Good News for Western Canada: Excess Pipeline Capacity by 2023

Good News for Western Canada: Excess Pipeline Capacity by 2023

(Important Disclaimer at Bottom)

Nearly a Million Additional Barrels per Day

In January 2021, U.S. President Joe Biden announced that he is revoking previously-approved permits for the Keystone XL pipeline, originally planned to add 830 thousand barrels per day (Mbbl/d) of transport capacity from the oil sands of Alberta, Canada to Steele City, Nebraska. Many saw this action, along with the administration's ban on federal land drilling, as a sign that United States (and by proxy, Canadian) oil and gas operations will be under scrutiny from the Biden-Harris administration these next 4 years.

We’re here to let you know that Keystone XL’s cancellation will not materially affect Western Canada’s energy landscape. While there is some additional risk to Western Canada oil and gas from President Joe Biden’s climate plan, Keystone’s cancellation isn't expected to affect Canada's crude oil fundamentals. The region currently has plenty of rail transport capacity available as well as plans to bring nearly 1 million barrels per day (MMbbl/d) of additional transport capacity in the next two years (1) through pipeline and pipeline-expansion projects. In the first of our two-part series into Western Canada’s changing crude fundamentals, we're going to dive into the supply-demand balance, upcoming infrastructure, and the rationale behind higher WCS price forecasts from industry analysts.

Canadian Differentials

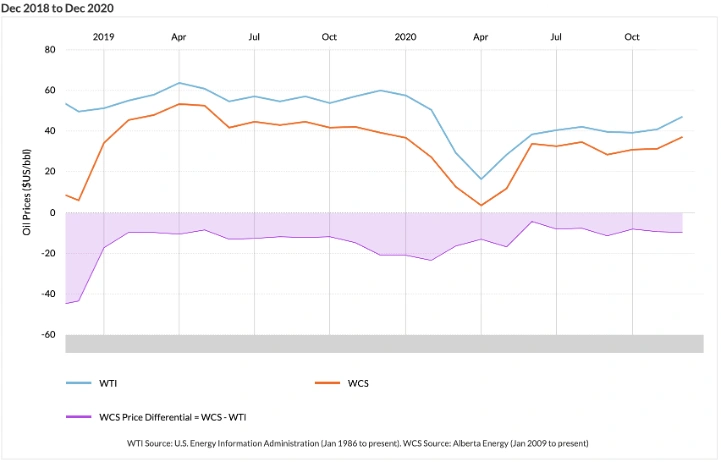

As we've mentioned in our Waha Hub white paper, we look at price differentials between regional hubs and their benchmarks because widening or narrowing of differentials is often an indicator of changing market dynamics. The price chart below shows Western Canada Select (WCS) against benchmark West Texas Intermediate (WTI) and their price differential over the last two years. WCS has historically been at a discount to WTI and at times priced at a very deep discount. Price blowouts are rare but have occurred previously, like in 2015 and 2018 when refinery shutdowns and transportation constraints became major negative externalities.

Source: EIA and Alberta Energy Regulator

On the chart we also see two instances where the differentials tightened substantially: once in January 2019 following Alberta’s provincial governments imposing of production limits, and again following 2020’s oil price crash. The 2019 production limits were imposed to stabilize dropping oil prices during a time of constrained transportation capacity. (2) Fortunately, this initiative was successful for Alberta and the WCS-WTI differential tightened considerably from over $43 in December 2018 to under $10 between February 2019 and June 2019. The differential stayed below $15 through November 2019.

The arrival of the COVID-19 pandemic and the 2020 Russia–Saudi Arabia oil price war had a large effect on oil prices across the world. In North America, WTI prices had fallen dramatically to below $30/bbl and the price of WCS had tumbled to an all-time low – below $5/bbl in early April 2020. Canadian producers were already dealing with transportation capacity issues but following COVID’s impact on WCS prices, many E&Ps were forced to cut capex and shut-in production in the region. Much like the Permian or Midcontinent, this major decrease in supply had led to the glut in the Western Canada clearing up last summer – supporting higher WCS prices and a tightening WCS-WTI differential.

Now as 2021 continues, differentials remain tight and Alberta has lifted production limits amidst forecasts of returning Canadian oil demand. Despite the additional production lifted limits will bring, evidence supports strong Canadian oil fundamentals in late-2021 and a much larger transportation capacity buffer than before – which can prevent transport-constrained price blowouts from happening again.

