Narrative Inversion: Canadian Publicly Traded Oil Company Sells Shale Asset at a Premium to a Private Equity Backed Company – More O&G M&A to Come

Narrative Inversion: Canadian Publicly Traded Oil Company Sells Shale Asset at a Premium to a Private Equity Backed Company – More O&G M&A to Come

Athabasca Oil Corporation (TSX: ATH) recently announced its disposition of non-core light oil assets in the Montney and Duvernay shale plays to a private equity backed buyer. The total net production sold was 2,925 boe/d, for a total consideration of $CAD 160MM (subject to some closing adjustments).

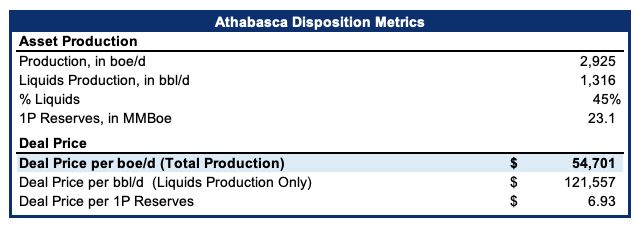

Athabasca Disposition Overview

We estimate these assets transacted at $CAD 54,700 boe/d ($USD 41,195), and the seller estimates a sale multiple of 7.9x net operating income. Some of the deal metrics can be seen below:

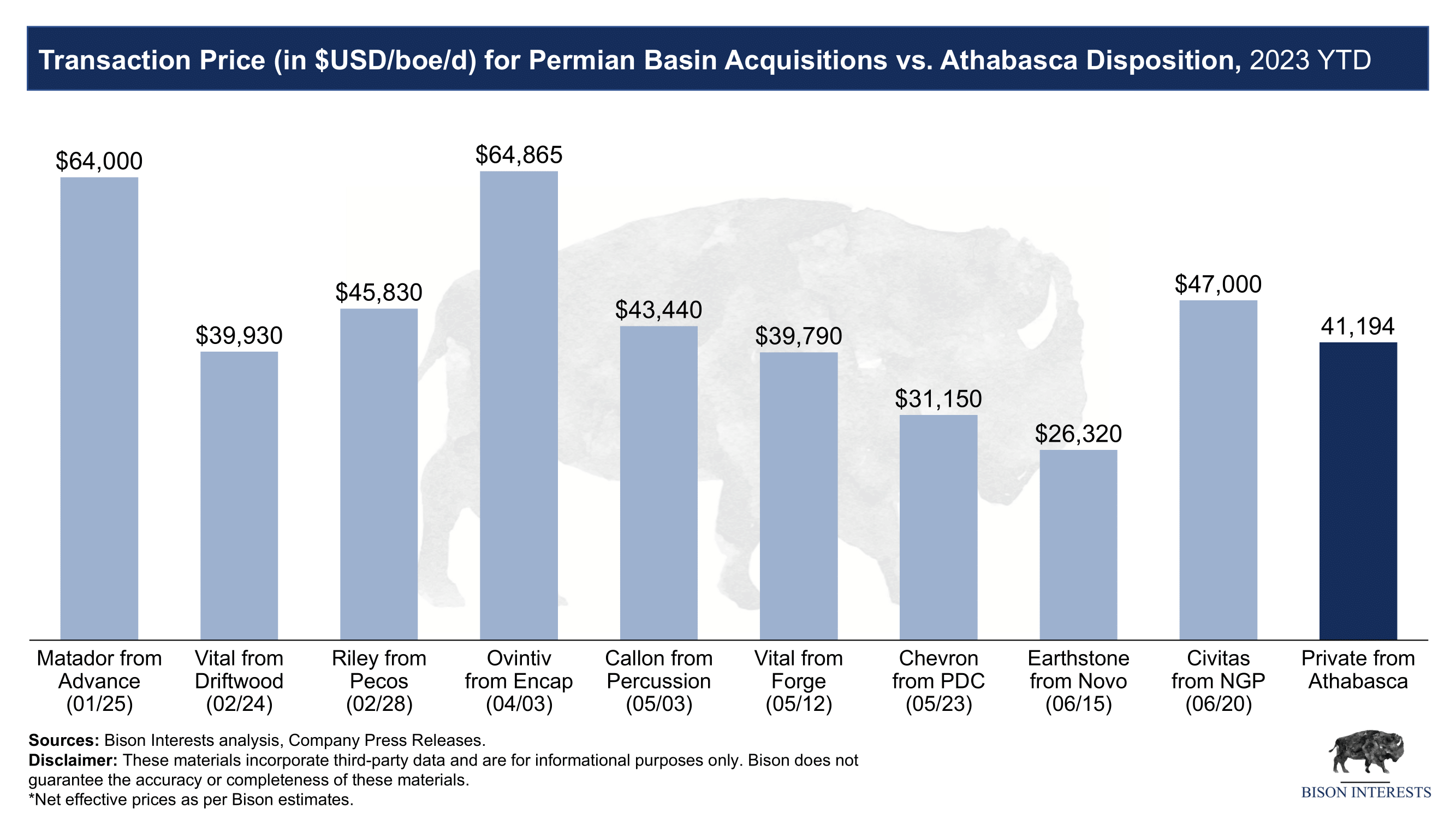

It is worth noting that these valuation metrics are on the higher end of recent Montney transactions, particularly when considering the higher gas weighting of the production. Even when compared to some of the Permian deals so far in 2023, this deal stacks up nicely:

Montney and Duvernay assets have transacted at lower multiples than Permian assets due to lower liquids weighting and because of fewer potential bidders in the region. And yet, after for adjusting for currency effects, it appears that Athabasca disposed of its assets at a higher valuation than many recent similar sized and larger Permian deals.

Implications:

This deal may be indicative of a rebound in Canadian M&A activity after a slowdown in Q2, and a steep decline since peaking in Q1 2021:

Importantly, it implies significant upside to many Canadian E&Ps trading at a substantial discount to the valuation implied by this deal. A ramping up of M&A activity could be a tailwind for small cap publicly traded oil & gas equities, which continue to trade at a discount to their liquidation values. These companies may have the opportunity to unlock significant value through dispositions like this one.

Another aspect worth noting is the “narrative violation:” the story told by private equity funds is that private assets are acquired by PE backed companies for low prices, improved, and then sold to publicly traded companies at higher valuations. However, in this case, a publicly traded company that had traded at a comparatively low valuation is selling high valuation assets to a private equity backed buyer. This narrative violation has positive implications for the potential performance of small, undervalued publicly traded E&P companies, and negative for the potential performance of private equity backed companies. With institutional fund flows towards private equity and out of public equity in the oil & gas space, this illiquidity premium may widen.

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises does not own shares of Athabasca Oil Corporation (TSX: ATH), but may buy or sell shares without any further notice.

Will PE never learn...Energy is not in their wheelhouse.

The importance of the "narrative inversion" cannot be overstated. Reading the news about the implosion of negative cash-flowing PE holdings, it seems like ultra-cheap energy could become an attempt to reactivate the original business model of PE. Where the exits will be may be less relevant to these buyers than the simple fact that they do not need a constant stream of new cash funding. Wonderful article as always.