Mid-Con is Now a Premium Market for Natural Gas and NGLs

Mid-Con is Now a Premium Market for Natural Gas and NGLs

(Important Disclaimer at Bottom)

Introduction to the Mid-Continent Region

Stretching across Oklahoma, Kansas, and the Texas Panhandle is an oil and gas region that goes by many names: the SCOOP/STACK, the Mid-Continent region, or simply mid-con. The mid-con region, while not officially defined, is generally understood to reference the Fayetteville, Woodford, and Cana Woodford shale gas plays in the Arkoma Basin, Ardmore Basin, and Anadarko Basin. Much like the Permian Basin, technological developments, including horizontal drilling and multi-stage fracture stimulation, have brought significant production and economic development to the mid-con region in the past decade.

At the heart of the mid-con oil and gas industry is Conway, Kansas. This city contains key natural gas liquids (“NGL”) production, transportation, and storage facilities for the Midwest. The Conway hub is the second largest NGL hub in the U.S. after Mont Belvieu. Unlike the Mont Belvieu hub, the Conway hub is a transit hub. A transit hub is a key transit or trans-shipment point that facilitates the transport of hydrocarbons, and in this case, NGLs. Thus, the Conway hub not only serves Midwest demand but also transports fuel supplies for much of the Midwest industrial and consumer NGL markets.

From the Conway hub, “propane is sent north to meet highly seasonal demand ranging from crop drying (Midwest) to home heating (Midwest and Northeast), or south to satisfy Gulf Coast petrochemical and export demand; butanes move to Conway from producing regions and Midwest refineries, and are either stored to satisfy seasonal demand for gasoline blending in the region or shipped to the Gulf Coast for export or in-region consumption; ethane also either passes through Conway on its way to the Gulf Coast, where it is consumed as a petrochemical feedstock or exporter or to Midwestern petrochemical plants as a feedstock.” (1) The Conway hub's immediate vicinity does lack local demand for NGL processing or end use, but the Conway hub’s interconnectedness with Midwest demand centers, mid-con and Rockies production, and the Gulf Coast NGL complex make the Conway hub central to North American NGL logistics.

Mid-Con Production since COVID-19

Oil and gas production declined dramatically across the United States in response to the oil price collapse in March 2020. In the following months some regions like the Permian and Bakken resumed a portion of their production activity, however production is still far below pre-COVID output. Even so, natural gas and liquid hydrocarbon production near the mid-con region in Oklahoma hasn’t rebounded nearly as much as production in other U.S. regions. For example, in the Anadarko region, natural gas production surpassed 8,000 million cubic feet per day (“MMcf/d”) for the first time in October 2019. By October 2020, production fell to 6,382 MMcf/d. For reference, October 2017 production was at 6,476 MMcf/d—two years of steady growth were wiped out in one year. November, natural gas production is expected to fall by another 130 MMcf/d.

Source: EIA October 2020 Drilling Activity report

Oil production in the region peaked in 2019 as well—before COVID-19 reached U.S. soil. Since reaching a high in the third quarter of 2019, Anadarko oil production remained around 500–600 Mbbl/d before plunging below 400 Mbbl/d in spring 2020. Since then, oil production rebounded by a fair amount before falling again in winter 2020. Anadarko oil production in October was 423 Mbbl/d, and there are 18 active rigs, which is 40 less than one year ago.

NGL and Natural Gas Prices at Conway

The effect of COVID-19 is reflected in the chart below of mid-con natural gas spot prices. In April 2020, prices dropped below $1.00/MMBtu. This drop was followed by a relatively quick rebound to pre-COVID-19 prices, and then prices settled around $1.35–1.65 range. Since the first week of October, mid-con natural gas prices have rallied substantially: they surpassed $3.00/MMBtu in the last week of October 2020. We attribute this to flat production in the region along with natural gas and NGL storage and demand developments, which are addressed later in this article.

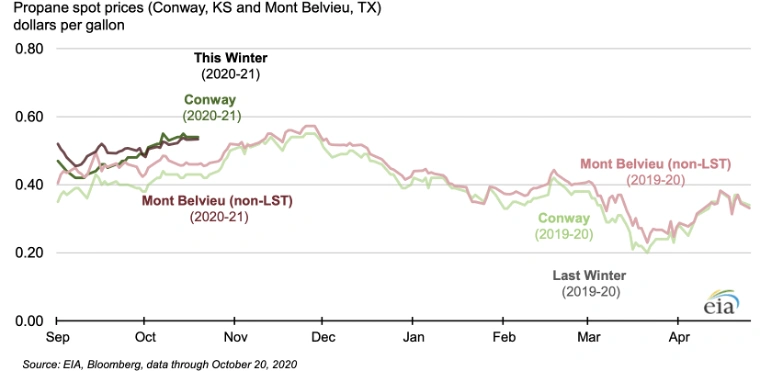

Part of the recent rally in mid-con NGL values is from the strength of propane pricing at Conway in the last month. The chart below depicts the propane prices between Mont Belvieu and Conway between August and October 2020. From mid-September to mid-October, Conway propane closing prices increased by 13.25 cents, a 32% gain in value. This rally was strong relative to the more modest increases in Mont Belvieu and crude oil prices.

