Bison: Tying the Macro with the Micro

Bison: Tying the Macro with the Micro

(Important Disclaimer at the Bottom)

This one is a little different. We have typically used this space to share a particular oil & gas market analysis or insight. We hope that these are helpful in providing industry context and promoting a better understanding of the price dynamics of often maligned but critically important commodities.

We also do these analyses to improve our own understanding of the industry and the trajectory of macroeconomic factors, and ultimately, commodity prices and company valuations. This month, we’re sharing a little about how we use our research in finding and evaluating investment opportunities – connecting the macro with the micro.

But first, a brief overview of the oil market and relevant changes since last month’s update:

Oil & Gas Fundamentals Are Promising Despite Lower Prices

The fundamentals for oil and related equities are unusually compelling. Absent a significant global economic crisis, the world oil market is likely to remain undersupplied for many years. This undersupply is a consequence of persistent underinvestment in oil exploration, delineation, and related services. And under-investment is aided by anti-industry government policy and shifting investor preferences that encourage return of capital over investment in oil and gas.

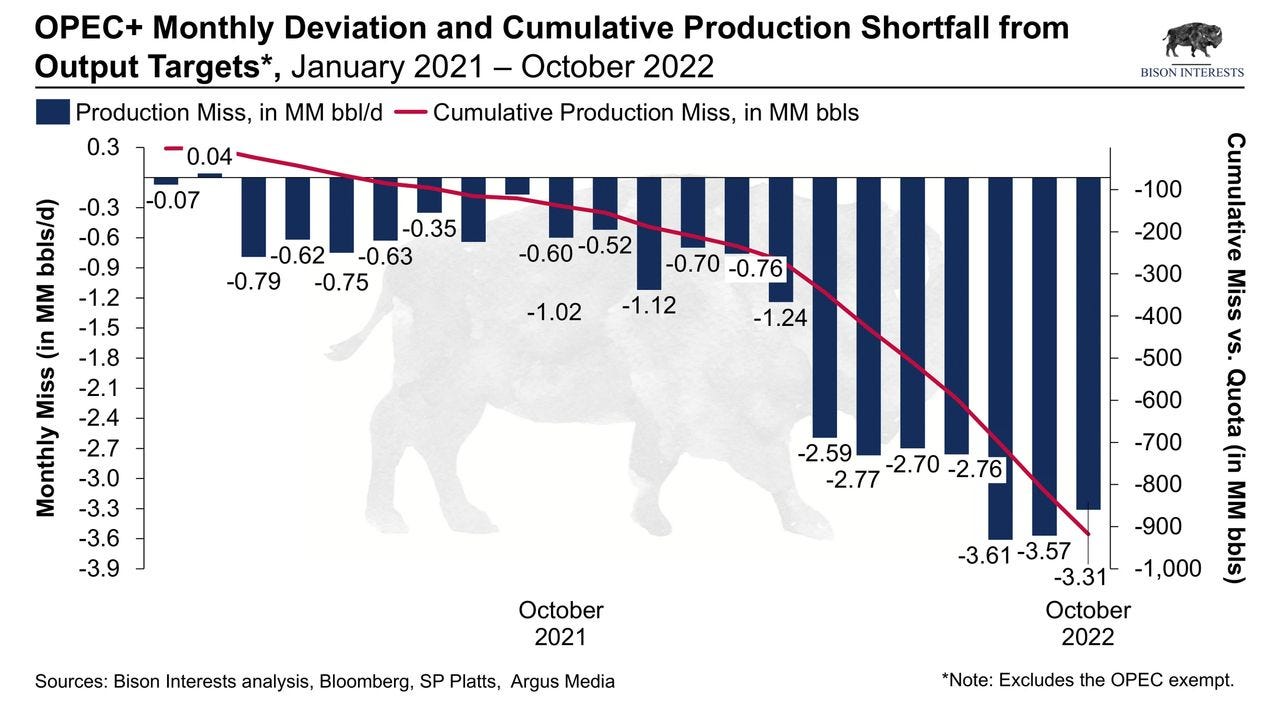

The consequences of persistent underinvestment have already begun to materialize. Even the world’s most prolific oil producers are now sounding the alarm. Saudi Arabian and other OPEC+ country energy ministers, national oil company executives, and others are sharing concerns of a critically under-supplied market and insufficient spare capacity. OPEC+, which controls ~40% of global oil production, has cut production quotas by 2MM bbl/d to partially reconcile nearly 2 years of below-quota production. And these OPEC+ quotas have been renamed “targets”, perhaps in recognition of the difficulties in meeting agreed upon production levels:

The production outlook for non-OPEC countries is also disappointing expectations. Russian oil production has been dwindling; a result of intensifying western sanctions combined with maturing oil fields with limited reinvestment. U.S shale production growth has likely peaked, with individual well productivity peaking or falling in most shale fields. Having already drained it’s DUC inventory and facing labour and drilling shortages, the US oil industry is struggling to increase production sufficiently to make up for production losses elsewhere and has significantly undershot consensus forecasts for 2022.

Against a backdrop of lower-than-expected production, oil demand continues to grow steadily, contrary to the prevailing narrative and net-zero policy goals. This is despite China’s aggressive zero-COVID policies, which are showing signs of loosening. Consequently, oil prices are likely to remain elevated for years, and producers share prices may benefit materially (with lot of volatility along the way).

The Golden Age of Oil & Gas Producers

In this secular oil and gas bull market, the share prices of oil and gas producers, services companies and related equities are likely to outperform the broader market. This is particularly true after a period of over-investment in other sectors, and as corporate earnings weaken along with leading economic indicators. Even in the scenario of a global recession, oil demand deferment may be insufficient to offset current supply deficits. Key considerations include declining Russian oil output, lack of OPEC+ spare capacity, and signs of the lifting of COVID lockdowns in China. To the extent that the world experiences a period of poor economic growth with high inflation, or stagflation similar to that of the 1970’s, oil equities may still outperform other asset classes:

Dispersion of Valuations and Differentiation of Oil Company Performance

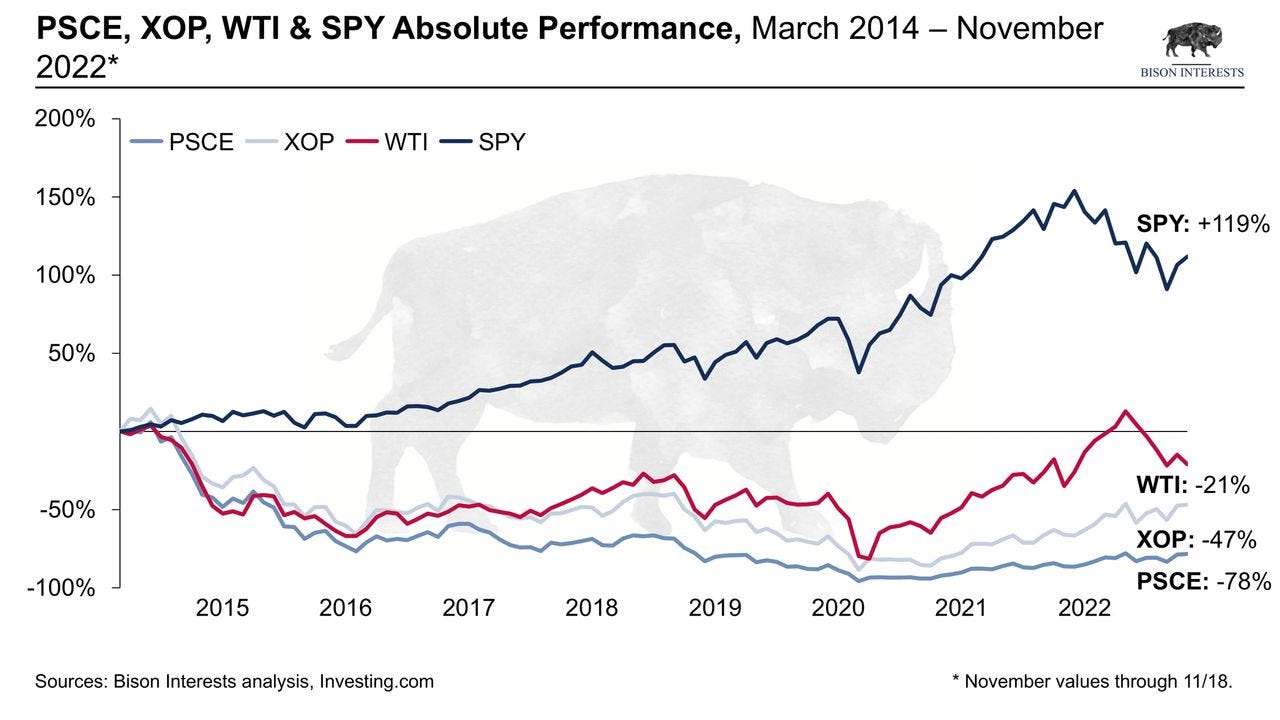

With oil prices rising faster than the associated costs of production, E&Ps should benefit materially. As expected, E&P share prices are outperforming the underlying commodity over time, as improving fundamentals are starting to be priced in by the market:

Oil and gas fundamentals have meaningfully improved over the last year, and the trade has garnered some intention from retail investors, asset managers, and the media. Underperformance of other sectors, particularly technology and “high growth / no profitability,” may be helping attract reluctant investors.

Oil and gas equities have traditionally traded in lockstep with oil futures. However, the above suggests that there has been a divergence since October, with oil equities trading up faster than the oil price. This may be indicative of re-invigorated investment interest in the space, which may catalyze a re-rate in oil and gas equities. These are currently pricing in materially lower-than-market oil and gas prices and remain undervalued versus both other asset classes and prior periods in which oil prices were similar.

Dispersion of Valuations Offers Stock Picking Opportunities

Not oil & gas equities are created equal. Over time, some companies are likely to outperform others, in some cases by orders of magnitude, due to differences in fundamentals and valuation. As we have displayed in prior white papers, Bison’s research and due diligence process is two-pronged: we approach investment due diligence from a top-down macroeconomic perspective to identify a sub sector of interest, and combine it with fundamental, bottom-up analysis of individual securities to identify those likely to outperform the peer set.

From an investment perspective, macroeconomic analysis is useful in identifying an investable universe of securities to express a particular theme. This research process occasionally leads to a result that we share via a white paper for you, our reader. We extensively diligence each of the identified companies, looking for those with value creating management teams, survivable balance sheets and quality assets at heavily discounted valuations. And in that diligence process, we sometimes identify a broader industry insight, which helps us identify promising themes and topics of macroeconomic analysis. Ultimately this is a circular process, bearing interesting investment ideas and relevant industry insights. More on this below.

Identification of Macroeconomic Drivers and Prior Investment Research

Our top-down research is focused on identifying niche, poorly understood sub-sectors of the oil and gas space which appear to be inflecting. Some generalists and macro analysts may have recently identified that oil and gas equities are likely to generate higher returns in the next few years. Differentiated analysis can be an important factor in leveraging that insight to actionable ideas.

Some of our oil and gas industry analysis has been disseminated publicly. We are proud of the research we have shared to date, particularly as our contrarian views on poorly understood niches in the oil and gas sector have gained broader acceptance. Almost two years since we started tracking the performance of our research, we are proud of our track record:

In the context of this research track record, and the compelling opportunity set of undervalued oil and gas equities with dispersion of valuations and exposures, we re-visit some of the insights from prior white papers and we connect them with associated investment opportunities.

Lack of OPEC+ Spare Capacity & Opportunity in Canadian Heavy Oil

We first shared our OPEC+ limited spare capacity thesis in September 2021, at a time where it was widely believed that OPEC+ had sufficient spare capacity to flood the market quickly. This was an overhang on the market and led to a misperception that rising oil prices were likely to be a temporary phenomenon. Only a year later, Bison’s initially highly contrarian piece on the lack of OPEC+ spare capacity has been broadly accepted by market participants and the mainstream media, particularly after OPEC+ announced a 2MM bbl/d cut to its production quota.

As the world begrudgingly accepts that OPEC+ production has likely peaked, there may be a call for more production from non-OPEC countries such as the US and Canada. Unfortunately, US shale production is already peaking—a view now shared by numerous industry insiders and analysts, and that we addressed in the DUC Dilemma below. Canada, on the other hand, has the second largest proven oil reserves in the world. These are concentrated in the oil sands, which have much lower decline rates than US shale.

