Oil Price War, Opportunity in Canadian Oil Equities

Oil Price War, Opportunity in Canadian Oil Equities

(Important Disclaimer at Bottom)

Written by Josh Young, CIO at Bison Interests (Important Disclaimer at Bottom)

Devastation in the oil market is headline news, as oil prices fall by the most since 1991 in response to the failure of OPEC+ and an oil price war by Saudi Arabia. Oil producer equities were already down almost 50% year to date, and are likely to fall further in response to the news of the Saudi price war.

Source: Reuters

Over the weekend I was already getting calls, emails and texts asking about likely opportunities amidst the carnage. One in particular comes to mind: Canadian oil producers. Why not just buy an oil and gas equity ETF like (XOP) or (XLE) and forget about it? Here's why:

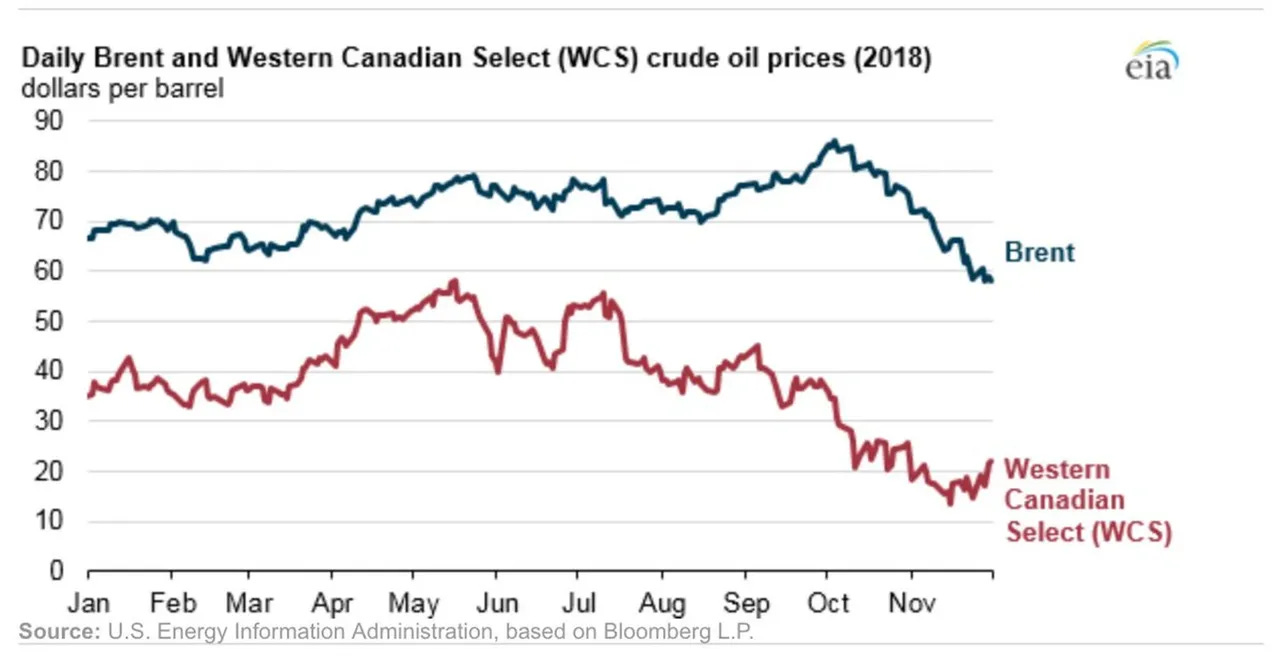

1) Canadian oil producers survived even lower realized oil prices already. In 2018, Western Canadian Select got as low as $14 per barrel due to local transportation issues. Surviving a period of exceptionally low prices positions them well to do so again:

2) The local transportation issues that sent local oil prices in Canada into the teens in 2018 have been generally resolved. Pipeline operator TC Energy (TRP) lowered its transport fee on the Keystone pipeline to export Canadian oil, indicative of this better transportation environment. Reduced midstream fees are a reason to prefer upstream producers to integrated (XLE) or midstream (AMLP) companies in this current dislocation.

3) Partially because of these historic transportation and low local price issues, and partially because capital markets closed to Canadian oil companies years before they closed to US E&Ps, Canadian producers have lower decline rates, higher free cash flow and generally more sustainable businesses. While few if any producers net any free cash flow at $30 WTI (USO), at higher prices Canadian producers generate substantially more free cash flow than comparable US producers per dollar of market cap or enterprise value.

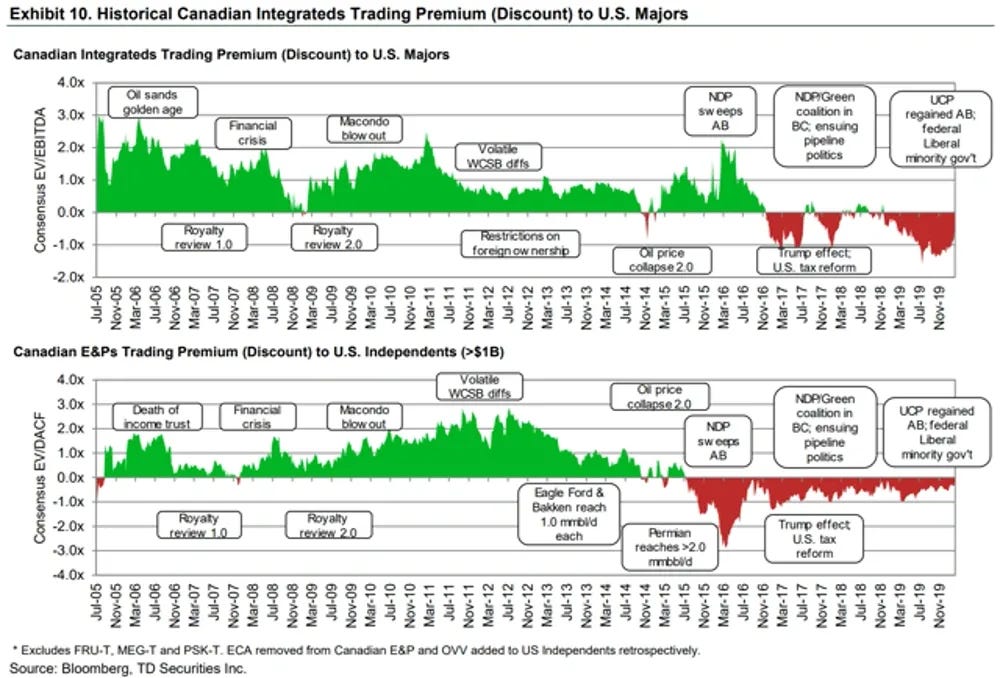

TD Bank displays an excellent chart of historical valuation premiums and discounts between US and Canadian producers, with a timeline commentary. While I think there's a better opportunity in medium sized E&Ps than in oil sands producers, it is still an effective graphical analysis that shows the long history of valuation premiums of Canadian producers before the recent history of discounts:

4) The Canadian producer ETF (XEG.TO) is not a great alternative as well, as it is primarily composed of integrated oil sands producers like Suncor (SU). While the integrated nature of the businesses of companies like Suncor offered a degree of protection in the oil price downturns of 2014 and 2016, their shares never traded down to nearly as low valuations as the independent producers. Even worse, refiners and midstream companies are seeing reduced demand and pricing power, partially discussed above and partially covered in a recent article on Exxon (XOM).

And oil sands operations like Suncor's, while they require comparatively smaller maintenance capital expenditures to sustain production, have higher operating costs than efficient independent conventional producers like Crescent Point (CPG), implying substantially lower upstream margins in a lower price environment.

5) The last time WTI was at $30 a barrel, some of these stocks were at much higher prices than they were on Friday:

Source: YCharts

For example, in 2016 when oil bottomed at $26, Crescent Point hit C$14. It closed on Friday at $2.91, almost 5x cheaper, despite billions of dollars of asset sales and debt pay-down. It may have been priced too richly at $14 in 2016 at $26 oil, but it is almost certainly priced too cheaply at $2.91 (and likely lower on Monday) at $30 WTI. And it is not alone, there are other such compelling independent Canadian producer opportunities.

6) The broader macro setup for energy stocks is compelling. Energy stocks were already at a low % of the overall market:

And energy stocks were already under-performing the market by the most since the attack on Pearl Harbor in 1941:

Source: FT

And energy had was already looking promising as the least favored sector versus technology, with potentially powerful mean reversion on both sides:

Source: stockcharts.com

These were compelling visual mean reversion arguments for oil and gas producer stocks, and are more compelling after the further % and price reductions after the Saudi announcement of the oil price war.

None of this addresses the specifics of the Saudi price war, what went wrong with OPEC+, demand risks from the Covid 19 pandemic and the ensuing global economic downturn, etc. However, in the context of a demand shock and now a supply shock, it is of value to find companies that have survived worse-than-current pricing. And I am finding such companies, along with compelling valuations and historical mean reversion opportunities, in Canada. And these opportunities may out-perform for many years into the future.

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises own shares in Crescent Point Energy and may buy or sell shares without any further notice.