Important Off-The-Run Metrics Indicate More Oil Opportunity Ahead

Important Off-The-Run Metrics Indicate More Oil Opportunity Ahead

(Important Disclaimer at the Bottom)

Opportunities in Oil Field Services

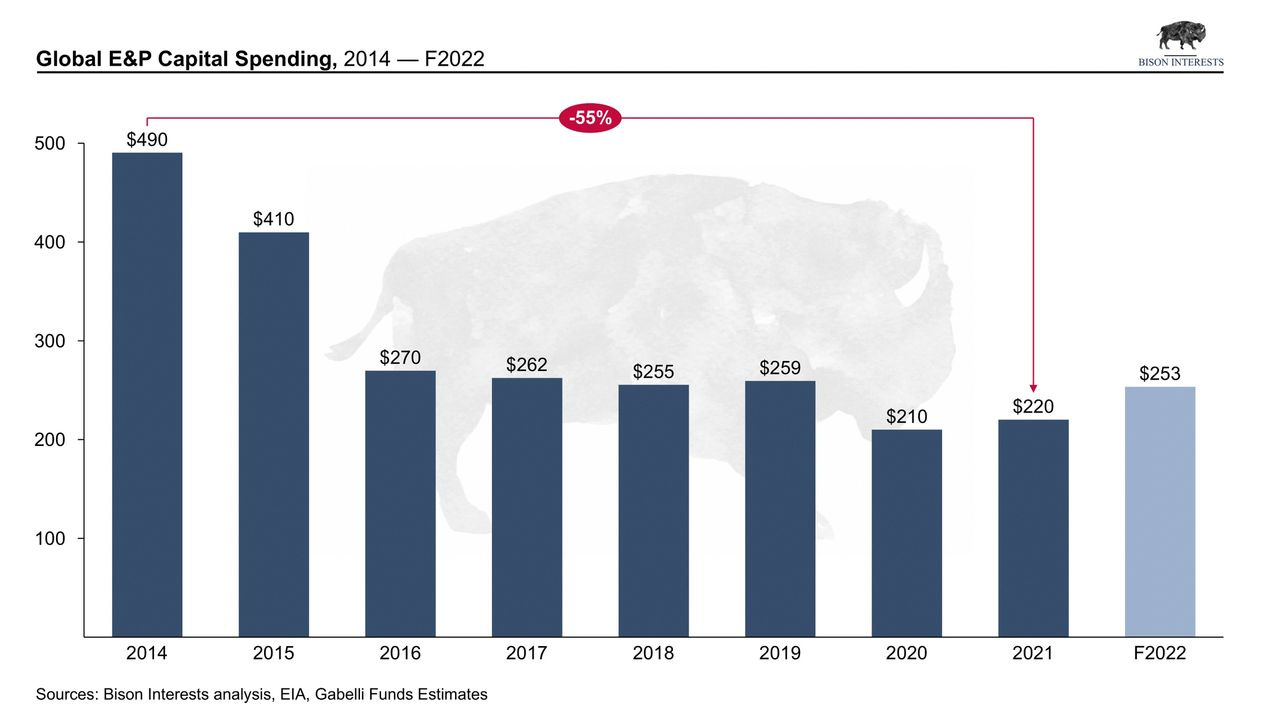

At Bison, we are constantly searching for: quality companies available at a steep discount to intrinsic value with multiple paths to re-rate to fair value, often likely to be helped by the macro backdrop. Today, several factors are coming into play to create a compelling backdrop for an oilfield activity boom. Oil prices are higher, energy and other commodity shortages are disrupting global economies and supply chains and drilled uncompleted well (DUC) inventories rapidly depleting to meet the shortfall in supply. These factors raise the prospect of an increase in drilling and exploration activity. Soaring gas prices are reverberating across supply chains and hurting the middle class, shifting the narrative and priorities of politicians, virtue-signalling CEO’s and media to energy supply security and lower oil and gasoline prices, a contrast to “ESG” considerations.

With world oil and DUC inventories depleting, and limited OPEC+ spare capacity to bring to market, the only way to increase supply and lower prices is to drill new oil and gas wells and stimulate new production. This is obviously bullish for oilfield services companies (OFS). These provide support to E&P’s by providing critical equipment & infrastructure, such as drilling rigs and pressure pumps, chemicals & labor. April 2020 was likely a cyclical trough in OFS activity, along with the broader oil and gas industry. Despite having rallied significantly from their lows, there remains a significant opportunity in oil and gas equities, and OFS companies particularly, as they catch up to oil and the broader market:

