Gas to Oil Switching – Winter is Coming

Gas to Oil Switching – Winter is Coming

(Important Disclaimer at the Bottom)

Once considered a “pioneer” in the transition to alternative energy, Europe is now in an unprecedented energy crisis. With limited LNG import capacity and its supply of natural gas from Russia cut off, Europe is reaching the point of desperation. The short supply of natural gas, which is primarily used to heat homes and generate electricity, is risking the quality of life of Europe’s citizens, the sustainability of its businesses, and the careers of its politicians.

Rather than attempting to rapidly add local supply, the EU is choosing to balance the market by forcibly lowering demand while subsidizing consumption—European Commission President Ursula von der Leyen recently announced that the EU would propose a “mandatory target” for reducing electricity consumption during peak demand. While energy rationing measures may dampen demand, they are not a viable long-term solution, particularly as Europe faces severe supply shortages of fossil fuels that may last for years due to restrictive green policy and the ongoing conflict with Russia.

The energy crisis that is presently unfolding is the result of years of underinvestment in and hostile policies towards fossil fuel energy infrastructure, along with policies that encouraged a shift towards less reliable renewable energy. The timeline for the impending crisis was only acceleratedwhen Russia invaded Ukraine, and Europe subsequently imposed sanctions. These have resulted in acute natural gas shortages, which have driven natural gas and associated power prices in Europe much higher:

Ironically, power prices may rise even higher as European governments continue to subsidise household consumption, while capping electricity producer profits. By eliminating demand destruction from higher prices, while reducing the incentive to produce electricity for utilities, the European is creating the perfect storm for much higher prices this winter.

Russia is “Weaponizing” Natural Gas

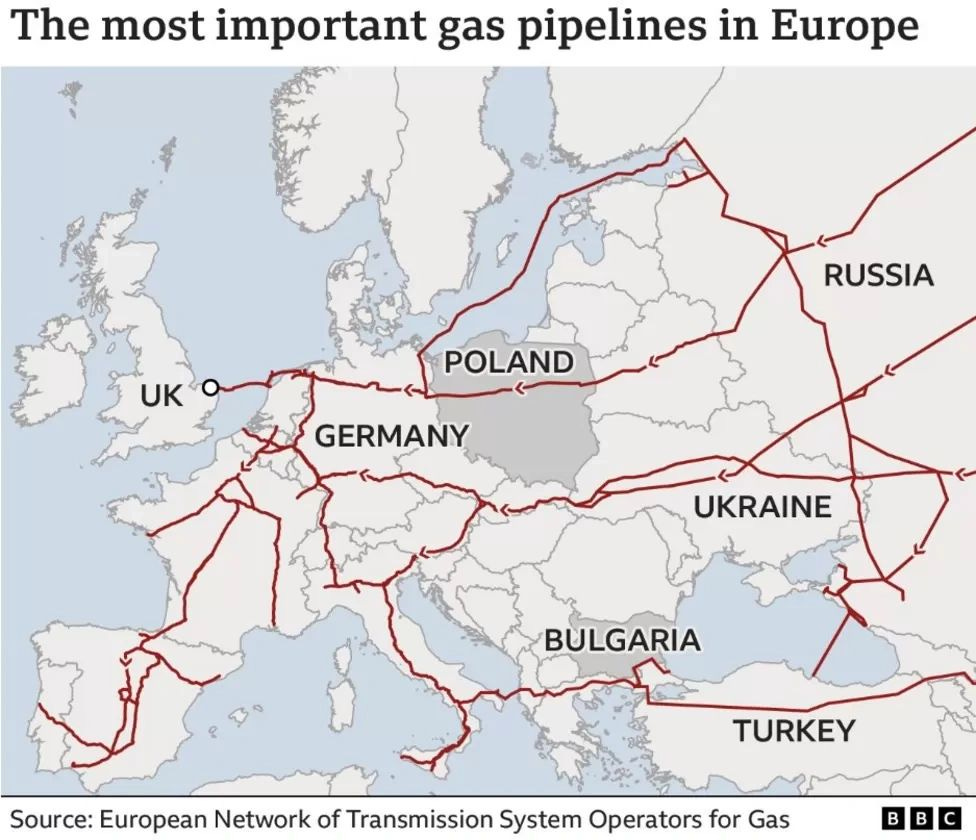

Having severely limited its own capacity to produce natural gas, Europe become heavily dependent on Russian natural gas imports via pipeline, as well as liquified natural gas (LNG) imports from the US and elsewhere. In 2021, the EU imported 40% of its natural gas from Russia via the Nordstream pipeline to Germany, as well as other pipelines running through Poland and Ukraine. [1].

