Another Big Permian Oil Deal

Another Big Permian Oil Deal

Callon’s Recent Acquisition Implies Further Upside for Vital Energy

Merger mania in the Permian basin continues with the $600+ million acquisition of a private oil company by a publicly traded oil & gas producer. Callon Petroleum (NYSE: CPE) is buying Permian assets from Percussion Petroleum while selling non-core Eagle Ford shale assets to Ridgemar Energy, both backed by the private equity firm Carnelian. This transaction dynamic is reminiscent of the recent deals between Ovintiv (NYSE: OVV) and the private equity firm EnCap, which set a recent high marker for Permian transaction valuations.

Similar to the Ovintiv deals, the Callon net effective price paid for the Permian assets is also likely higher than advertised due to estimated liabilities assumed by Callon. This high deal price perpetuates the trend of rising private to public transaction multiples for oil & gas assets, particularly in the Permian basin. It also highlights the significant upside for Permian focused Vital Energy (NYSE: VTLE) and other discounted small cap publicly traded oil & gas producers. Further analysis below.

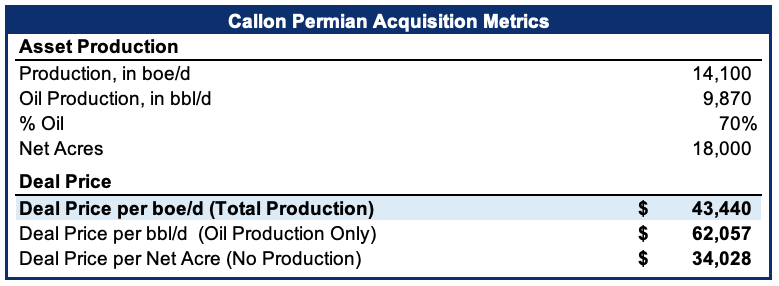

Callon Acquisition and Implications

Callon is buying 14,100 boe/d of production (70% oil), for a consideration valued at $475MM at the time of announcement, including cash and stock. In this transaction, Callon is also assuming some of the existing contingent liabilities of $12.5MM for 2023, as well as $25MM for 2024 and 2025 if oil prices average $60+/bbl. Also, sources indicate that Callon is assuming liabilities in this transaction including out of the money commodity price hedges, which we estimate at $75MM:

After relevant transaction adjustments, Callon is paying $43,000 per boe/d, a healthy valuation which is reflective of improving transaction multiples:

It is worth noting that CPE likely paid a higher price for these Permian assets to add to quality inventory, adding 80 net operated drilling locations with a mid-range breakeven price of $52/bbl. In its Eagle Ford sale, Callon is giving up 65 net drilling locations with a breakeven price of $56/bbl. Some analysts estimate the Permian assets transacted at PV-10 while the Eagle Ford assets transacted at PV-15; differences in inventory quality reconcile this valuation difference to some extent, although some sources indicate a much smaller number of high return potential drilling locations in the Permian asset.

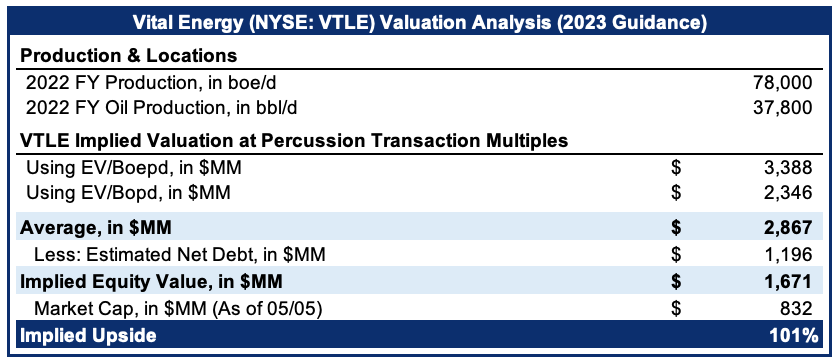

Implications for Vital Energy

This Permian transaction reads-through well for Vital Energy. Vital has similar but larger assets, that are valued in the public market at a fraction of the price implied by this transaction. We estimate that this transaction implies 100% upside for Vital Energy based on management’s 2023 production guidance, which has been conservative recently:

$43,000 per boe/d is on the low end of the rising transaction value trend for oil & gas production assets in the Permian basin. While it is not the highest value recent deal, it is continuing the rising price trend, and indicates a hot market with numerous potential buyers for these assets. Factors including limited inventory, a history of legacy low performing wells, and comparatively small asset size at 14,100 boe/d may have contributed to this lower deal valuation. It is noteworthy that Vital is much larger than Percussion but is otherwise similar in many respects, making this a relevant deal “comp” that could represent the low end of a reasonable value expectation range in a sale. With more inventory and a larger size, Vital might sell for more than a 100% premium.

While deal valuations at $43,000 per boe/d are healthy, they are nowhere near the high end of deal valuations we’ve seen recently. and it helps that valuation multiples in private/public oil deals are rising. As such, this is meant to illustrate a base case for Vital at the current valuation. Additionally, this may represent the value of Vital’s assets to a potential acquirer like Callon.

Conclusion/Takeaways

It is worth noting that there are still many publicly traded, smaller capitalization oil equities that are currently trading at lower multiples than that implied by this and other recent transaction, despite having similar assets. Even at reasonable mid-cycle valuations, the premiums implied in these transactions offers potential significant upside, likely due to depressed public market valuations and numerous funded bidders. This seems particularly true for Vital, which screens cheap even against heavily discounted small cap peers.

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises owns shares in Vital Energy (NYSE: VTLE), and may buy or sell shares without any further notice.

Good piece.

Now we know why Josh stayed home from Omaha. Parenting AND writing.