Embracing Volatility: Buying the Black Friday Sale on Oil

Embracing Volatility: Buying the Black Friday Sale on Oil

(Important Disclaimer at the Bottom)

On the Friday after Thanksgiving, “Black Friday,” there was a 12% drop in the price of oil. The combination of renewed Covid fears and shifting macro-economic dynamics sent volatility spiking and oil and gas equities plunging. Many pundits and “experts” who were late to the oil market rally were quick to call for the end—to this we say: “not so fast!”. We remain convinced that we are in the early innings of a multi-year bull market, and with a few clouds forming, we face head-first into the potential storm.

The selloff came on a day with historically low volume after the announcement of the novel Omicron variant (conveniently skipping two Greek letters). The sell-off appeared sentiment driven, as with a lack of concrete data it was up to investors imaginations to forecast it’s market impact. A few weeks later, the prospect of renewed lockdowns in major economies appears unlikely, as both real-world data and messaging from health officials suggest that Omicron, while far more infectious than previous mutations of the virus, is far less deadly:

Low Market Breadth Indicates More Volatility to Come?

While oil and gas equities are poised for another leg higher, the broader market appears to be rolling over. The divergence between “real” economy stocks—which trade a single-digit multiples of cash flow—and growth equities seems to be reversing. The latter seem to be losing steam: the tech-heavy NASDAQ’s push higher is increasingly driven by the mega-cap FAAMNG stocks while the rest of the index continues to languish:

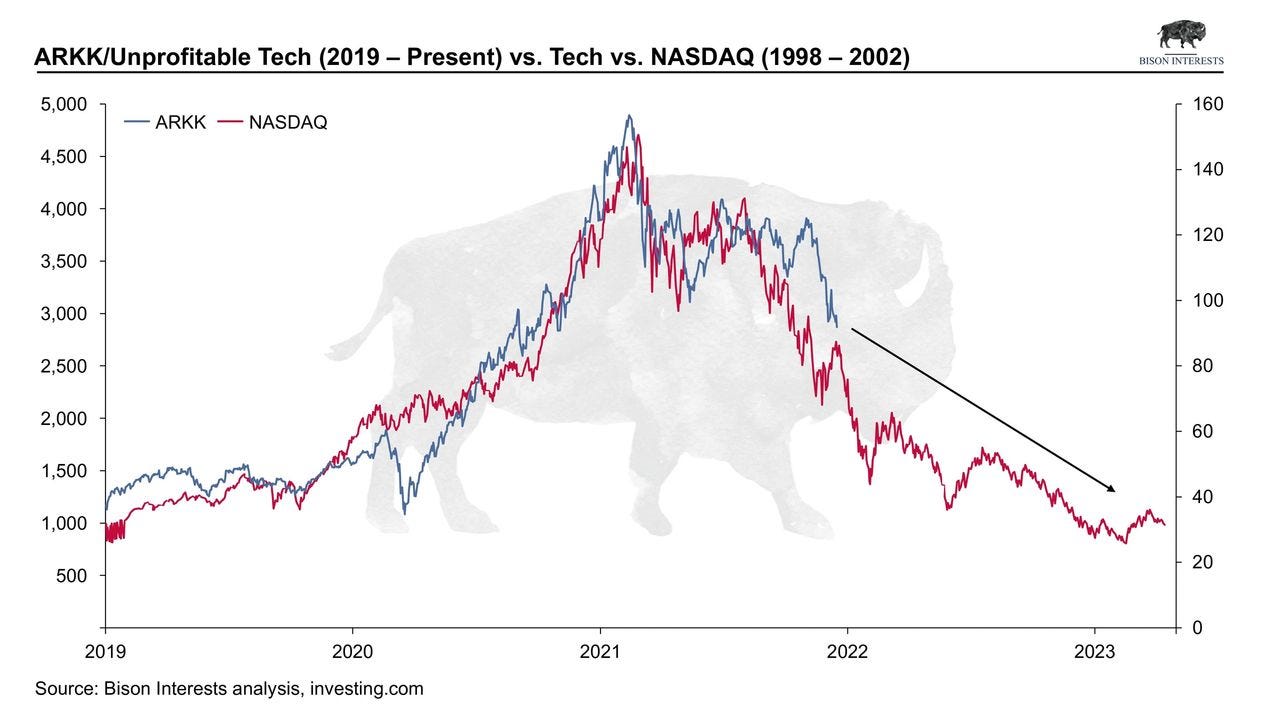

Historically this has portended a wider market reversal, particularly as index leaders turned to laggards. Additionally, higher equity valuations imply increased risk from the federal reserve’s policy decisions. The fed recently announced that they will begin tapering their bond purchases and raising rates faster than originally projected to assuage white-hot inflation, posing the risk of a taper tantrum similar to the one in 2018 [1]. This risk is especially pronounced this time around as most growth stocks have essentially become “long duration” equities, with most of their present values coming from cashflows expected to be generated far in the future—which are far more sensitive to changes in interest rates. Therefore, a small increase in rates could materially affect the present value calculation for growth equities and swiftly unwind sky-high valuations. This is reminiscent of the collapse of the Dot-Com bubble, as illustrated by this chart showing the ARKK ETF, which is largely comprised of richly valued and unprofitable tech companies, overlaid on the NASDAQ as it crashed at the end of that bubble in 2000 — 2001:

While Bison owns none of these companies in its portfolio, the role of fund flows in an indexed market should not be overlooked. The foundation of our investment strategy is buying good companies at bargain valuations. However, we appreciate the risk that in a broader market selloff, portfolio holdings may be negatively affected (as they have been already). We continue to capitalize on this short-term volatility to add to long-term positions, as we maintain the view that oil equities remain cyclically and structurally cheap, and commodity prices are headed higher:

Energy Stocks are Still Cheap, “Pricing in” Lower Oil and Gas

Despite multiple compelling longer term bullish factors for the oil and gas sector, the equities are currently “pricing in” much lower commodity prices than the prevailing market price, which is even lower than the price indicated by backwardated futures markets. Below is a Credit Suisse chart illustrating this, albeit in a messier form than we’d like. In short, oil and gas stocks are trading as if oil were at $51 and natural gas were at $2.65, despite recent prices of $70 for WTI oil and $3.80 for Henry Hub natural gas. This implies a substantial “margin of safety” embedded in the equities, which can be enhanced through further selection of value priced individual oil and gas stocks:

Insufficient Investment in Oil & Gas Production Results in Higher Prices

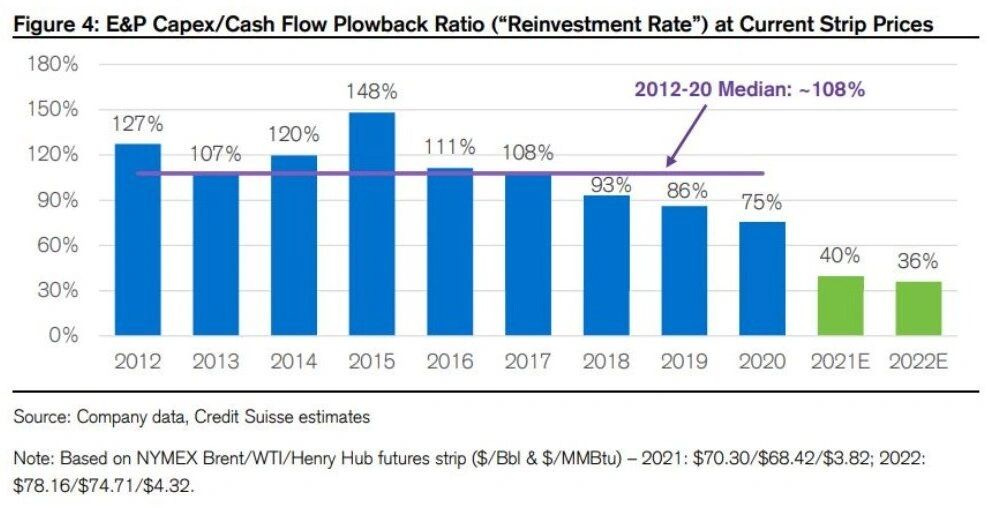

The longer-term oil bull thesis remains intact. Producers continue to exhibit capital discipline, using the cash flow generated from higher market prices to buy back shares and pay dividends, rather than investing in exploration and drilling to sustain production. This is well illustrated in a recent chart from Credit Suisse:

The lack of investment in the sector has compounded for some time now, and it is becoming increasingly clear that future production will fall short of demand unless investment picks up materially. This is illustrated in a chart from JP Morgan, which implies much higher future oil prices:

Problematic policy will continue to contribute to projected energy deficits as world governments become increasingly hostile to the fossil-fuel industry, which ironically, coincides with the reduction in industry capital spending. World leaders and governments continue to reduce the industry’s ability to operate. In the US, the government has banned oil leases on federal lands and cancelled pipelines while simultaneously pushing for lower gasoline prices—policies which they insist are not causing higher energy prices [2]. Our CIO Josh Young addressed this profound misunderstanding of basic market economics recently on Al Jazeera .

Shifting investor preferences are also driving the investment shortfall, as banks and investment funds continue restrict oil and gas producers’ access to capital. Consequently, the supply of credit available to E&Ps has been shrinking, resulting in a higher cost of capital and contributing to lower industry-wide investment, further exacerbating likely future under-supply:

The Energy Crisis Roars On

You may not have heard this from muted news headlines in the US, but there is an ongoing energy crisis in Europe and Asia. It is likely the culmination of years of underinvestment in reliable energy sources, as a part of a poorly implemented energy transition. Global commodity prices continue to rise, fuelling price inflation as higher costs are passed along the value chain. The situation is especially bad in Europe, where natural gas prices have nearly quadrupled this year and are now sitting above $200 per barrel of oil equivalent, recently hitting a high of $270!

Energy Crisis: Cost Inflation and Spill-over Effects

In addition to costing people more to heat and power their homes in the winter and disproportionately burdening the poorest people, higher energy prices have a negative spillover effect into other industries. For instance, higher gas prices are forcing ammonia factories—which convert gas into fertilizer used to grow crops—to shut down, driving food prices higher [3]. Historically, food inflation has not reflected positively on the incumbent administration, and in some cases, has catalyzed revolutions such as the Arab Spring. As fuel and energy price subsidies roll out across Europe and elsewhere, prices may go even higher as demand destruction is averted through subsidies. Additionally, gasoline substitutes like fuel oil and diesel will be increasingly consumed, potentially forcing oil prices much higher from “surprise” demand.

The Oil Market is Under-Supplied: Insufficient Production Capacity & Relentless Inventory Draws

Onshore stockpiles of crude oil and distillates continue to draw down amidst a backdrop of post-pandemic heightened demand, which in our view, increases the likelihood of an undersupplied market moving forward. We addressed this previously in “Oil Demand is Outweighing Supply”, and the situation has since worsened. Additionally, the OPEC+ has the stated their intention to get inventories back to their 2000—2014 average of 338 MM bbls, a period in which oil prices were ~$100/barrel:

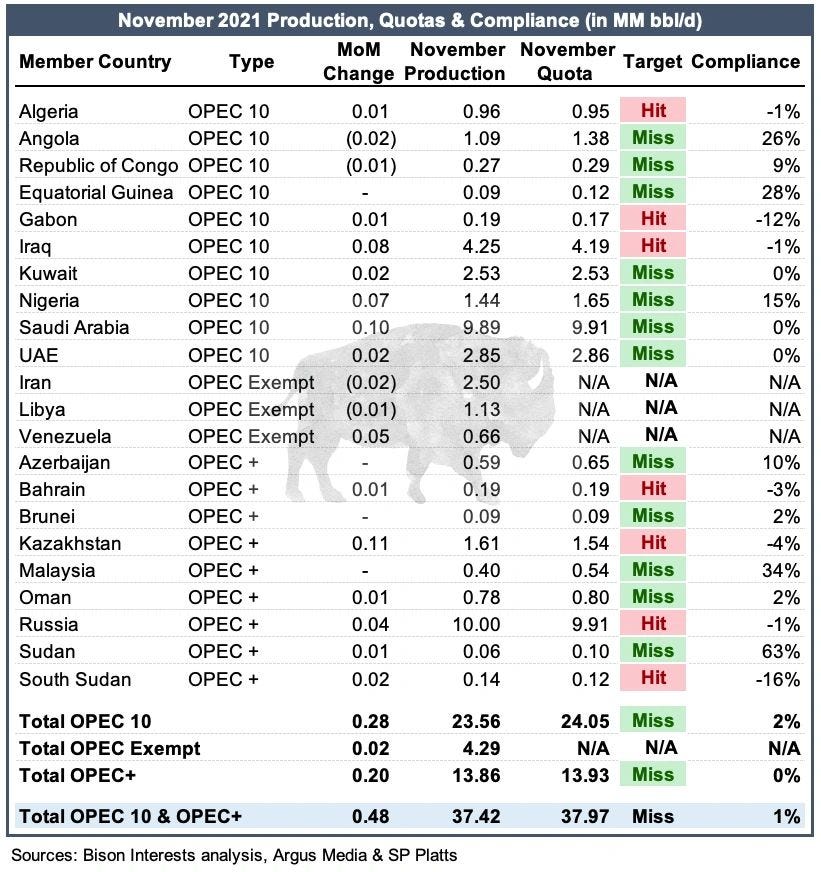

A consequence of sustained underinvestment in oil exploration, production and critical infrastructure is that most oil-producing countries simply don’t have the spare capacity needed to ramp up production moving forward. As such, it is likely that oil prices will rise as the market shifts into a structural deficit. This deficit may persist due to non-economic reasons such as ESG-driven divestment and unfavourable regulations. Our early call on OPEC+ spare capacity being lower than advertised is rapidly becoming a widely adopted narrative, with the cartel having once again come short of its own targets in November:

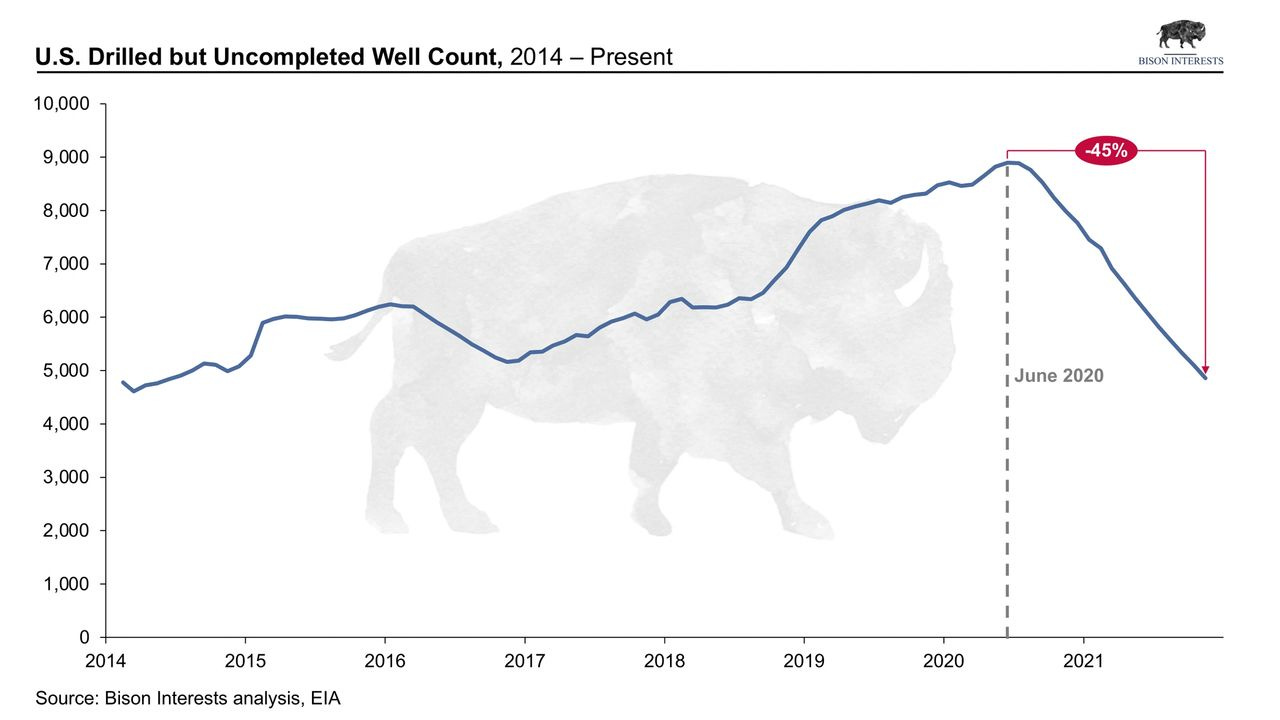

The situation in the U.S, which supplies roughly a fifth of global oil supplies, is equally promising for higher prices. The inventory of drilled but uncompleted wells (DUC’s), which are a form of working capital for E&P’s and are necessary to maintain and grow production, is approaching dangerously low levels:

DUCs are a form of oilfield working capital. A producing shale oil well is brought online in two distinct phases, each requiring different specialized crews and equipment: The well is first drilled using a drilling rig, and is then stimulated to production, or “completed,” using a frac spread. A DUC is a well that has been drilled but has not yet been completed (thus the DUC acronym: Drilled Un-Completed). Therefore, when the rate of drilling outpaces completions DUC inventory rises—which has been the case for some time now—DUC inventory draws down.

Bison is currently performing an in-depth analysis of the DUC shortage and possible outcomes moving forward (more on this to come). At a high level, we surmise that the higher supply of frac spreads relative to drilling rigs is a major driver of DUC depletion:

Our preliminary calculations indicate that the U.S needs to add over 100 drilling rigs to keep the DUC count flat and sustain production at current levels or deliver moderate growth:

This is a material increase over the existing rig count, which currently sits at 560 as of November [4]. This has meaningful implications for likely US production, as there is substantial lead time needed for rigs to be refurbished and/or re-activated, transported to the appropriate well pad and to then begin drilling. Additionally, severe labor and supply shortages may exacerbate the issue even if the equipment could otherwise be supplied on time. Ultimately, we anticipate that the rig count may not reach necessary levels for the reasons above, US production may continue to underwhelm expectations, and oil and gas prices will likely continue their climb higher.

Like many of the topics we address in our research, the potential impact on US production of the rapidly depleting inventory of DUCs is under appreciated. We are eager to continue our track record of success in research, and look forward to providing a more comprehensive analysis of the situation shortly:

Buying the Black Friday Sale

At Bison, we continue to view volatility as our friend. As fear and uncertainty sweep the market, we opportunistically buy equities that had already been cheap and are further discounted amidst an environment of fear, and occasionally, panic selling. As Baron Rothschild said: “Buy when there's blood in the streets, even if the blood is your own." With a strong longer term macro backdrop and inexpensive valuations, we continue to face into the storm.

Sources

[1] Source: The Wall Street Journal

[2] Source: The Financial Times

[3] Source: Bloomberg

[4] Source: EIA