OPEC+ Capitulates

OPEC+ Capitulates

(Important Disclaimer at the Bottom)

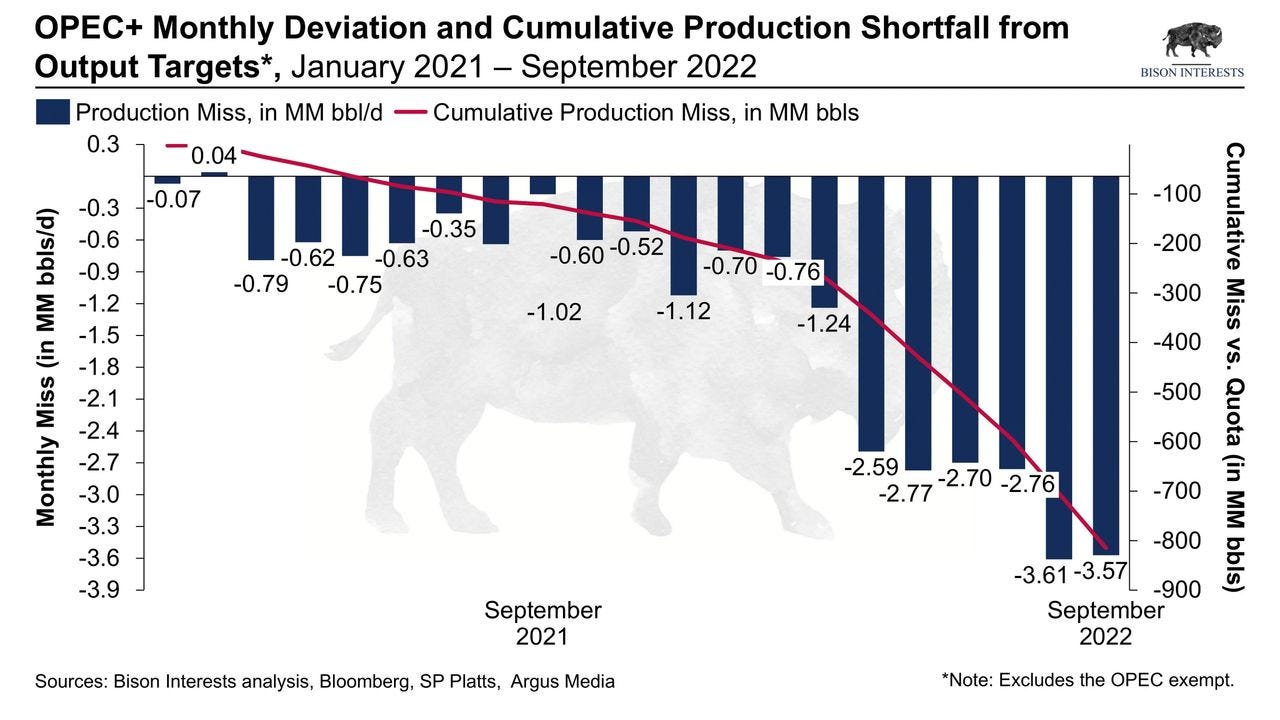

On October 5, 2022, OPEC+ agreed to a 2MM bbl/d cut to its oil production quotas, despite vocal opposition by the Biden Administration (and the media). For Bison white paper readers, this was no surprise. In our August 2022 white paper, OPEC+ is Protecting Oil Market Downside, we argued that OPEC+ had very little remaining capacity to increase oil output and would likely cut production quotas soon. Lack of investment is a key driver of diminished OPEC+ spare capacity, which we identified in The Myth of OPEC+ Spare Capacity in September 2021, and has translated to increasing production misses by OPEC+. Most recently in September 2022, OPEC+ missed its 42.2MM bb/d quota by 3.57MM bbl/d! Since the start of OPEC+’s post-COVID production increases in January 2021, OPEC+’s cumulative oil production shortfall versus quota has ballooned to over 800MM barrels:

Several Indicators that OPEC+ Production May Have Peaked

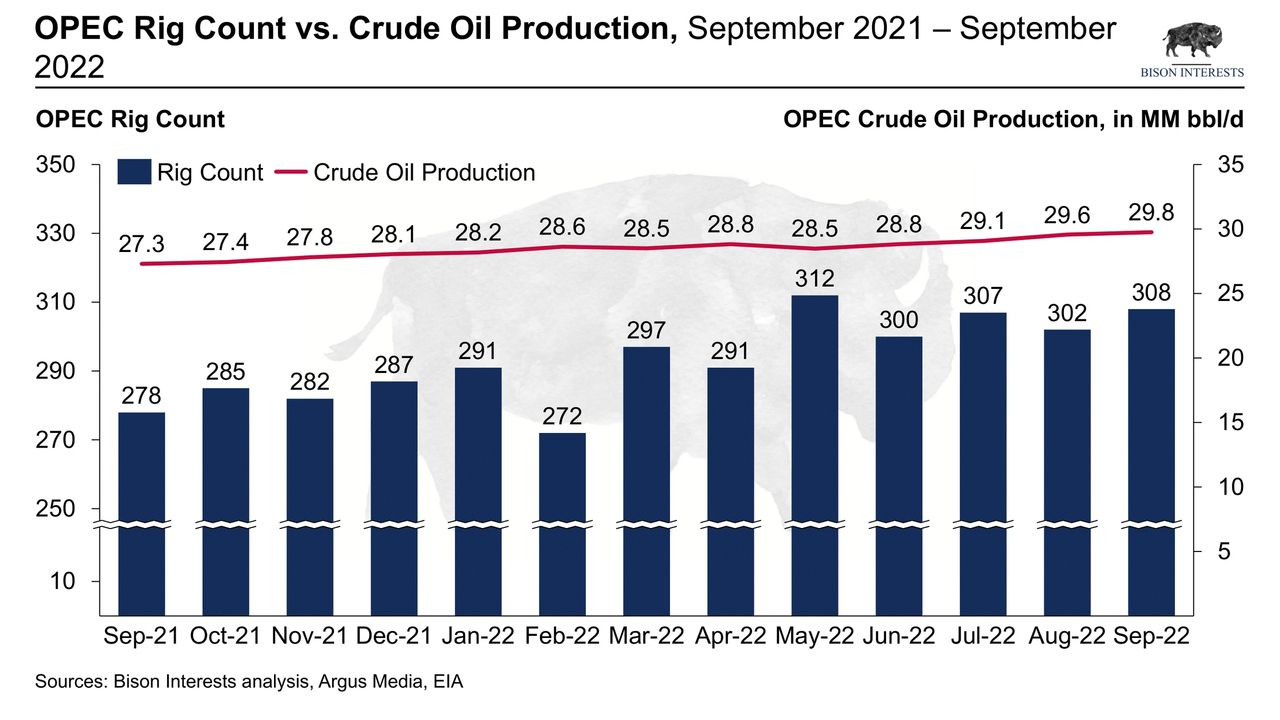

There are several indications that these production misses will persist, and that OPEC+ production levels may have peaked. The most prominent is that investment in oil field development by nearly all OPEC+ member countries has remained low after the oil price crash — activity has not rebounded with higher oil prices. For instance, the active rig count in OPEC countries has been about flat for most of this year:

Russia, OPEC+’s second largest producer, is already showing signs of declining production. While Russia’s output had fallen off following its invasion of Ukraine and associated Western sanctions, production rebounded in the following months as replacement customers were found for their oil such as China and India. Ironically, due to higher oil prices and smaller than anticipated declines in volumes, Russia’s oil profit reached $93B in the first 100 days of the conflict with Ukraine [1]. Russia’s temporary production rebound appears to be reversing, with Russian crude oil exports declining steadily since May:

Despite declining productive capacity, OPEC+ has attempted to maintain its image as oil producer of last resort. In August, OPEC+ announced a token quota increase of 0.1MM bbl/d, despite continued global supply shortages and large quota misses by OPEC+ members, which suggested that OPEC+ was struggling to supply the market [2]. Supportive of our view that OPEC+ could not meet any larger increase, the group announced it was slashing October production by 0.1MM bbl/d — swiftly rolling back the increase they approved only a month prior [3].

Production Cut

OPEC+’s limited ability to increase oil production to capture higher oil prices indicated to us that they were likely to opportunistically reduce production to protect falling oil prices – at a time when the conversation was still focused on OPEC+ growing production. With OPEC+ oilfields already running near maximum capacity, which could hinder long term oil recovery prospects, there was an added incentive to reduce production. With any hint of potential global economic slowdown, OPEC+ could cut in anticipation of muted demand growth. And with OPEC+ members repeatedly expressing concern that global production capacity remained too low, output cuts could be an effective tool to increase prices and stimulate new investment [4].

Only 2 months later, OPEC+ signalled its intention to slash production in response to falling oil prices and uncertainty surrounding the global economic outlook. Following the initial OPEC+ announcement, most analysts and market participants began to anticipate a cut of 0.5 - 1MM bbl/d — which was reflected in the price of oil in the days ahead of the meeting. OPEC+ surprised many when it announced baseline cuts of 2MM bbl/d.

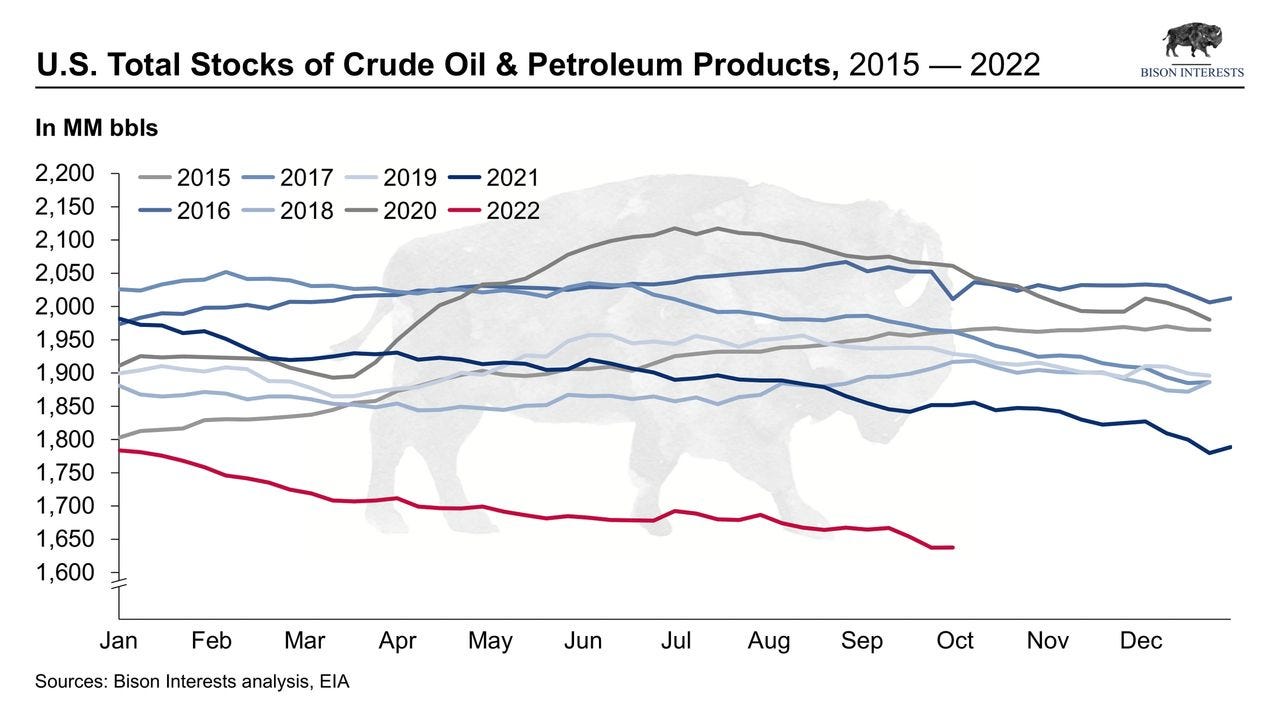

A 2MM bbl/d production cut has implications for long term oil prices, given that global markets were already very tight—and likely undersupplied—as indicated by dwindling oil inventories in the US and elsewhere:

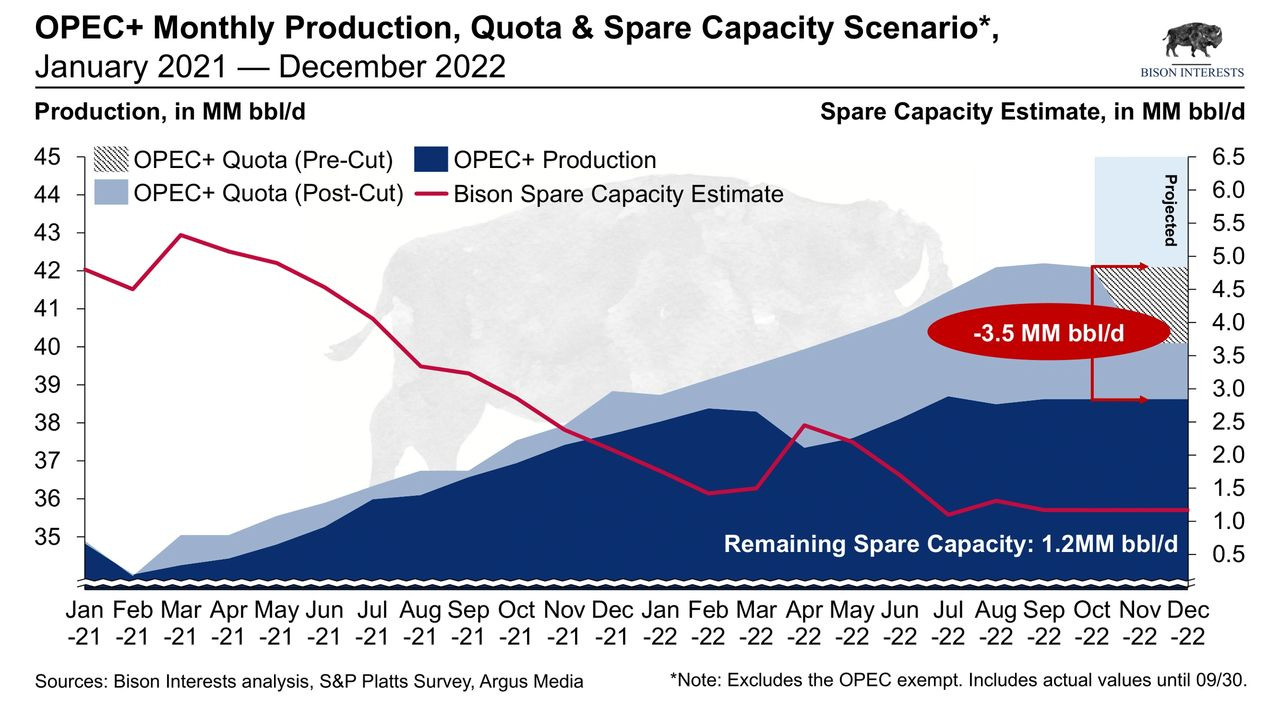

Even if OPEC+ production quotas had remained flat, production would likely have continued to lag, as can be seen below. The world oil market may see a long-term production shortfall of 3.5MM bbl/d vs. pre-cut production quotas:

OPEC+ has little spare capacity remaining, held by a few member countries such as the UAE and Kuwait. The challenges of producing at or near full capacity imply continued struggles to grow production sufficiently to meet even the now-lowered quotas. This could mean further OPEC+ quota cuts in the future, even if the oil market remains tight.

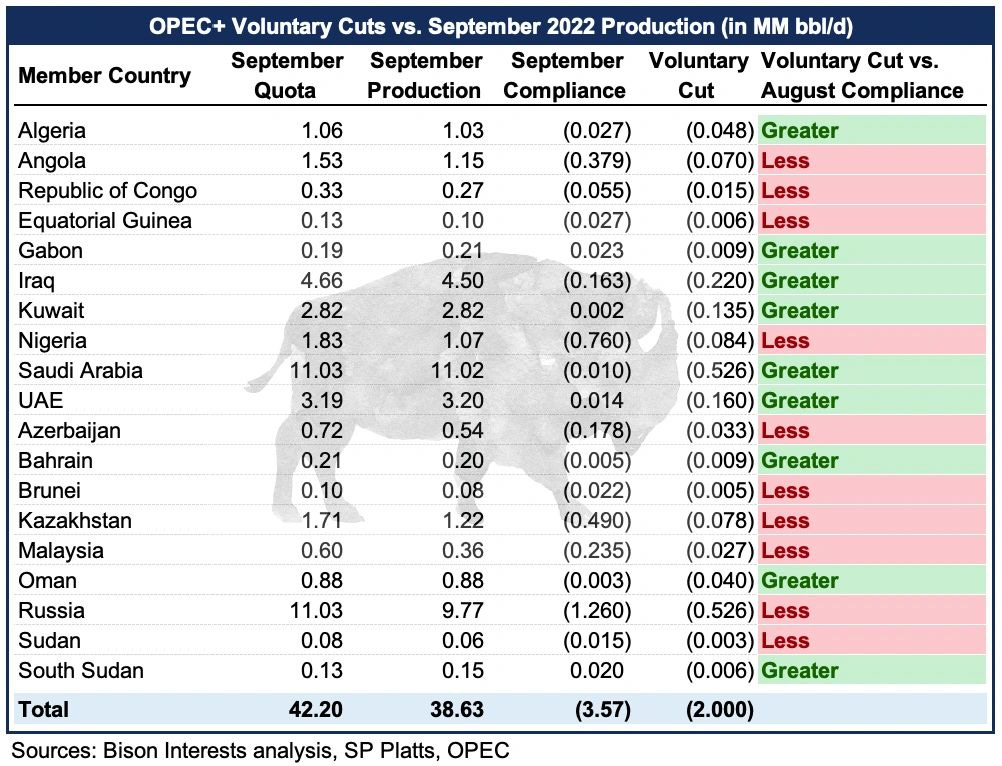

OPEC+ has been struggling to meet production quotas for months now, and as a result, the actual supply of oil taken off the market will likely be much lower than 2MM bbl/d. And not all member countries are equal: many smaller producers have missed quotas markedly for several successive months now, suggesting that they are definitively out of spare production capacity. Nonetheless, OPEC+ has ascribed these countries some voluntary production cuts, despite already lower than quota production:

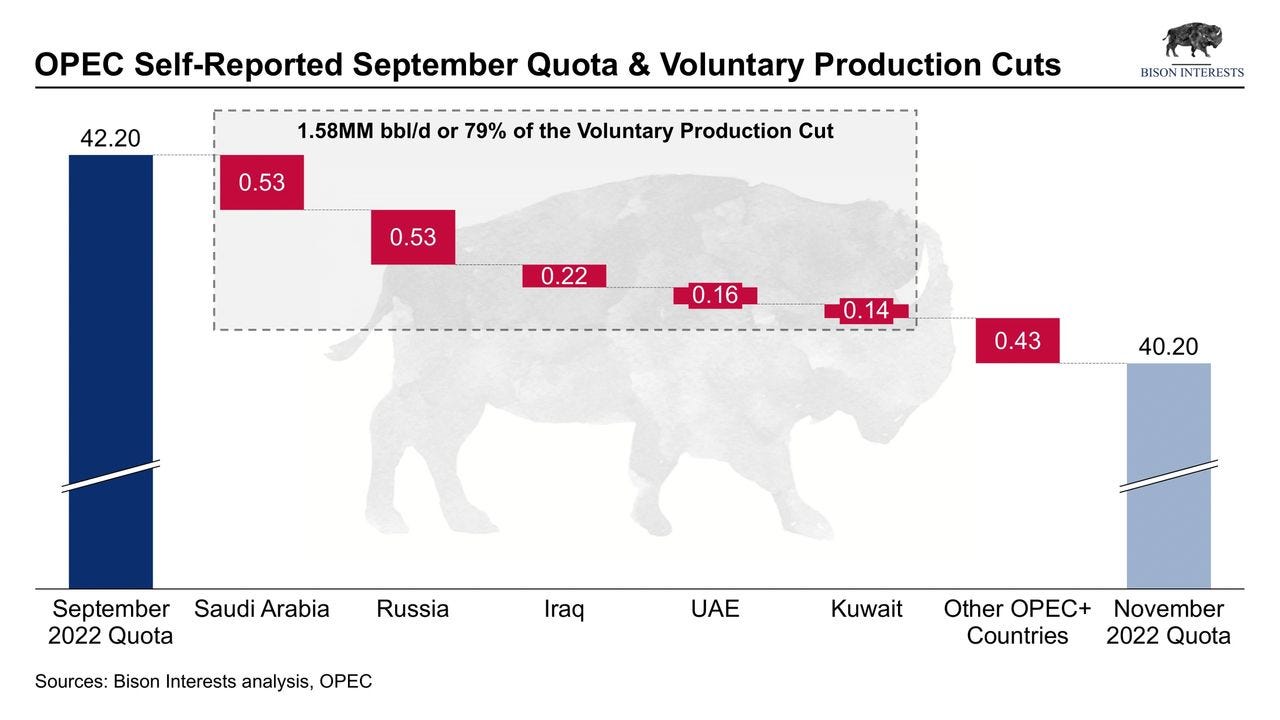

More than half of OPEC+ members had already missed September production quotas by more than the amount of production they are now being asked to cut voluntarily, indicating that there may be limited incremental production taken off the market by those countries. Additionally, OPEC+'s voluntary cut schedule seems to confirm our initial suspicion that the bulk of remaining OPEC+ spare capacity was concentrated in a handful of countries. As can be seen below, 79% of OPEC+’s 2MM bbl/d cut will be borne by 5 countries:

OPEC+ Production Outlook & Implications

OPEC+ production is likely on a declining trajectory, and these cuts may be the start of an attempt to reconcile nearly 2 years of missed production quotas and muted drilling activity. This could ultimately translate into lowered market expectations for OPEC+ production, and broader awareness of medium-term oil market undersupply.

We identified peak in OPEC+ spare capacity and production last year, and in our view, this is a big step towards recognition of that by OPEC+ and ultimately the broader market. Even if OPEC+ succeeds in its goal of increasing oil prices, it is unlikely that they can subsequently sustainably increase production to capture these higher prices in the short to medium term due to lack of spare capacity and insufficient investment.

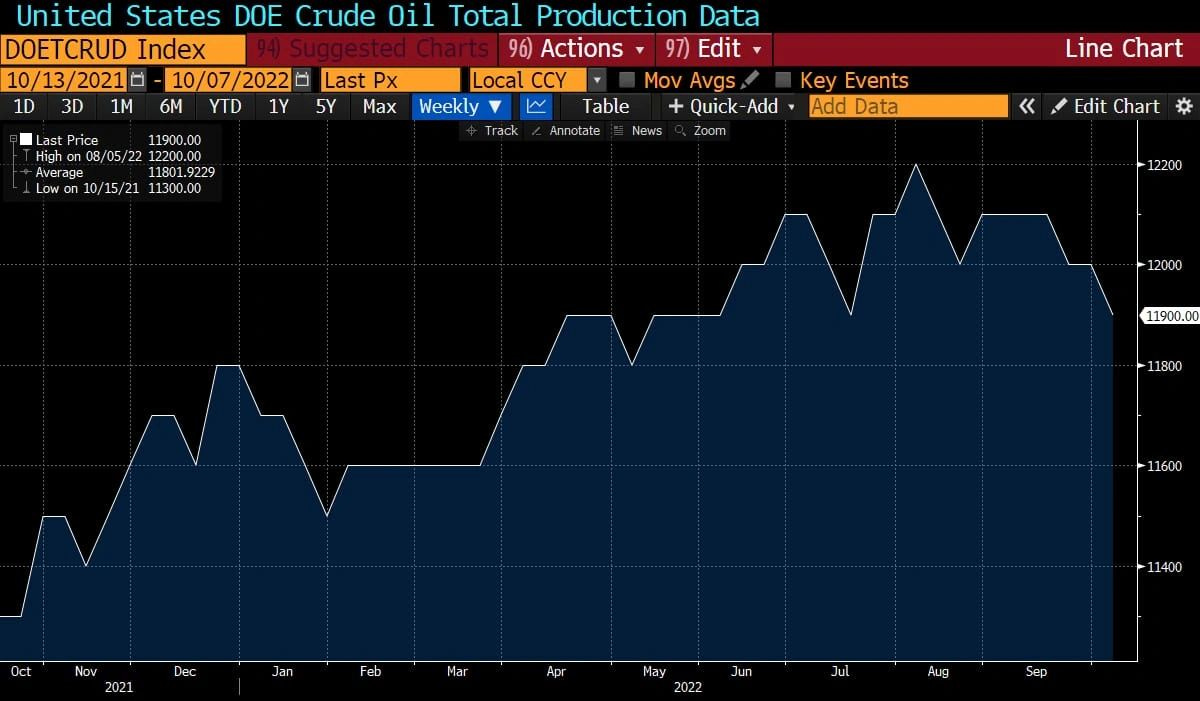

As world oil demand continues to steadily edge higher despite economic challenges, while OPEC+ supply continues to surprise to the downside, the oil market may be entering a new regime where $100+ oil becomes the new norm. This is particularly true as non-OPEC production expectations are revised downwards, as seen in recent US oil production data:

Oil prices are unlikely to “normalize” until supply increases substantially to meet growing world demand. It seems increasingly unlikely that the oil market will be adequately supplied anytime soon, considering historical and current lack of investment, restrictive policy and the lead times associated with new oil production such as offshore developments.

Many are concerned that slowing economic growth, accelerating inflation, and rising interest rates could potentially induce a recession and dampen oil demand. While a recession may be a short-term headwind for oil prices, this could actually improve longer term oil market fundamentals. Higher interest rates and equity cost of capital would likely further restrict investment in oil and gas, and investment in the industry is already far below levels required to meet likely future demand.

With OPEC+ capitulation, disappointing non-OPEC oil production, and tight markets despite likely temporary Chinese lockdowns and weak economic activity, we think oil prices should be elevated in the medium to long term. In this environment, oil & gas producers—which are already experiencing record free cash flow generation at $80 WTI—will benefit disproportionately.

Sources

[2] Source: Oilprice.com

[3] Source: The New York Times

[4] Source: OPEC

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.