. Shortages are particularly acute among higher specification rigs, which are equipped with various features that allow for pad-optimized batch drilling, particularly for shale formations.

Looking Ahead

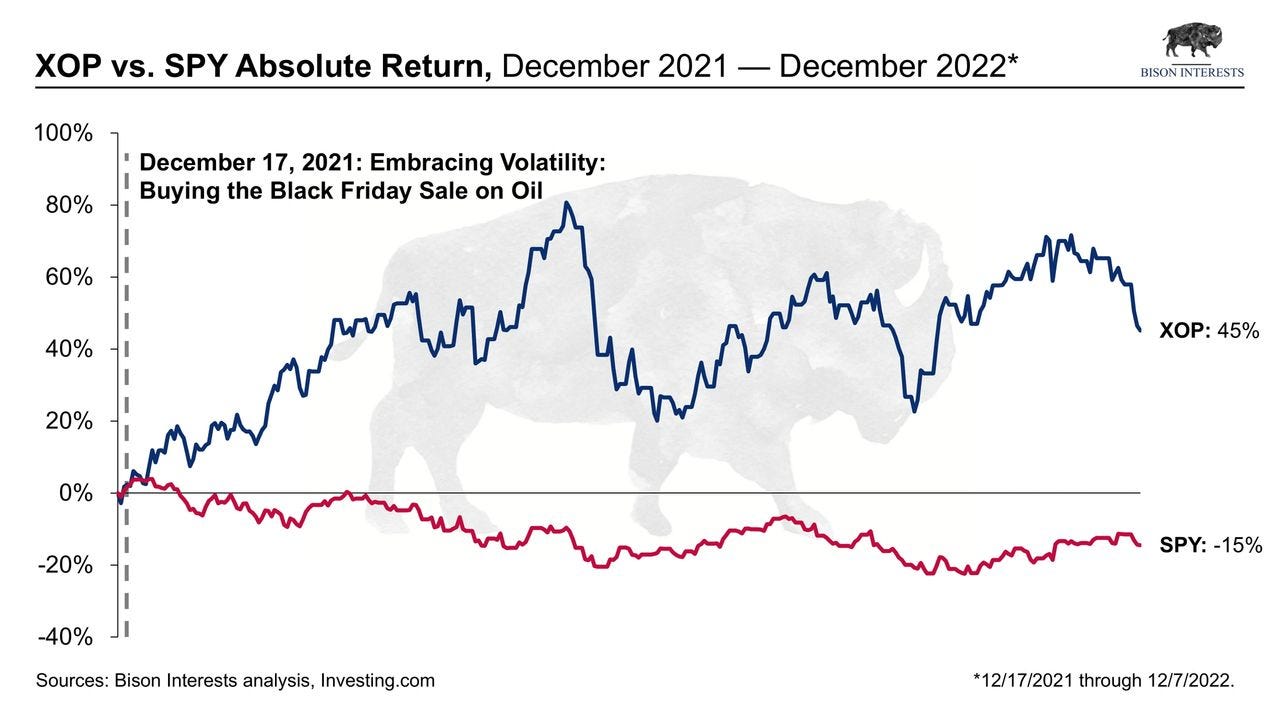

In December 2021, we addressed the oil market sell-off associated with renewed Covid fears from the Omicron wave in Embracing Volatility: Buying the Black Friday Sale on Oil. Despite recent price action we argued that the fundamental backdrop for oil remained compelling, and that it presented an opportunity to buy oil & gas equities at a discount. In hindsight our paper was well timed, nearly “bottom ticking” the market:

One year later, oil & gas equities have experienced another drawdown, yet the fundamental setup is even more attractive. Supply is tight, demand is improving, and China appears to be rapidly re-opening. This presents us with another compelling opportunity to face into the fear and negative sentiment to buy oil & gas equities. Most compelling to us here are the equities of heavily discounted small cap oil and gas producers and oilfield services companies, despite the significant volatility that likely lies ahead.

Sources

[1] Source: Al Jazeera

[2] Source: Oilprice.com

[3] Source: The Wall Street Journal

[4] Source: S&P Global

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Thanks for sharing your views. I must admit to sitting on the fence with energy over the last year, bullish long term, but with a worsening slowdown ahead of us a just can't square the circle at this moment in time. All the fundamentals scream buy and hold but I'm yet to see a compelling argument of bullish price action if a hard recession hits.

Great article.