Energy Crisis Update: Energy Market Dislocations & Bison Opportunity

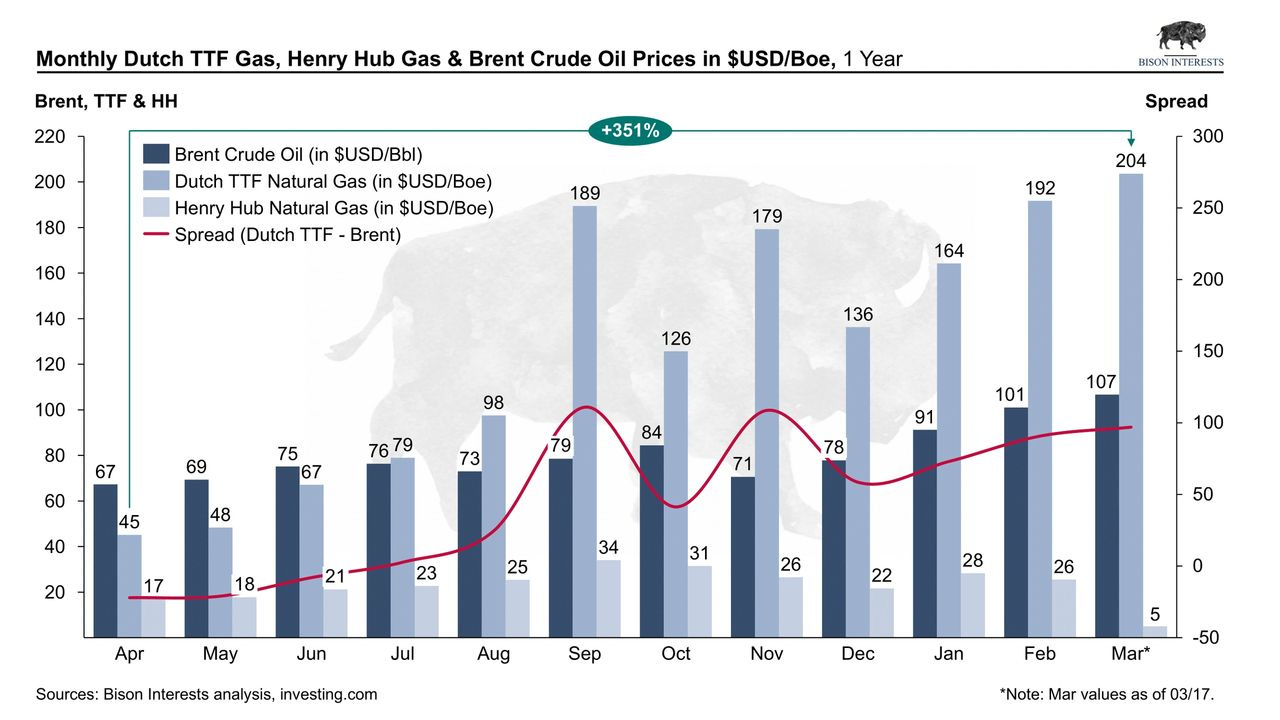

Since our November 2021 white paper, Bison: Reliable Energy Research in a Rapidly Shifting Landscape, energy markets have continued to evolve. The energy crisis in Europe continues to unfold, and Dutch TTF gas prices rose beyond 2021 highs, likely due to a risk premium and potential shortages of gas resulting from the ongoing conflict in Ukraine. Note that Russian gas currently accounts for 40% of the EU’s consumption [1].

The ongoing energy crisis is the culmination of years of underinvestment across the oil and gas value chain, combined with bad energy policy, ESG activism and divestment. While energy prices have undeniably been lifted by the ongoing crisis in Eastern Europe, underinvestment in energy supply security were bound to lead to shortages and soaring prices eventually. The current conflict is an unexpected, short-term tailwind; oil and gas prices could correct sharply in the event of a negotiated peace, but will likely rise further over time due to longer term factors.

While higher energy prices are a major tailwind for oil and gas equities, they are a bad spell for the broader economy: they disproportionately hurt the poor and middle-class, and they stoke already white-hot broader price inflation. However, soaring energy prices are an early manifestation of a larger under-supply issues and are likely to persist. This may drive additional energy market dislocations, along the lines of those that we previously identified and addressed.

