OPEC+ is Protecting Oil Market Downside

OPEC+ is Protecting Oil Market Downside

(Important Disclaimer at the Bottom)

Shortages of oil, natural gas and coal are reverberating across world economies—the bill from prior underinvestment is coming due, and Russian supply disruptions aren’t helping. Europe and parts of Asia are already facing an unprecedented energy crisis, with the price of natural gas in Europe (TTF) having increased 10x in 18 months:

With energy shortages looming, European governments are warning of potential mandated blackouts—some are even recommending burning firewood for heat! As the crisis intensifies, oil is increasingly being used to power factories and generate electricity, and oil will likely be an important source of heating fuel this coming winter.

In the aftermath of the spike in oil and diesel prices earlier this year, and with the energy crisis worsening, OPEC+ is increasingly drawing attention as it repeatedly misses production quotas. Western government leaders have foregone prior commitments and visited Saudi Arabia to ask for more oil.

OPEC+ has previously exercised oil market control and withheld production to support oil prices, including in April 2020. However, since January 2021, OPEC+ has been increasing quotas and production by millions of barrels per day. With oil prices rising since then and spiking in March 2022 due to Russia’s invasion of Ukraine, OPEC+ has been pushing to supply as much oil as possible to the market to capture higher prices. So why have they been missing production quotas by millions of barrels per day? They are nearly out of spare oil production capacity.

A “healthy” oil field should not be run at maximum capacity, as over-production reduces the quantity of total recoverable oil — OPEC+ knows this. As such, OPEC+ as a group and individual members of the cartel may be quick to reduce production moving forward. Should demand fall and the oil market move into an over-supplied situation in the event of an economic slowdown or increased lockdowns in China, OPEC+ oil supply may be reduced swiftly in response. With OPEC+ controlling over 40% of global oil supply, a cut would support oil prices in the event of a demand drawdown. An “overshoot” of production cuts could easily send oil prices soaring, which would be a positive outcome for OPEC+ members.

Bison’s OPEC+ Spare Capacity Work: From Contrarian to Mainstream

We shared our initial “The Myth of OPEC+ Spare Capacity” thesis in September 2021. In the aftermath of a price war in early 2020 and years of low oil prices, almost all oil analysts and market participants accepted OPEC+ self-reported numbers. This was a factor in consensus bearish views on oil prices—insisting that OPEC+ could simply “turn on the taps” and flood the market with supply. In contrast to this widely accepted narrative, Bison argued that OPEC+ spare capacity was overstated. We observed that OPEC+ had already begun to miss its production quotas, member countries had been underinvesting in productive capacity, and maturing oil fields with few new discoveries and that limited development was resulting in declining production capacity.

Our October 2021 follow up analysis “OPEC+ Space Capacity is Insufficient Amid the Global Energy Crisis” came at time when energy supply issues were leading to higher energy prices, particularly with lower than consensus US oil production and reduced natural gas supplies to Europe from Russia. Persistent oil bears cited abundant OPEC+ spare capacity as the “escape valve” to the escalating energy supply crisis, while Bison maintained its view that OPEC+ spare capacity was overstated. We estimated OPEC+ total spare capacity to be between 2.75MM barrels of oil per day (bbl/d) – 3.75MM bbl/d as of October 2021. Despite increased drilling and development by OPEC+ members, production undershot large quota increases and drilling over the subsequent year, confirming our analysis.

OPEC+ spare capacity has been an issue that has been widely debated—and poorly understood—for years. Naturally, when Bison put out a controversial research piece citing that OPEC+ spare capacity had nearly run out, we received a lot of pushback. Many cited our lack of expertise in reserve engineering, lack of presence in OPEC+ countries, research papers by industry consultants claiming plentiful spare capacity, etc. Even around the time of our white paper publication, we had begun to see validation of our work: OPEC+ missed several of their budgeted production increases, the IEA had been consistently revising their estimates of spare capacity, and an Ex Saudi Aramco EVP had already sounded the alarm.

Today, it appears that our initial thesis is on its way to becoming consensus: OPEC+ quota misses have worsened every month, their production is significantly behind quota, and both are making mainstream media headlines. Given their track record of 18+ months of under-production, it is likely that OPEC+ is already producing at or near max capacity, which may be declining as their oil fields mature despite new investment:

On Recession Fears & The “OPEC+ Put”

Many are concerned that central bank monetary tightening and worsening economic conditions could result in a recession. In this scenario, demand for oil, gas and its distillates could fall, pressuring prices downwards. Due to these economic concerns, bearish views on oil and gas and associated equities are increasingly popular and speculative interest in oil futures is quite low.