As political sentiment shifts away from environmentalism towards energy supply security with rising oil prices, while OPEC+ spare capacity is depleted, Canada may become the world’s marginal supplier of energy. And with rising geopolitical uncertainty, there is likely to be an even higher premium on quality assets in traditionally stable jurisdictions.

In this environment, small Canadian producers would benefit disproportionately because these are the least likely target of potentially harmful regulation floated by regulators, such as windfall profits taxes, and are generating significant cash flow. We shared a few likely beneficiaries in a Bloomberg interview, which have done quite well since.

The DUC Dilemma & Emphasis on Low-Decline Production

In our January 2022 DUC Dilemma, we argued that the US was rapidly depleting its inventory of drilled uncompleted wells to maintain production amid muted drilling activity. Without a material increase in drilling rigs relative to frac spread counts, US production growth was likely to disappoint expectations. After almost a year and almost a million barrel per day oil production disappointment vs EIA projections, this view now appears to have made it into headlines. It is remarkable that the US has struggled to increase oil production since the 2020 market downturn despite materially higher prices:

Most of the best wells in the US shale patch have already been drilled and exhausted: moving forward, shale production will likely necessitate higher re-investment rates just to maintain production levels. This is problematic as oil field services costs have increased dramatically, and there are some critical shortages in the oilfield services value chain that are unlikely to be resolved for some time.

As shale disappoints, there may be a renewed focus on conventional production with lower decline rates. And while low-decline oil production assets have traditionally commanded a premium in prior bull markets, remarkably, there are still some publicly traded E&P companies with low decline rates that are trading at meaningful discounts to their high decline counterparts. We discussed one of these in a recent Seeking Alpha article, well as on Bloomberg and elsewhere.

Compelling Opportunity in Small Cap E&P’s

Despite rapidly improving fundamentals, the broader small cap oil & gas sub-sector remains heavily discounted vs. both large cap peers and the broader market, as we initially discussed in our May 2022 white paper, Small Cap EP’s: Compelling Opportunity. We see the potential for valuations to improve across the board in this bull market, with equity multiples potentially trading in-line with historical averages in periods where oil prices were similar, or higher.

Several catalysts may drive a re-rate in small cap oil and gas equity valuations. For one, small-cap producers have materially underperformed both large-cap peers and the broader market, as can be seen below:

This underperformance has been exacerbated by multiple compression; whereby small company fundamentals have improved while share prices have stagnated. There is potential for small cap equities to re-rate significantly, and small cap oil and gas producers we have discussed may be promising beneficiaries.

Additionally, smaller producers usually have a higher cost of production then their large cap counterparts, implying greater FCF torque to higher oil prices. These have exhibited larger increases in cash flow and faster debt paydown than large caps, yet still command significantly lower valuations.

Bison Fundamental Analysis

Bison’s raison d’être is finding the best possible opportunities within the oil and gas space and pursuing them. This approach requires us to select specific companies we believe are likely to outperform peers, rather than having broad exposure to themes through baskets of securities. Effective due diligence and fundamental analysis of individual securities can lead to material outperformance over time, as evidenced by the outperformance of companies we have publicly disclosed owning, from the time of the dissemination of our thesis, vs. the broader sector ETF XOP:

Bison Research: More to Come

Over the years, Bison has publicly disseminated several of its stock picks, particularly through appearances on mainstream media and on Seeking Alpha. We found that sharing these ideas has helped in crowdsourcing research, often yielding feedback on our investment theses by those with niche knowledge including geology, regulatory frameworks, pipeline availability, and local pricing dynamics. We are grateful to have a knowledgeable set of readers with such diverse backgrounds, with whom we can share ideas and receive feedback.

Additionally, public dissemination of select securities has given our followers a deeper look into our due-diligence and macro analysis, while also spotlighting the value of our industry research. To complement the investment theses we have already shared publicly, we wanted to share how our macro research related to them and to tie the two together more explicitly. We are proud of the track record of our publicly disseminated stock picks and white papers, and we look forward to continuing to provide differentiated perspectives.

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.