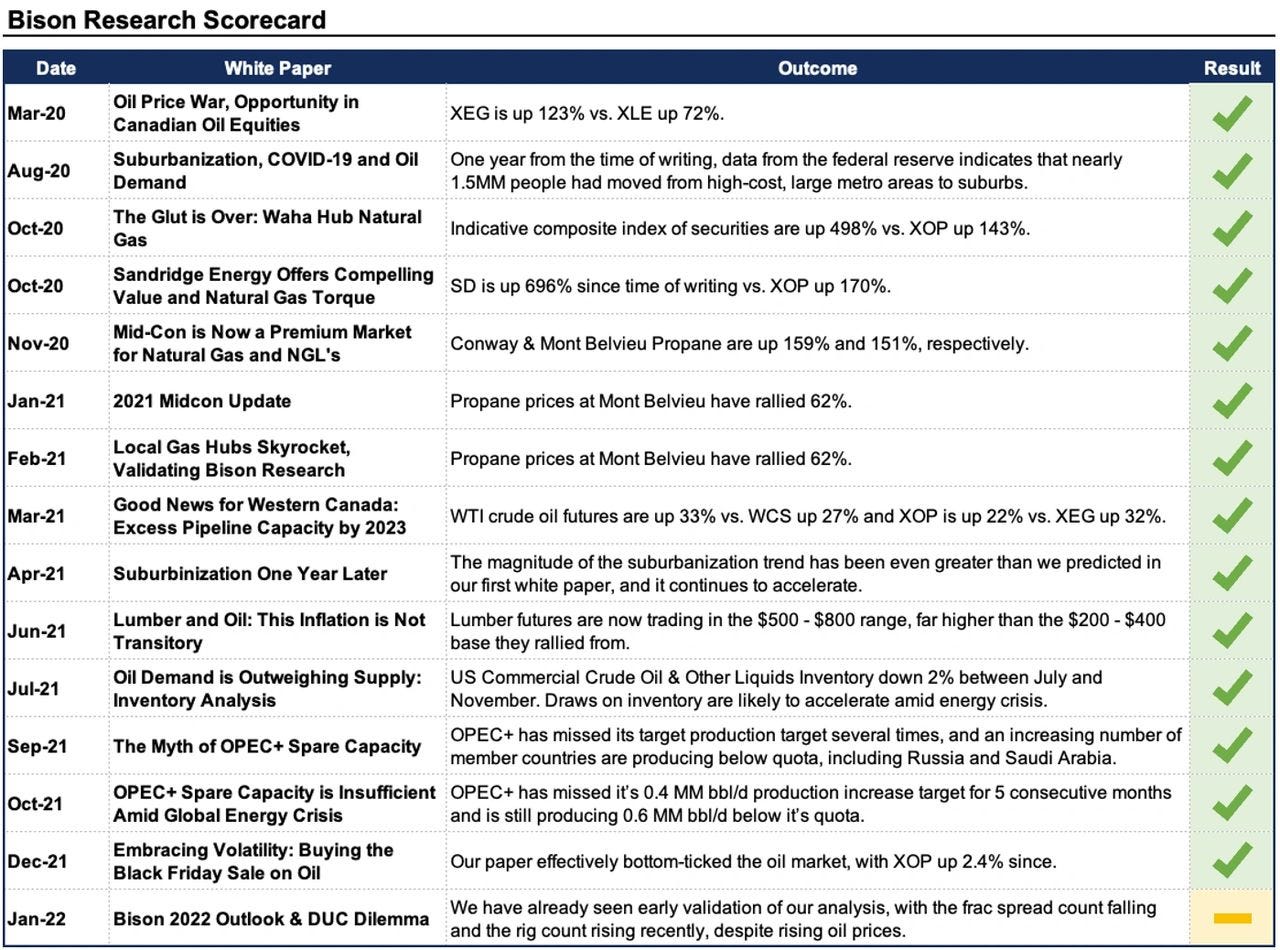

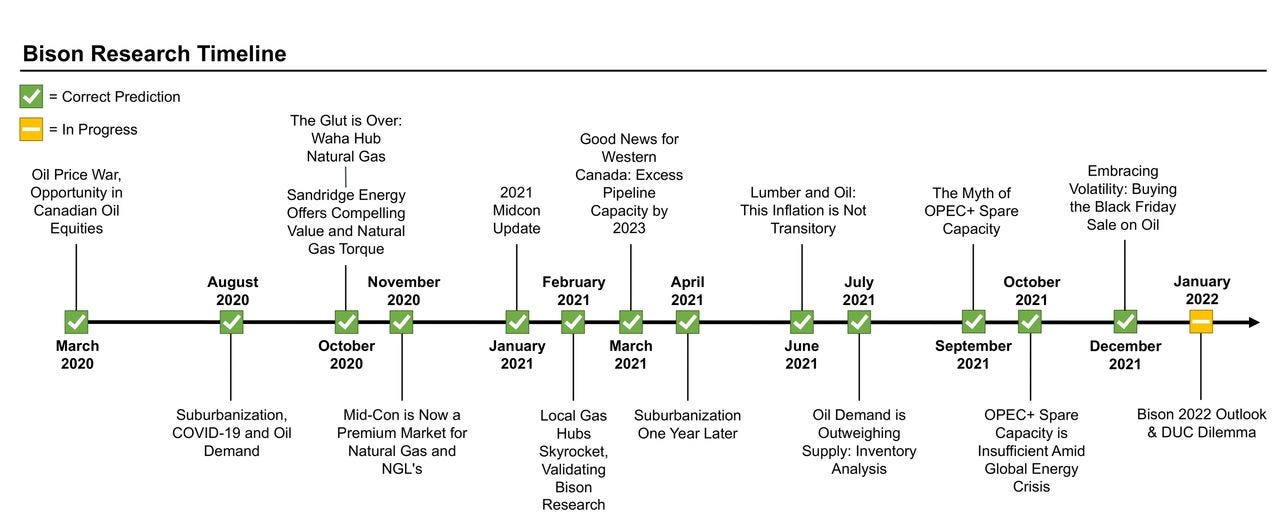

In that context, it is timely to review to review the performance of Bison’s white papers since last November. Some of the factors identified here are ongoing drivers of oil prices and merit a watchful eye and regular updates to better understand the oil market:

OPEC+ Spare Capacity

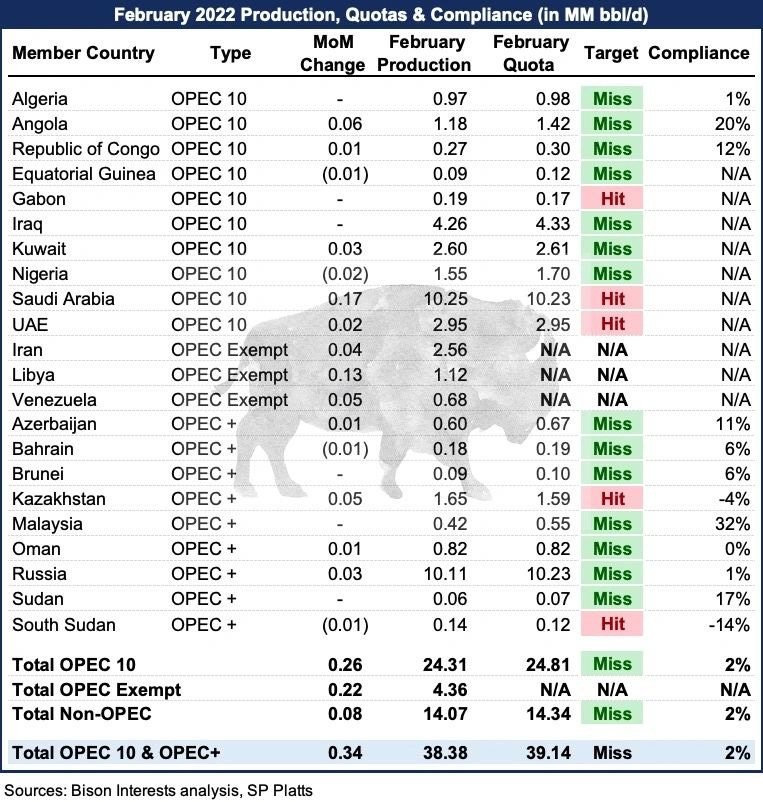

In our September 2021 white paper, The Myth of OPEC+ Spare Capacity, we contended that OPEC+ spare capacity was markedly overstated. We showed that Russia and Saudi Arabia—the cartel's largest producers—were likely exploiting opaque reporting requirements and definitional nuances to overstate spare capacity. Declining capital expenditures, large draws from onshore inventories and production levels nearing OPEC+ targets were signs that Russia & Saudi Arabia were approaching full production capacity.

In our October follow-up piece, OPEC+ Spare Capacity is Insufficient Amid Global Energy Crisis, expanded on our analysis and suggested that OPEC+ cartel has anywhere from 3.8MM – 5.2MM bbl/d in spare production capacity. In the context of the nascent energy crisis, we had argued that this could propel energy prices higher as demand grows faster than supply, and the OPEC+ is unable to fill the shortfall in the same way it had previously.