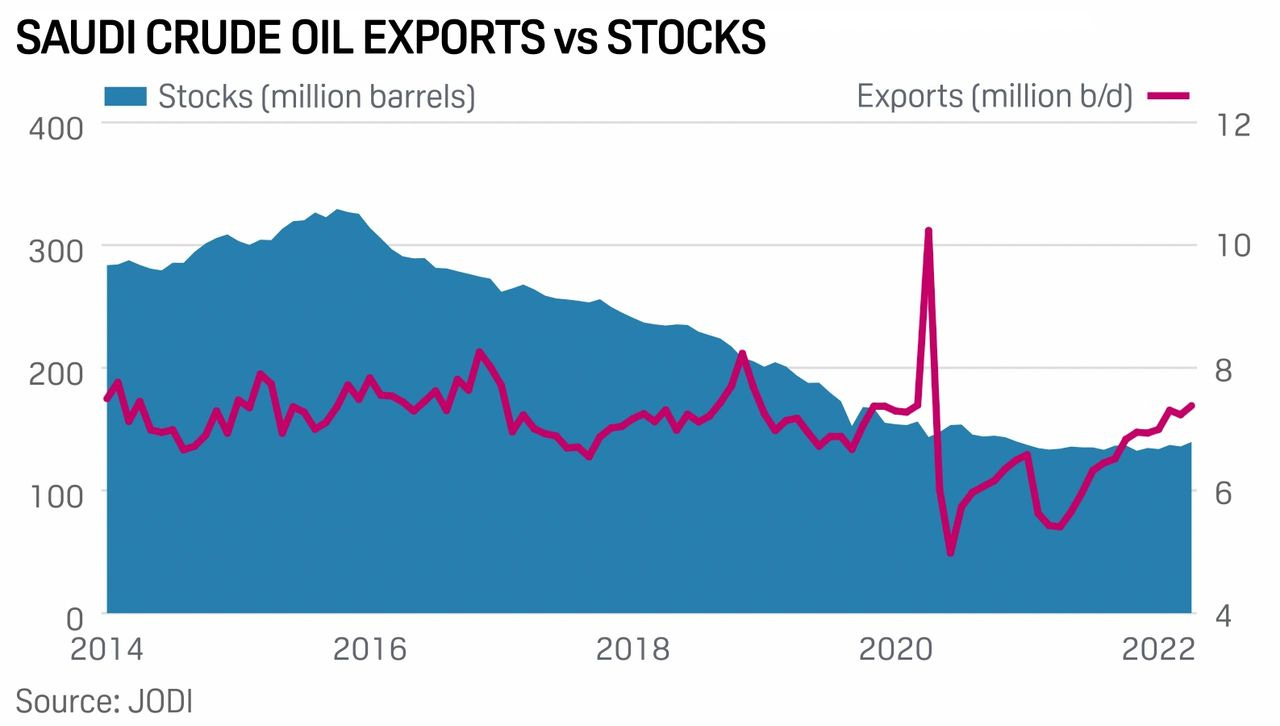

We have a variant view. OPEC+ is aligned with higher oil prices, and has a vested interest in producing and selling as much oil as possible to capture them. For instance, Saudi Arabia has been heavily depleting its onshore oil inventories in favour of exports, which reached $30B in March [1]:

While OPEC+ has little spare capacity left to raise production, it could easily and meaningfully reduce production in the event of an actual recession to protect prices. And with oil fields currently running at or above maximum capacity, which may hurt long term production capacity and is unsustainable for extended periods of time, member countries have an added incentive to step in and lower production in the event of a recession.

Bearish oil analysts and market participants seem to be overlooking the speed and extent to which OPEC+ could slash production in response to perceived demand destruction. OPEC+ members are already running at very near or full capacity: production has fallen short of its self-imposed targets, and compliance to these quotas has been rising, not by choice, as can be seen below:

And should there be no recession, there is no reason to think that OPEC+ won’t continue to miss production quotas moving forward. With no OPEC+ spare capacity “escape valve,” we should expect prices oil prices to adjust much higher, while their ability and inclination to curtail production should buffer downside price movements.

OPEC+ Production is Likely to Undershoot Moving Forward

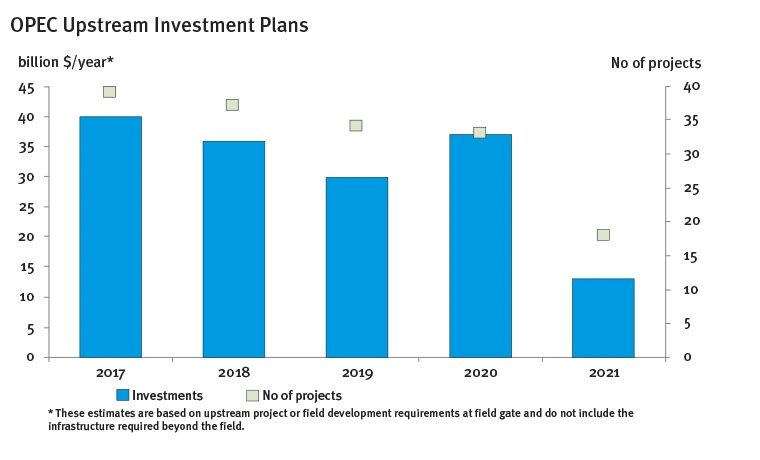

Although there are several indications that OPEC+ production has peaked and may decline moving forward, the most compelling is the sheer lack of investment. Like it’s OECD counterparts, OPEC+ countries have been underinvesting in oil production capacity for years, as can be seen below:

Lack of investment in productive capacity was at the core of our original thesis, and in our view, will be the biggest driver of an undersupplied global market. And based on investment trends and the trajectory of OPEC+ production this year, there is a material risk of flattening or declining OPEC+ oil production moving forward. If OPEC+ production was to remain flat, almost 3.3MM bbl/d of expected OPEC+ oil production could be left off the market:

Recent Developments are Encouraging

oRecently, there have been several indications that our initial thesis was true, aside from clear production missed from OPEC+. For instance, President Biden’s visit t Saudi Arabia, in which he intended to request that the Kingdom increase its oil production, left much to be desired. Prince Mohammed denied Biden’s request, stating that it is the world’s collective responsibility to invest in fossil-fuel production.

Shockingly, the prince himself revised down Aramco’s 13MM bbl/d stated production capacity, making it clear that it will soon not have any more capacity to increase production [2]. This was validated again in Saudi Aramco’s Q2 earnings call, in which management revealed plans to increase production capacity to 12.3MM bbl/d, but only by 2025—implying that Saudi Arabia’s production capacity was previously overstated [3].

OPEC Secretary General Haitham Al-Ghais recently warned that the world is “running on thin ice […] because spare capacity is becoming scarce”. He explained that he believes the recent sell off in oil—which is largely related to China demand fears—is overblown, particularly when considering how tight physical markets are [4]. This is the second time an executive with boots on the ground has sounded the alarm, and it likely won’t be the last.

Earlier this month, OPEC+ agreed on a token increase of 0.1MM bbl/d for September despite calls from several global leaders for more production, stating that it had to ration it’s “severely limited” reserves of output. And in our view, this increase was largely symbolic in the context of current global demand, and repeated production misses vs. quota increases in the past [5].

Bison Thought Leadership

Bison has been focused on this OPEC+ spare capacity issue for some time now because it may be an important driver of structurally higher oil prices moving forward. Since our published thesis in September 2021, this has been covered in mainstream media outlets such as Bloomberg, Reuters, CNBC and elsewhere. These came out months after our prior pieces, often mirrored our logic and analysis that was not present in other publicly available research pieces, and serve as evidence of Bison thought leadership in the oil and gas space even if we weren’t directly cited.

Looking forward, OPEC+ production will be watched closely as these issues are increasingly in the spotlight. As the group continues to struggle to increase production, or even keep it steady, global markets may begin to price in this new reality—sending oil prices higher. And while this likely implies more pain for world economies already facing energy shortages, it should bolster higher energy prices and associated equities.

Sources

[1] Bloomberg

[2] Source: The Washington Post

[3] Source: SP Platts

[4] Source: BNN Bloomberg

[5] Source: BNN Bloomberg

Important Disclaimer:Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.