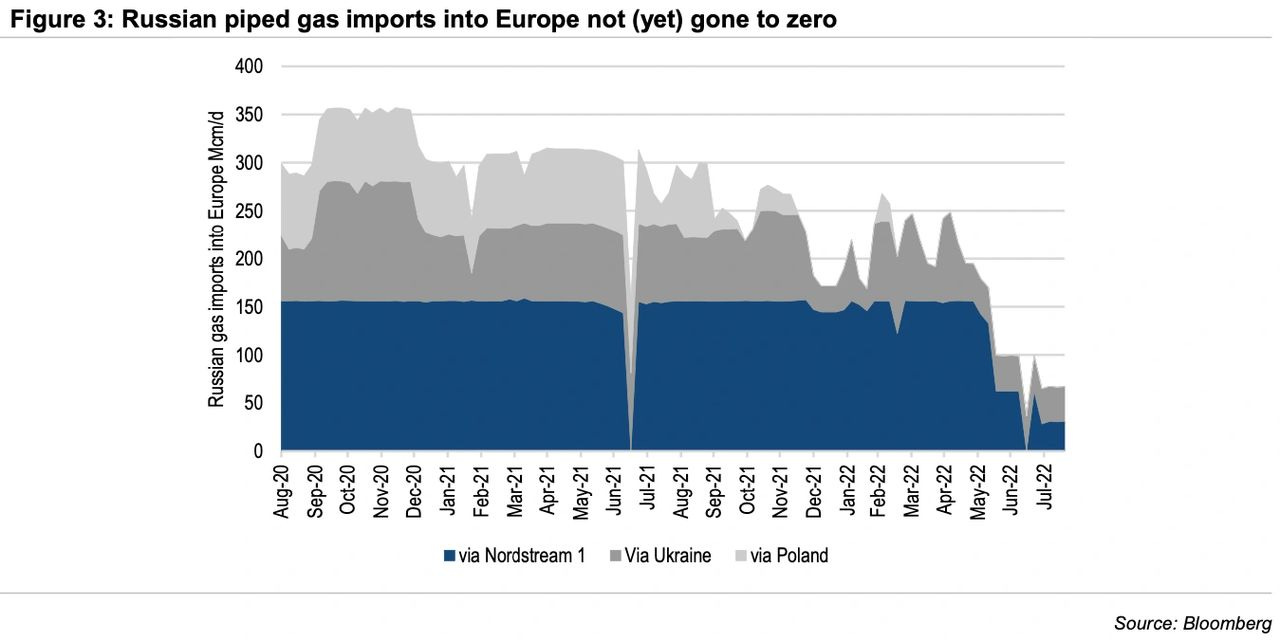

Following Russia’s invasion of Ukraine, European countries imposed several rounds of sanctions on Russian-sourced energy. And while initially Russian state-controlled producer Gazprom continued to supply some gas to Europe via pipeline, flows have been declining since the onset of the war:

Russia appears to be “weaponizing” it’s control over gas supplies to Europe. The Kremlin has made various claims regarding “technical problems” caused by western sanctions have reduced gas flows via pipeline. Most recently, Gazprom shut down the Nordstream 1 pipeline completely for “planned maintenance”, which was supposed to end on September 2nd. The pipeline has not been reopened, citing a gas leak that prevented the turbine from working. Should Nordstream remain shut-in, this could send gas prices even higher in Europe ahead of winter.

LNG Imports Won’t Save the Day

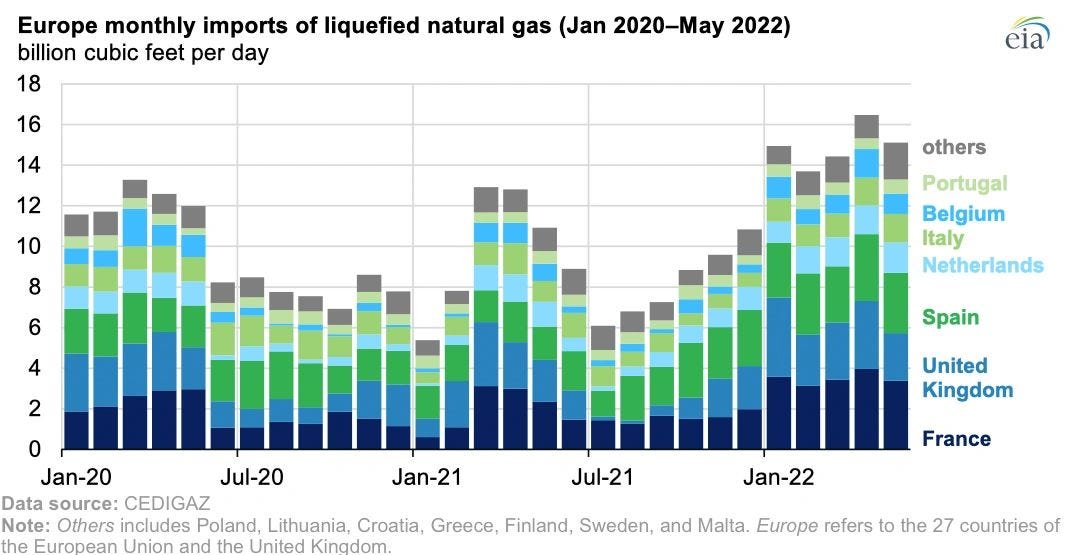

Europe has been dependent on LNG imports to meet domestic gas demand, even prior to this crisis. In early 2022, prior to the war in Ukraine, European countries had already begun importing record quantities of LNG to refill heavily depleted storage inventories:

To cope with rising prices and shortages following the war in Ukraine and associated energy sanctions on Russia, European countries have been looking to LNG imports. Consequently, insatiable European demand has been increasing global competition for LNG as it redirected cargoes bound for other regions. Unfortunately, there are several issues along the global LNG supply chains that indicate this won’t be enough to meet its needs ahead of winter.

A major issue is that Europe doesn’t have the import and regasification capacity to fully replace the gas that was previously coming in via pipeline. It doesn’t help that LNG import facilities may already be running above their sustainable capacities. Europe’s current LNG import capacity is 157 billion cubic meters in regasified form per year, or 15.2 Bcf/d [2]. From January through May 22, LNG imports into Europe and the UK averaged 14.9 Bcf/d, which is 5.9 Bcf/d (66%) more than the annual average in 2021, and 98% of total capacity [3]. Germany has already taken steps to secure five floating LNG terminals, another indication that current import capacity is insufficient [4].

Some central and eastern European countries receive limited LNG imports due to lack of water access. These countries were previously highly dependent on Russia for imports via pipeline. In response to lower Russian supplies, gas must now be transferred from coastal LNG import facility via pipeline. This has its challenges, as not all of Europe’s LNG terminals are fully integrated with pipelines. The countries that do have pipelines, mostly in Northern Europe, have limited takeaway capacity. Considering lengthy lead times and regulatory hurdles for building pipelines and other energy infrastructure, central and eastern European countries may face particularly severe shortages if Russian flows don’t resume ahead of winter.

Tight Global LNG Market

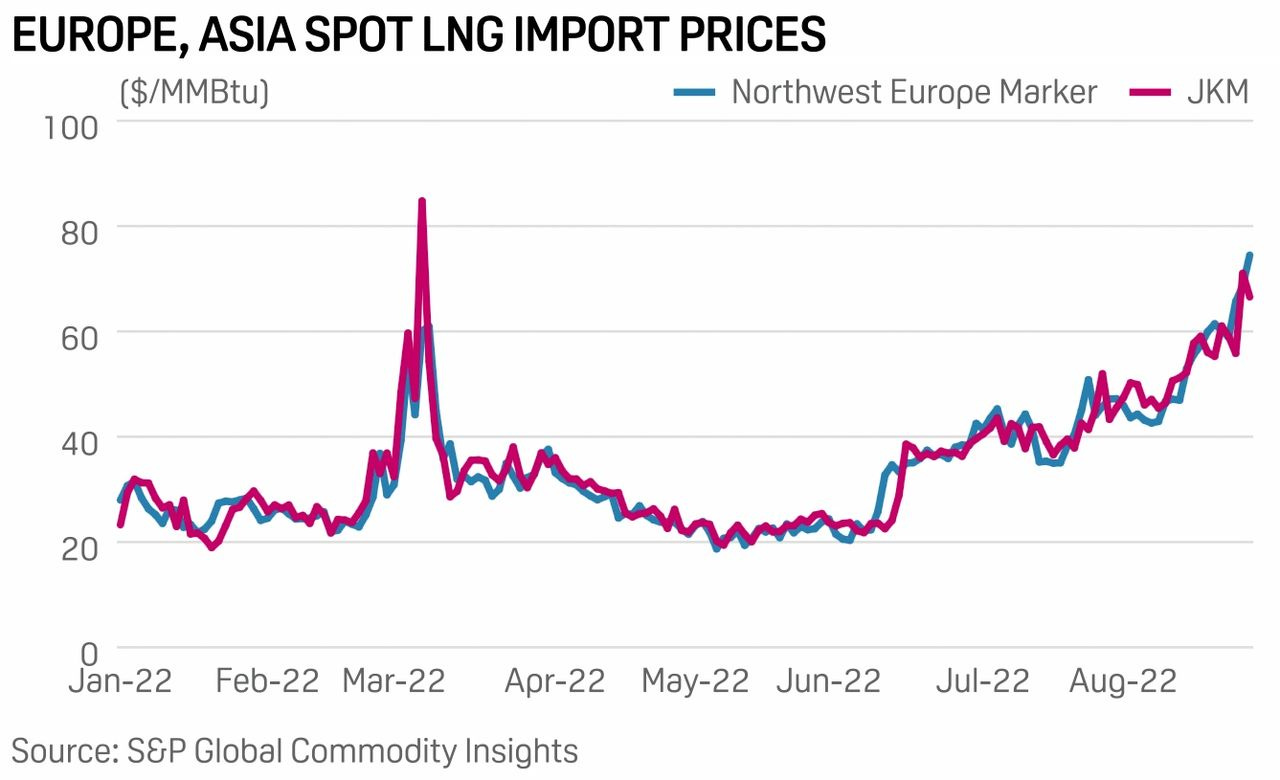

A tight global LNG market due to higher European demand may catalyze an energy crisis in Asia as well, which has also seen rising LNG prices:

There simply aren’t enough LNG carriers to satisfy global demand, and as a result, European and Asian buyers have been competing fiercely for limited cargos. Many cargos for the US and elsewhere have already been diverted to Europe, and as a result, Asian LNG imports have languished:

As Asia looks to refill depleted stocks of natural gas ahead of winter, competition for LNG is likely to intensify, driving higher prices. LNG vessel charter rates have already been rising in response to a tight market, further fuelling natural gas price increases:

As demand for longer term charters picks up with winter, with few new ships being built, charter rates in the pacific may swell to $400,000/day for a round voyage in winter [5]. Higher charter rates and global LNG benchmark prices could cause pain for consumers in Asia—Europe’s energy crisis may have a “contagion” effect on the rest of the world.

Gas-to-Oil Switching

Sufficient electricity generation is a major cause of concern for Europe. Faced with soaring natural gas prices and limited supply, European utilities may choose to burn refined oil products such as fuel oil, diesel and gasoline instead of natural gas for electricity generation. Doing so would be highly economic, as indicated by the price differential more than $250/barrel equivalent (boe) between Dutch TTF Natural Gas and Brent Crude:

Gas-to-oil switching is not a new phenomenon: in 2021, European power facilities generated 47.95 terawatt-hours of electricity by burning oil products, amounting to roughly 80,000 boe/d [6]. Switching activity in Europe picked up in the 4th quarter of 2021, in tandem with climbing natural gas prices, illustrating that there is some relationship between gas prices and switching.

The fundamentals for natural gas prices in Europe are compelling: demand will likely rise materially in the coming winter months, while supply remains constrained by a lack of LNG import capacity and restricted gas flows from Russia. And while European gas prices may continue to moderate from recent extremes, it is unlikely that these will revert to long term averages given the fundamental backdrop. And as gas prices settle structurally higher, we anticipate an increase in oil burning for power generation in Europe.

Asia is similarly affected by higher LNG prices, as gas has been drawn away from Asia to Europe by ultra-high prices. Asia and has the added benefit of existing oil burning power generators that had mostly been mothballed. Reactivating these and converting others to burning oil products will likely see a substantial uplift in oil consumption for power generation in Asia.

Switching Activity Estimation

In response the soaring natural gas prices in Europe and Asia and associated switching activity, the IEA recently revised its oil demand growth estimate upwards by 380,000 boe/d to 2.1MM boe/d [7]. Bison’s view is that the IEA and other analysts may be substantially underestimating the potential impact of gas-to-oil switching this winter.

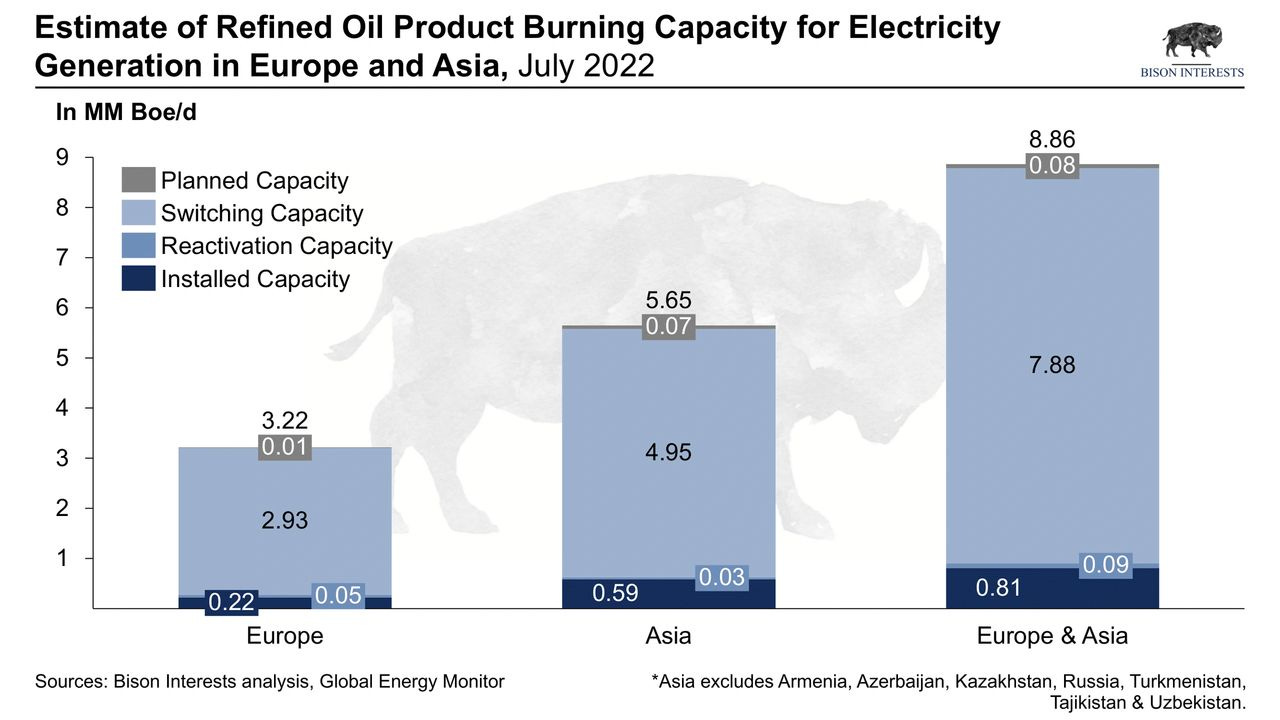

We have conducted our own analysis of oil burning capacity among power facilities in Europe and Asia, and as a lower bound we estimate that there is approximately 810,000 boe/d of installed oil burning capacity in Europe and Asia alone that will come online before this winter—more than 2 times the IEA estimate:

As gas prices remain elevated and electricity remains in short supply in Europe and Asia, we expect installed oil and oil product burning capacity will be utilized near 100% this winter. There is an additional∼8MM boe/d of upside to potential oil demand as non-operating plants are reactivated and operating plants are converted to burn oil. Even if only 10% of this capacity were to come online, it would imply a material 800,000 boe/d of surprise oil demand in addition to our 810,000 boe/d lower bound estimate.

Below an overview of our methodology, assumptions, and findings, as well as a discussion of their implications.

Assumptions

To simplify our analysis, we made a series of conservative assumptions.

Demand for 1 barrel of refined oil products (diesel, fuel oil and gasoline) would translate to one barrel of crude. This assumption adds a layer of conservatism to our estimate, given that 1 barrel of crude yields less than one barrel of refined products, and subsequently, demand for one barrel of refined products should have some multiplier effect on total demand for crude oil.

There is an efficiency factor of 95%. Given the magnitude of current shortages, it is reasonable to assume to that generators will run at 100% of nameplate capacity, with a 5% forced/scheduled outage rate (there is empirical evidence of this). For the sake of comparison, many plants in the US run at 96% of nameplate capacity in the winter.

Plant capacity is 100% transferrable between fuels.

Defining Different Types of Capacity

To arrive at our lower bound estimate of gas-to-oil switching, we defined 4 types of capacity.

Installed Capacity: Plants that are currently operating, and that are equipped to burn refined oil products. This is the power generation capacity that could most easily switch to refined products ahead of winter and is most likely to do so. Installed capacity was calculated to be 810,000 boe/d in Europe and Asia and served as the lower bound of our estimate.

Reactivation Capacity: Mothballed & retired plants equipped to burn refined oil products. This is oil product burning capacity that is currently not operating but could be brought back online ahead of winter. Several countries in Europe, notably Germany, have already reactivated fossil fuel plants, though they claim these measures are temporary. Our estimate of maximum reactivation capacity in Europe and Asia is 90,000 boe/d, although it is difficult to estimate how much of this capacity will come online ahead of winter.

Switching Capacity: Operating plants that are currently not equipped to burn refined oil products. In response to sustained higher gas prices, many operating plants not equipped to burn refined oil products may convert their generators. There is an upfront fixed cost in doing so, as well as a lead time of 2 months or more. Some operators may choose to undertake conversion projects as we enter “shoulder season”, the period in which gas demand from air conditioners declines but heating demand hasn’t yet picked up, and thus, electricity demand is lower. Our estimate of maximum reactivation capacity in Europe and Asia is 7.8MM boe/d, and while it is highly unlikely that all this capacity will convert ahead of winter, we do expect that some of it will, providing additional upside to oil demand which the IEA is not accounting for.

Planned Capacity: Announced, pre-construction, construction and previously cancelled projects that will be equipped to burn refined oil products. Our planned capacity estimate is 80,000 boe/d, although it is unlikely this capacity comes on ahead of this winter.

Implications for Oil Demand

Based on our estimates, there is at least 450,000 boe/d of oil demand which will come online this winter not being considered by the IEA and other oil analysts. This is likely conservative, as our estimate does not consider countries outside of Europe & Asia that may see gas-to-oil switching activity upside as well. In addition to installed capacity demand, there is additional ∼8MM boe/d upside from reactivation of retired plants and the conversion of operating generators to have dual fuel capacity.

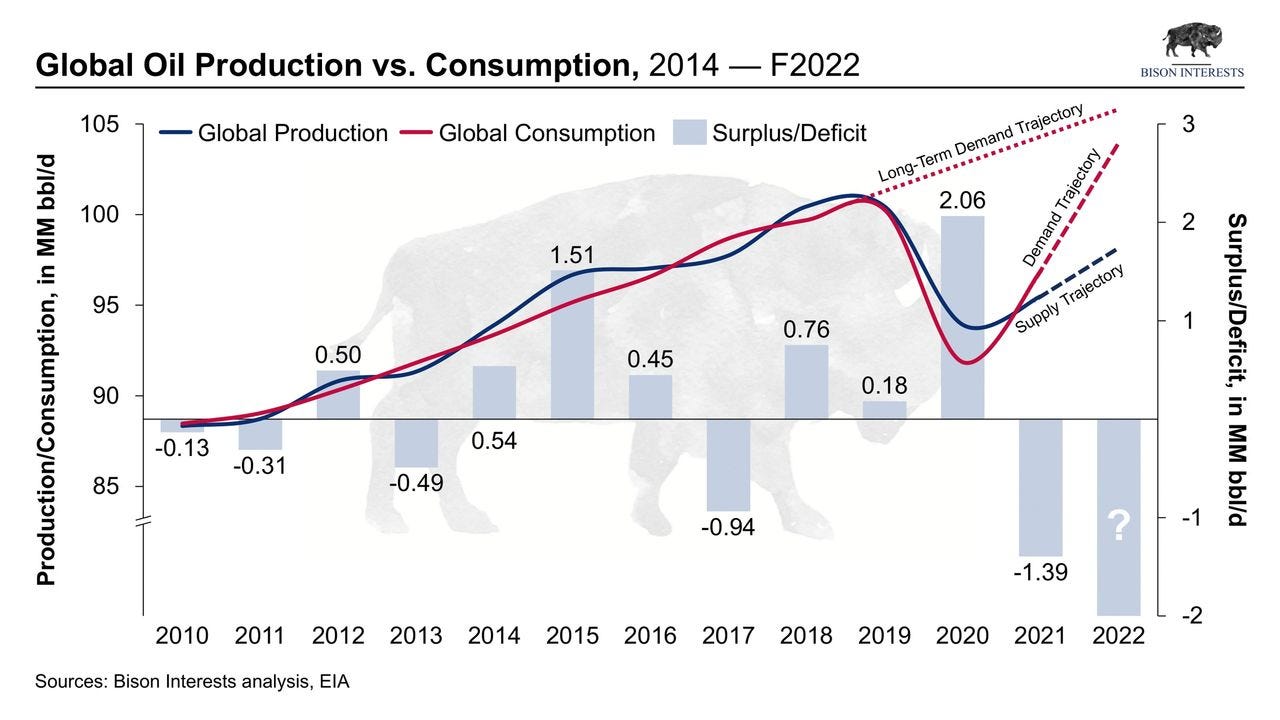

In the context of a very tight global oil market, 800,000 boe/d of oil demand at the low end is very material. This is particularly true as world oil markets remain in a structural deficit, which is projected to grow, and global inventories continue to be depleted as a result:

In 2021, global demand for oil was ∼97 million barrels per day. Our low-end estimate for gas-to-oil switching could rapidly increase global demand by 0.8, or almost 1% of total world demand. As the world oil demand continues to outpace production, supply deficits could widen further. In this scenario, small incremental changes in oil demand could have a disproportionately large effect on oil prices.

Looking Ahead

Despite their astronomical rise so far this year, there is little indication that European natural gas prices will fall back to pre-crisis levels anytime soon. Global LNG markets remain tight as Europe and Asia compete for limited export and vessel capacity, while exporting countries still have domestic demand to satisfy. And despite the ongoing energy crisis, there appears to be little political will for new investment in fossil fuels, with governments instead opting for “temporary” solutions such as reopening coal plants and delaying shuttering nuclear facilities.

While the energy crisis is unfortunately negatively impacting the global economy and the standard of living of millions of people, it is further boosting the previously depressed oil & gas industry. As European gas prices remain elevated, we may see higher natural gas prices here in the US as new export capacity is added, bringing more gas into the higher priced global market. And as European and Asian utilities and industries continue to substitute oil for natural gas, we may see elevated oil prices—and higher profitability for oil and gas producers.

Sources

[1] Source: BBC

[2] Source: European Commission

[3] Source: EIA

[4] Source: Reuters

[5] Source: SP Platts

[6] Source: Our World in Data

[7] Source: Bloomberg

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.