When we first published these papers we received a lot of pushback, often from self-proclaimed industry” experts”. They argued that we were unqualified to make such an assessment, especially with limited access to reserve reports and no boots on the ground in Saudi Arabia. As subsequent monthly data has come in, it has become exceedingly clear that OPEC+ has less spare capacity than stated. They have now missed their target production for several consecutive months, and continue to produce below their aggregate quota:

There have been early non-production data indicators confirming this as well. In October 2021, ex Saudi Aramco EVP Sadad Al-Husseini said that the OPEC had no more than 2.5—3MM bbl/d of spare capacity. Additionally, the IEA has been continuously revising their estimate of OPEC+ spare capacity. In June 2021, they warned that OPEC+ spare capacity could fall to 5MM bbl/d, an estimate which they revised down from 4MM bbl/d in October 2021[2]. In February 2022 the IEA once again made an adjustment, warning that the cumulative production shortfall from target could have amounted to over 1B bbls since 2021[3]. This came as no surprise to Bison, which has been monitoring OPEC+ production misses for over consecutive months in 2021:

Embracing Volatility

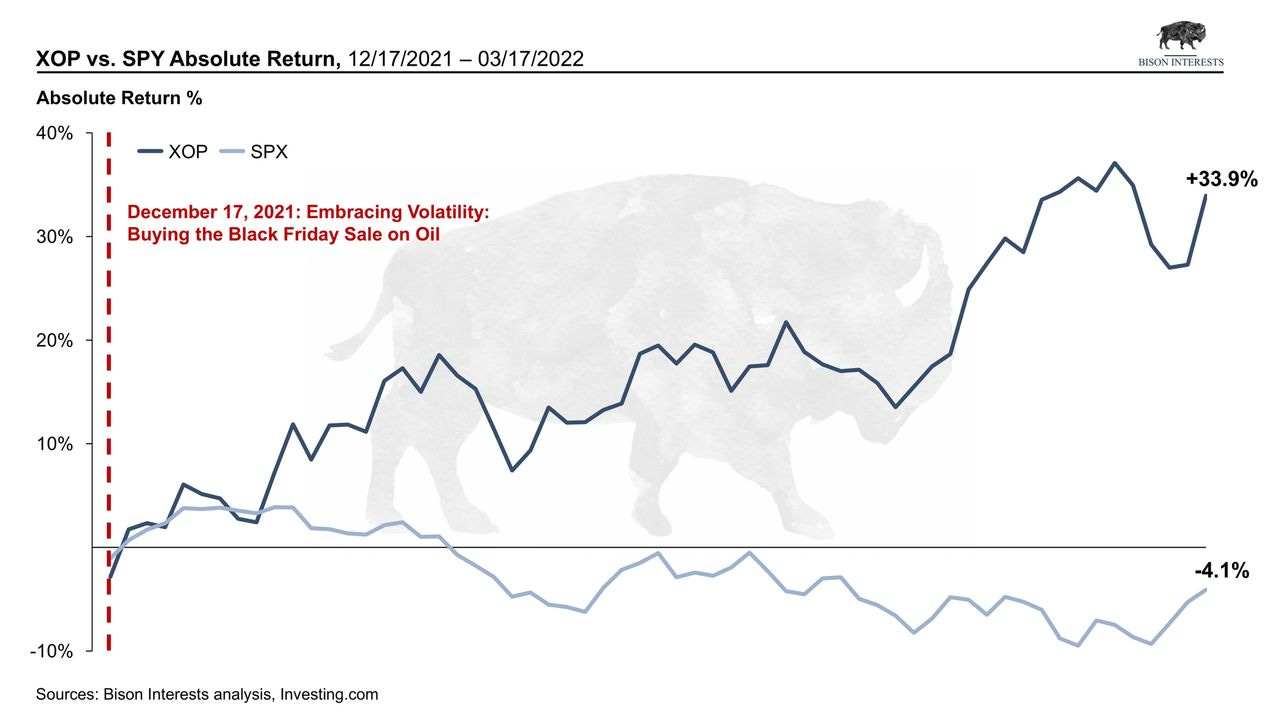

November 2021 was a turbulent month for oil and gas equities. On the Friday after Thanksgiving, there was a 12% drop in the price of oil on news of the rapid spread of novel “Omicron” variant, and its possible dampening effects on oil demand. In our December 2021 paper, Embracing Volatility: Buying the Black Friday Sale on Oil, we argued that the long-term oil bull thesis was intact, and that this short term weakness posed a significant a buying opportunity. While many were selling off oil and gas equities and some pundits were even calling for a top in oil, we were buying aggressively as cyclically and structurally cheap equities became even more attractive.

Bison’s edge is in buying quality oil and gas company’s shares at discounted prices and holding them through significant volatility. Part of our investment philosophy is to embrace this volatility, and in this case, we saw the correction in oil and gas equities as an opportunity to re-visit the long-term oil thesis and re-affirm our conviction, while many market participants were panic selling. Bison’s paper essentially “bottom ticked” the correction! Since publication through March 17, 2022, XOP is up 33.9% vs. the SPX down 4.1%:

Bison 2022 Oil Outlook & DUC Dilemma

In our January 14th 2022 paper, Bison 2022 Outlook & DUC Dilemma, we suggested that the confluence of “ESG” mandates by investment allocators & hostility towards oil and gas by policy makers, the lack of capital available to the industry, and depressed drilling and production levels and rising demand were likely to lead to much higher oil prices in 2022. We espoused this view at a time where oil had already seen a massive 58% rally in 2021, and many market participants felt that oil prices were unsustainably high and due for a massive correction; some were even shorting oil futures outright.