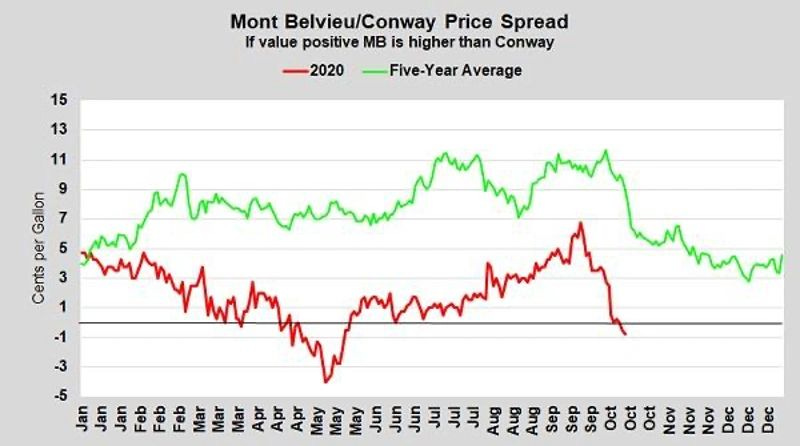

The chart below compares propane spot prices at Conway and Mont Belvieu from August through October 20, 2020. Conway spot prices consistently remained below Mont Belvieu prices, before overtaking it near the $0.50 range in October 2020. Interesting details emerge when we plot the 2020 Conway/Mont Belvieu spread against the 5-year average spread between the two.

The chart below shows us exactly that, where if the value is above the black line, Mont Belvieu LST is holding the premium over Conway and when the value is below the black line, Conway is valued higher. We see that the spread between Mont Belvieu and Conway was much wider over the past five years than it is today. In the 5-year average, Mont Belvieu was more than 7 cents above Conway in non-winter months consistently. This is a deep contrast to September and October of 2020, where the basis collapsed and Conway emerged with a slight premium in price mid-October. This is a rare occurrence, happening once earlier during the oil price collapse and again now. Considering that this is a major shift away from the average spread for the last 5 years, we look to recent changes in the market to help us better understand the change in relative price.

Source: Cost Management Solutions

Recent Developments in Supply/Demand Dynamics and Outlook

Conway’s value relative to Mont Belvieu LST generally improves this time of year, but got an early start, possibly due to early crop drying and an earlier bout of colder temperatures according to a recent LPGas Magazine article. This LPGas article also dives deeper into other supply and demand developments contributing to the recent strength in mid-con prices, summarized below.

Essentially, there is a propane movement east that is tightening supplies for the mid-con region. Additional pipeline capacity and more options for Canadian producers to export their propane production led to less propane imported into the mid-con region. Canadian producers began exporting propane by rail to Mexico a few years ago and added the ability to ship waterborne exports to Asia in the last two years. According to the article, the mid-continent is becoming the last resort destination for Canadian exports. This has led mid-con propane inventories to be under expected levels, while East Coast propane inventory has set new five-year highs almost every week in October. (5) Data shows that U.S. Midwest inventory is currently 469,000 barrels, 1.7% below last year. Inventory on the East Coast is currently at 2.505 million barrels – or 35.6 percent higher than this time last year. (5)

Rusty Braziel, founder and CEO of RBN Energy, spoke at a National Propane Gas Association webinar in July 2020. He spoke at length about how while most are aware of the decline in crude and natural gas production due to demand destruction from the virus, he feels that much fewer are aware of the changing propane export dynamics. Braziel told participants that “COVID-19 and declines in natural gas and crude production are factors [in the supply picture] this year as well as more propane exports going out of British Columbia on the west side of the U.S., and Pennsylvania on the east side of the U.S. These are new factors that retail propane marketers need to be aware of this year. These factors could put a squeeze across the supply/demand equation, especially if we have a cold winter.” (6)

Dwindling NGL supply in the Midwest, along with demand-related factors are core elements in the narrowing spread between Conway and Mont Belvieu values. Reflecting strong demand and forecasted below-normal temperatures, Conway propane spot prices are now at a premium to Mont Belvieu spot prices. As we look ahead, the EIA is estimating 5 percent more heating degree-days this winter and 14 percent more propane demand due to a colder winter plus the impacts of COVID-19-related quarantines. With winter approaching quickly, there are concerns that local market supply shortages could occur during high winter demand periods.

Key Points

• Associated natural gas production in the U.S. “mid-con” region has not rebounded from the oil price collapse as much as other U.S. regions. For example, in the Anadarko region, natural gas production surpassed 8,000 million cubic feet per day (“MMcf/d”) for the first time in October 2019. By October 2020, production fell to 6,382 MMcf/d. For reference, October 2017 production was at 6,476 MMcf/d—two years of steady growth were wiped out in one year.

• Due to structural changes in the propane market, mid-con propane inventory has been lower than usual while East Coast propane inventory set new five-year highs almost every week in October. Additional options for Canadian producers to export propane production has led to less propane imported into the mid-con region. (5) This movement east is tightening mid-con supply and has been a core element in the narrowing spread between Conway and Mont Belvieu propane basis differential.

• The supply deficit and developments in the mid-con propane market have recently driven up basis prices at regional hubs. Since the first week of October,mid-con natural gas prices have rallied substantially, to above $3.00/MMBtu in the last week of October 2020. Conway, Kansas propane spot prices are now at a premium to MontBelvieu at $0.53, reflecting strong demand and below-normal forecasted temperatures.

Important Disclaimer:

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Sources

https://www.energy.gov/sites/prod/files/2018/12/f58/Nov%202018%20DOE%20Ethane%20Hub%20Report.pdf

https://www.lpgasmagazine.com/conway-gains-in-value-relative-to-mont-belvieu/

https://www.naturalgasintel.com/data-snapshot/daily-gpi/MCWNGPL

https://www.eia.gov/special/heatingfuels/resources/Propane_Briefing.pdf

https://www.eia.gov/special/heatingfuels/resources/Propane_Briefing.pdf