Canadian Oil Production in 2021 and Ahead

Western Canadian oil production was hit hard last year, reaching a low of 3.36 MMbbl/d in May of 2020. However, recent reports show the region has recovered to pre-pandemic production levels and most forecasts expect to see production reach all-time highs soon. A January 2021 RBN Energy report shows total crude oil production in Western Canada averaged 4.24 MMbbl/d for November 2020 and is estimated to average 4.3 MMbbl/d in December 2020. (3) This is nearly at pre-pandemic levels from February 2020, and is a substantial recovery from last year’s low of 3.36 MMbbl/d in May 2020. It’s safe to say that the region’s production levels have rebounded from the effects of COVID19.

Source: RBN

The industry consensus is that Western Canadian oil production will expand in 2021 and it will be a record year for Alberta’s oil sands production, due to the Alberta government’s removal of their 2-year long production limit (RBN, Reuters and S&P Platts).This will come primarily in the form of a 512 Mbbl/d increase in Alberta’s tar sands production in 2021 and the combined output from Canada’s other provinces, which is much smaller. RBN estimates that oil production in Canada will rise to a record-high 4.45 MMbbl/d this year, up from 3.9 MMbbl/d in 2020. This aligns with forecasts from major midstream operator Enbridge as well as S&P Platts, who both estimate a 500-600 Mbbl/d production increase in 2021.

Looking further ahead, RBN forecasts production reaching 5 MMbbl/d in mid-2022 and leveling out at 5.75 MMbbl/d past 2024. This is in line with the Canadian Energy Regulator’s (CER) high case “reference” forecast of reaching 5 MMbbl/d in 2022 and 5.5 MMbbl/d in 2023, but much more optimistic than CER’s updated “evolving” scenario which shows oil production growing slower and peaking at 5 MMbbl/d in 2035. (4) While production is expected to grow larger in the next few years, the available transport capacity is expected to grow much more significantly.

New Infrastructure Projects

It’s no secret that the majority of Canadian-produced oil is exported to the United States and most near-term production growth in Canada will be geared towards U.S. exports. According to Oil Sands Magazine, in 2021 there will be about 600 Mbbl/day of Canadian crude consumed in local refineries, and 4 MMbbl/day available as export supply. (5) And often it is not export demand that constrains Canadian oil and gas production but instead pipeline takeaway capacity constraints. The oversupply strains prices locally, however the severity was drastically reduced due to the sharp drop in prices due to the COVID-19 pandemic in 2020 and related decreases in E&P activity last year. This glut is now expected to flip into an undersupplied market as new pipeline projects are reaching the market in 2021 and 2022.

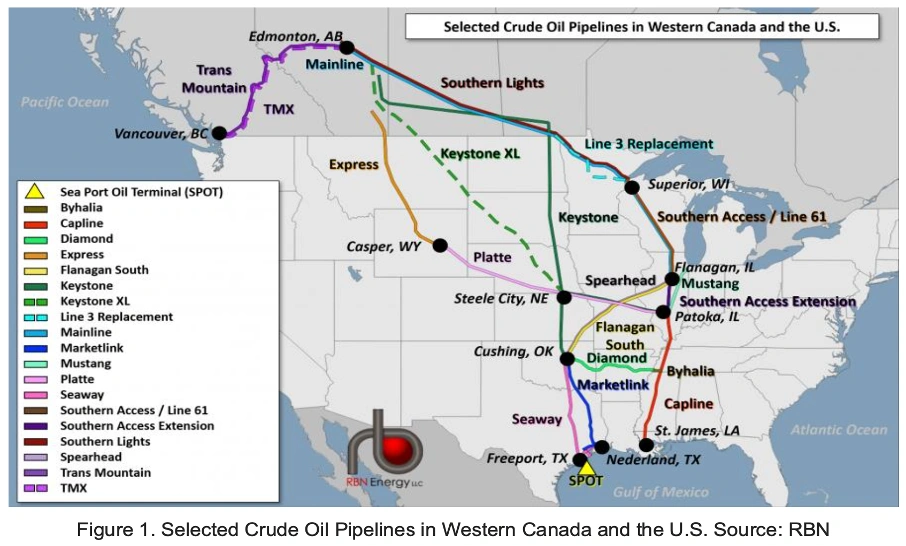

Source: RBN

Currently, Western Canada has about 3.8 MMbbl/day of crude oil export capacity and an additional 400 Mbbl/d in rail capacity, which exceeds current available export supply but only slightly. In total, nearly 1 MMbbl/d of transportation capacity is expected to come online by summer 2022 from the additional pipelines and debottlenecking plans we’ve outlined below:

Enbridge and TC’s debottlenecking plans will add 100 Mbbl/d of capacity in late 2021

Enbridge's Line 3 Replacement (L3RP) will bring 370 Mbbl/d of new capacity in the next year

The Canadian government-owned Trans Mountain Expansion (TMX) is expected to bring 590 Mbbl/d of additional pipeline capacity with target operation date in December 2022 (6)

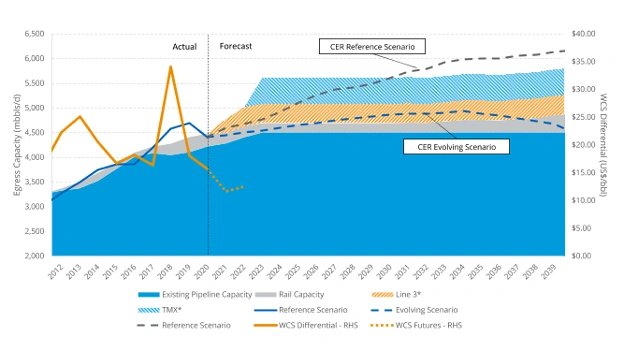

Jackie Forrest, executive director of the ARC Energy Research Institute, agrees with Bison’s view that production and export growth is supported by the upcoming pipeline infrastructure, stating that “both [TMX and L3RP] seem like they’re going to occur. If they do, then there’s probably ample takeaway capacity for some time out of Western Canada.” (7) Additional capacity growth beyond 2022 is possible as midstream companies continue to explore plans to bolt on expansions at current facilities. Below is a chart from the CER showing production out of Western Canada against available takeaway capacity, actuals and forecasted. We see that the Canada Energy Regulator forecasts that the capacity provided TMX and L3RP are sufficient to handle supply until around 2030 in their high-production scenario, and sufficient indefinitely in their low-production scenario.

Source: ATB Capital Markets Inc.

Risk to WCS

Following President Biden’s cancellation of the Keystone XL Pipeline project, there has been rising uncertainty surrounding cross-border projects between the US and Canada. In recent weeks there have been renewed and intensified efforts from activists to interrupt the construction of Enbridge Inc.’s Line 3 and Line 5, and Energy Transfer’s Dakota Access Pipeline (DAPL). While it is not likely, if this additional capacity does not reach the market the region will be at risk of another transportation constrained period. We will do a deep dive on the risks that these pipelines face and their likelihood of reaching commercial operation in part two of our Canadian oil and gas series.

Western Canadian crude prices are also subject to demand uncertainty around refinery maintenance. For example, BP’s 430,000 bbl/day Whiting Refinery in Indiana is the largest U.S. refinery purchaser of Canadian heavy oil in the country and also has a history of maintenance shutdowns in past years. A August 2015 shutdown of the refinery dented Alberta's oil exports and was partially to blame for the wide discount on Western Canadian Select that year, where WCS almost halved between early July and August 2015, falling to a 9-year low of $20 a barrel (at a ~$20 differential to WTI). Again in 2018 there was an outage at Whiting, except this time it lasted 2 months and was more severe. Here, the differential rose to as much as US $47 a barrel by the end of October 2018. We maintain that low-probability high-impact events like these could be a risk for WCS prices if this additional transport capacity does not come to market.

Price Forecast and Outlook

Much of our research has pointed to the idea that the lasting impact of COVID on the oil and gas industry will not be on demand, but rather supply. Once pent-up demand returns to North America in the form of energy use (as it has in countries like China and India), the additional transport capacity should be enough to support a tighter differential towards the end of 2021. However, investment levels do not seem adequate to support future demand and we expect crude prices to be on an upward trajectory in the coming years. Deloitte’s December 2020 Oil, Gas and Chemical Price Forecast concurs, stating “while overall supply and demand levels are lower than in 2019, the boost in global demand indicates a return to pre-pandemic behavior and this is reflected in stronger price forecasts for 2021.” (8)

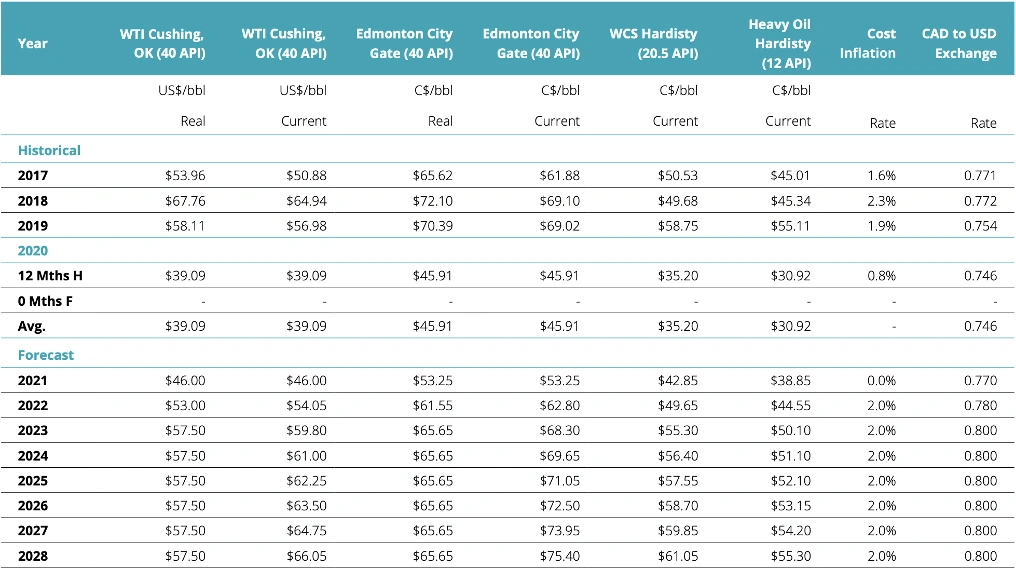

The below forecast from the same Deloitte report shows the price forecast for Canadian crude WCS, Edmonton Par, and WTI below. WCS Hardisty averaged $35.20 in 2020, and is forecast to average $42.85 in 2021 and $49.65 in 2022. This is a 21.73% year-on-year increase for 2021, and a 15.87% increase for 2022. The Edmonton Par averaged $45.91 in 2020, and is forecasted at $53.25 for 2021 and $62.80 in 2022. For the Edmonton Par, that is a 16% year-on-year increase for 2021 and a 17.93% increase for 2022. Both Canadian blends are expected to see continued price growth throughout the 2020’s, with prices for WCS and Edmonton Par forecast to reach $57.55 and $71.05 in 2025, respectively.

Source: Deloitte

Conclusion

For Canada, we see macro fundamentals changing in the next two years as there are higher levels of production and much, much more takeaway capacity coming. Not only are prices expected to track more in line with WTI but the environment may be less volatile as we have a much larger buffer of transportation capacity. This should drastically decrease the likelihood of price blowouts like those in 2015 and 2018.

Another reason the supply-demand balance and transport capacity is relevant is that we can better evaluate opportunities in Canadian E&P public equities. Canadian oil and gas equities have dealt with negative market sentiment in response to WCS-WTI differential blowouts. And still today, Canadian oil equities have not recovered as much as U.S. oil equities post-COVID, generally lagging behind in returning to prior valuations. This leaves opportunities in Canadian equities that are undervalued and have massive upside to the tightening oil market. As this commodity cycle continues, we will update our research, investment thesis and share our thoughts along the way.

Key Points

Production Output: Total output from Western Canada has returned to pre-pandemic levels and is forecast to rise to a record-high 4.45 million bpd in 2021, up from an average 3.9 MMbbl/d in 2020. Forecasts estimate there will be about 600 Mbbl/d of crude consumed in local refineries, and 4 MMbbl/d available to export in 2021. However, this production is far eclipsed by the upcoming transportation capacity being added.

Demand & Transportation Capacity: Demand outlook is higher due to additional energy demand from returning oil sands production, high levels of U.S. imports and forecasts of pandemic-related suppressed demand returning. The bottleneck here lies in transportation capacity, which should be alleviated as pipeline capacity increases by nearly 1 MMbbl/d in the next few years. Current pipeline transportation capacity is at ~4.2 MMbbl/d of transport capacity and there is 450+ Mbbl/d of pipeline capacity expected to come online in 2021, with another 500+ Mbbl/d of capacity by the end of Q2 2022.(9)

Price Outlook: Consensus forecasts that we’ll see higher WCS prices in a tightening market. Deloitte's most recent price forecast expects WCS prices to rise from an average of $35.20 in 2020, to a forecasted $42.85 in 2021, $49.65 in 2022 and $57.55 in 2025. Once additional pipeline capacity is added at the end of 2021, Canadian heavy differentials will likely be less volatile, and follow more in-line with WTI prices.

Important Disclaimer:

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Sources:

2. https://www.alberta.ca/oil-production-limit.aspx

4. https://www.cer-rec.gc.ca/en/data-analysis/canada-energy-future/2020/results/index.html

6. https://www.reuters.com/article/us-canada-pipeline-transmountain-idUSKBN29T0BA

7. https://news.yahoo.com/keystone-canada-record-oil-exports-us-193018933.html