WTI oil is subsequently up 43.7% in just 2 months of 2022, driven by predicted world oil supply disappointments and higher demand, and helped along by geopolitical risk:

While much higher oil prices would traditionally incentivize new production and quell rising prices, we argued that this time may be different. For one, “ESG” concerns and restrictive government policy are putting a cap on drilling activity, and thus the decision to increase production is no longer economically motivated. Consequently, the supply deficit is likely to widen as demand grows and supply begins to dwindle as existing wells are depleted, putting further pressure on prices.

As we discussed in our identification of the oilfield services opportunity above, oil companies are warming up to the idea of increased capital expenditures and new drilling – despite this, looming supply deficits are unlikely to be resolved anytime soon. As we have identified across letters and white papers over time, underinvestment has plagued the oil and gas industry for some time now. This under-investment has been particularly in oil field services. Due to logistical problems in the oil and gas supply chain, shortages of critical materials, a drastic reduction in the pool of skilled labor in the industry and the general lack of available capital, these issues may take years to unwind and lead to much higher prices in the interim:

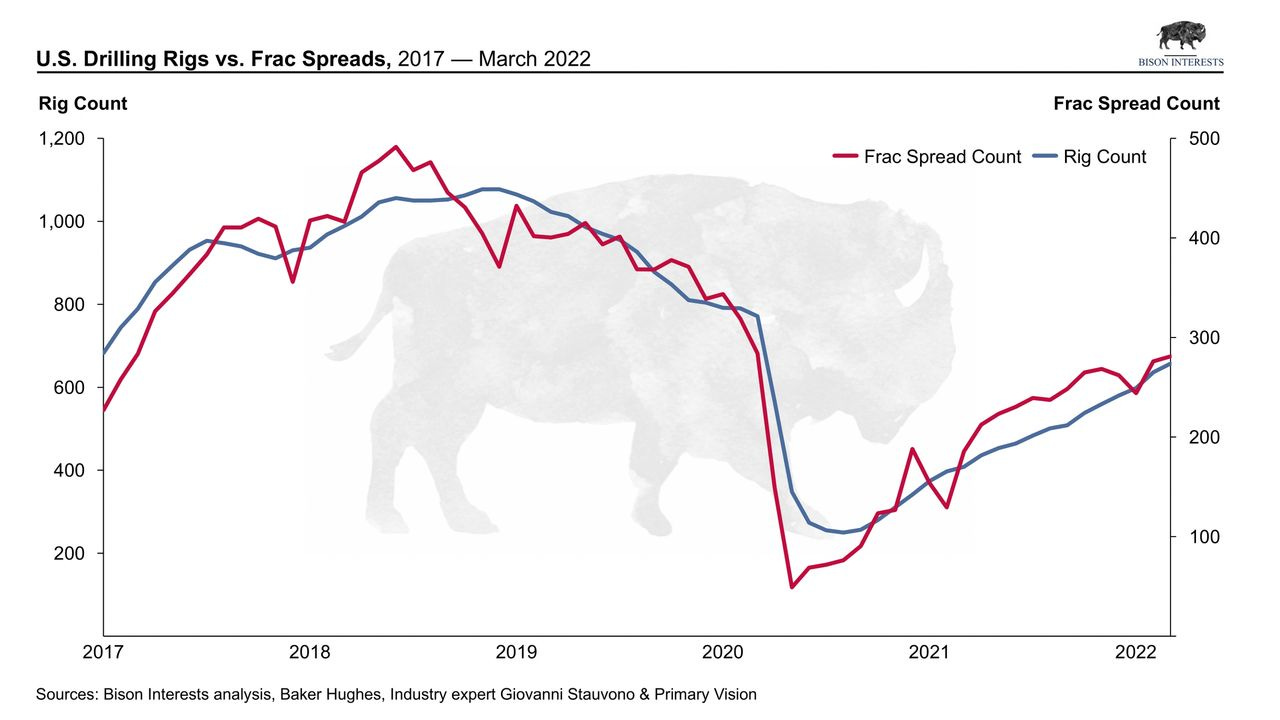

While drilling levels remain depressed compared to previous cycle highs, oil demand has remained strong. Consequently, the industry has been rapidly completing its inventory of drilled uncompleted wells (DUCs) to hold production flat. As mentioned in our white paper, DUC’s are a form of oilfield working capital and allow E&Ps to maintain production with less capital investment—so long as there is an inventory of DUC’s left to be completed. Since the onset of the pandemic, DUC inventory has fallen dramatically, and this trend has accelerated since our paper in January:

The supply of rigs and frac spreads used for well drilling and completion can be a leading indicator of DUC inventory changes. We argued that there is an optimal ratio of frac spreads relative to drilling rigs needed to keep DUC inventory flat, and given the rapid depletion of DUC inventory, rig counts were likely to rise materially while frac spreads were likely to fall. Since the time of publishing, the US has added 56 rigs while the frac spread count has been roughly flat, and the frac spread/drilling rig ratio has fallen from 0.53 to 0.43:

Reliable Research Ahead of Headlines

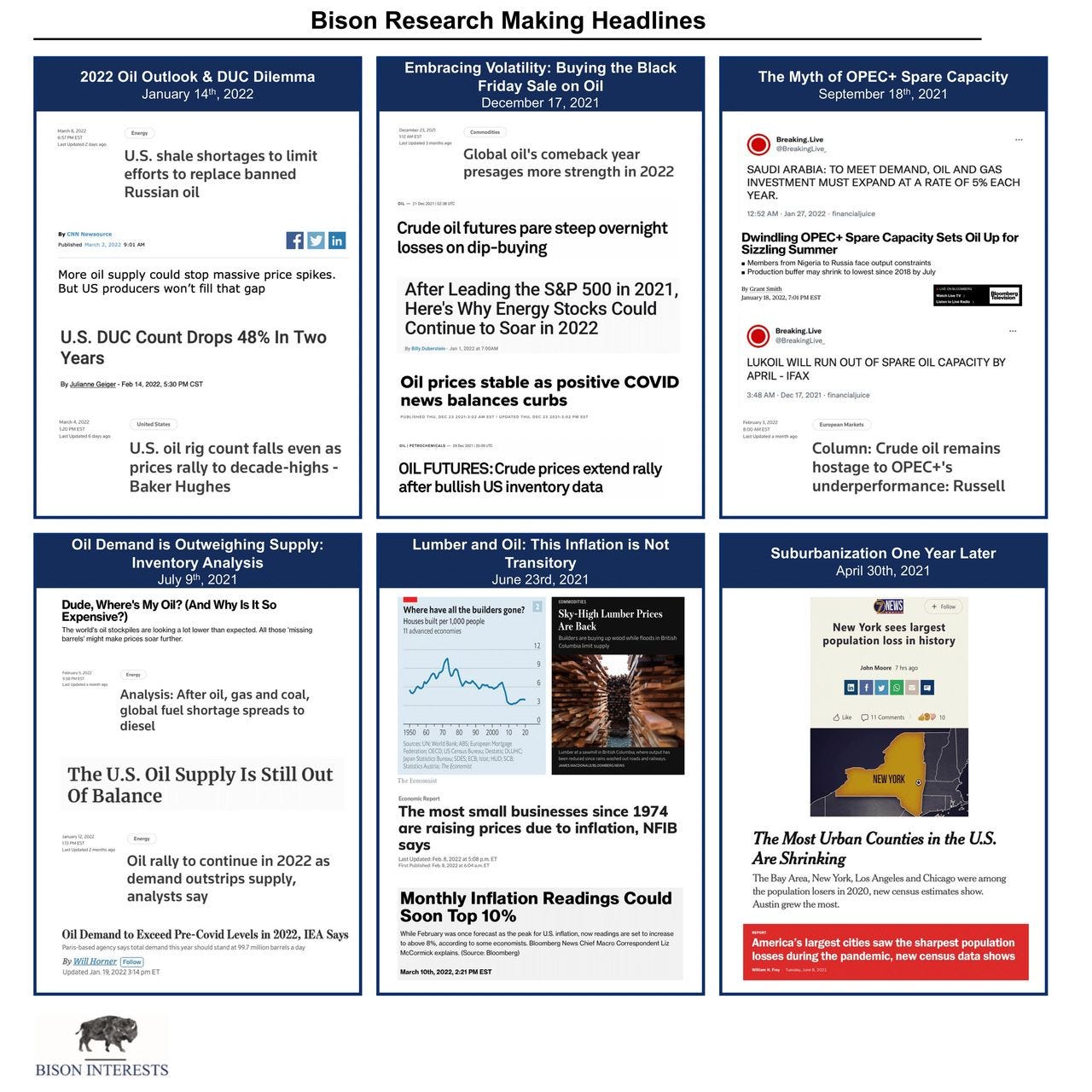

Bison has become well-known for putting out contentious research. While we often receive pushback at the time of publishing, our views have tended to become mainstream as new information surfaces and is recognized by market participants. This consensus ultimately makes it to news headlines, as can be seen below:

While it can be frustrating to see Bison research findings in mainstream news articles several months later, often without citation or recognition, this also serves as an external source of validation for our contrarian analyses. When topics addressed in Bison white papers make it to front-page news headlines, they often have become the consensus view and have ”worked.” Bison has been sharing its research and publishing white papers for almost 2 years now, and we’re proud of our track record to date:

The Bison Methodology: Differentiated Research, Variant Views, and Superior Outcomes

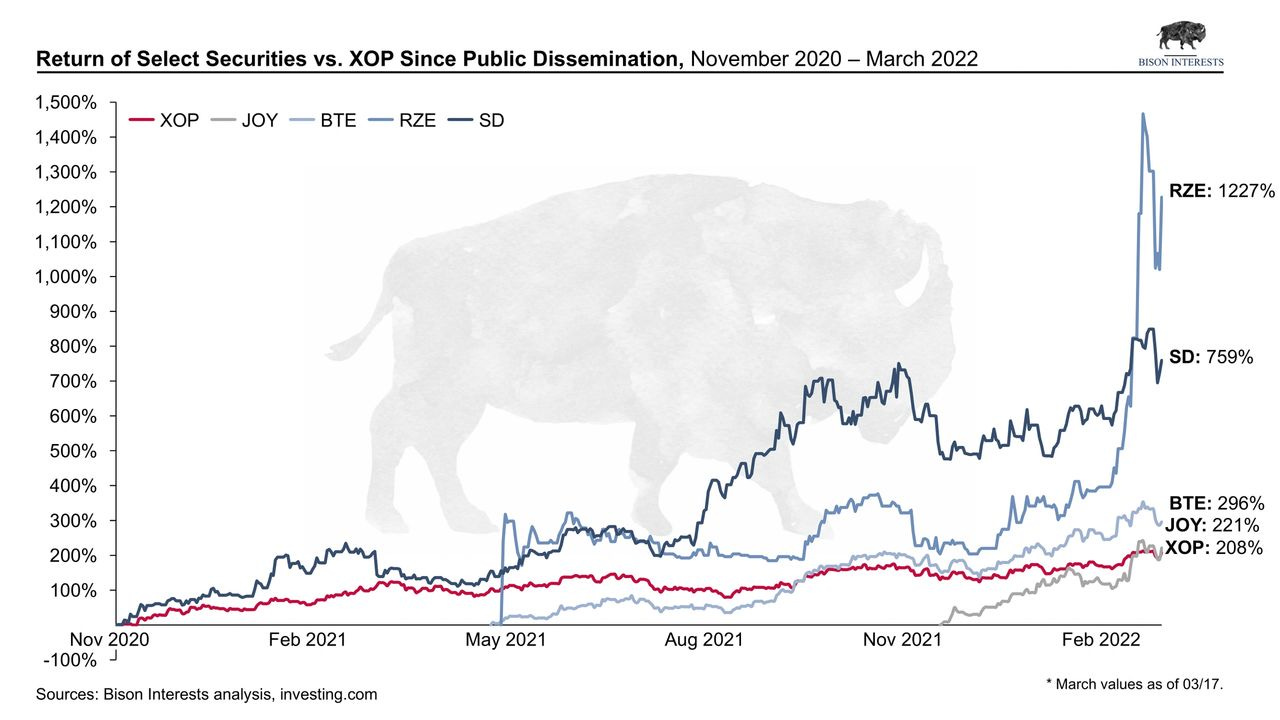

Bison’s investment philosophy is simple: we buy deeply undervalued oil and gas securities with high quality assets, proven management teams, and at least one additional catalyst likely to lead to a re-rate. Once a security has met our stringent investment criteria, we buy it in size and hold it through significant volatility while we wait for oil prices to rise, catalysts to materialize and the security to re-rate higher. To date, we have done so with resounding success. And this success can easily be tracked through the performance of publicly traded companies that we have disclosed ownership of and discussed in publicly available media. Here is a chart illustrating that over the past ~18 months and comparing that performance to the oil equities ETF XOP:

While our investment philosophy is simple, the research that leads to superior security selection is rigorous and nuanced. We look for opportunities in areas of the market that are often overlooked, potentially due to lack of analyst/expert coverage, overwhelming negative sentiment from investors who have previously lost money in the space, or for non-economic reasons, such as ESG mandates. This differentiated research approach inevitably leads to variant views, which often contradict the consensus views adopted by industry “experts”. We are happy to share this research with you, and have found that the continued tracking of important, under-followed indicators can provide differentiated insight into the broader oil and gas markets as well as niche sub-markets.

Sources

[1] Source: Reuters

[2] Source: Reuters

[3] Source: Bloomberg

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Share this post: