OPEC+ Meets, Saudi Voluntarily Cuts Production

OPEC+ Meets, Saudi Voluntarily Cuts Production

This past weekend, OPEC+ struck a deal to extend production cuts into 2024 to support the oil market. And aside from official production cuts, it is possible that individual member countries will announce further voluntary cuts, as did Saudi Arabia.

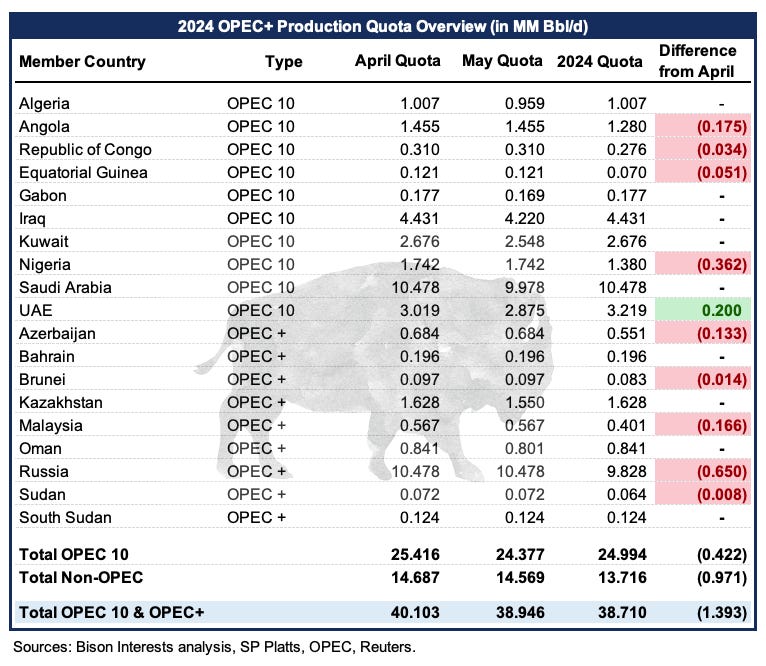

We estimate that effective January 2024, OPEC+ will be cutting production quotas by 1.4MM bbl/d using April 2023 as a baseline, or an additional 0.24MM bbl/d from expected May quotas following the implementation of surprise voluntary production cuts announced in April:

As can be seen above, the entirety of the production cut will be borne by 9 member countries, notably Russia. Many of the smaller OPEC+ producers had already been struggling to meet current production quotas for some time now, implying that they were out of spare capacity. New targets may be an attempt to reconcile nearly two years of lackluster production by reducing quotas in line with current output levels.

In contrast to OPEC+’s smaller members, many of the larger producers will see their production quotas unchanged, effectively undoing May voluntary cuts. These countries have been producing closer to production targets and arguably have some production capacity remaining, although it may have been lower than advertised. The United Arab Emirates—which may have the most spare production capacity out of all member countries—will see its production quota increase by 0.2MM bbl/d in 2024.

Additionally, Saudi Arabia announced voluntary production cuts of 1MM bbl/d effective July 2023, and specified that it could extend these if deemed necessary. However, Saudi Arabia had already slashed 0.5MM bbl/d of production as part of OPEC+ surprise production cuts of 1.6MM that came into effect in May, and it was unclear whether this would be included in the July reduction. In either case, this is incrementally positive for the oil market as this will reduce inventories along with the chances of OPEC+ discord, which could have led to a price war like that seen in March 2020.

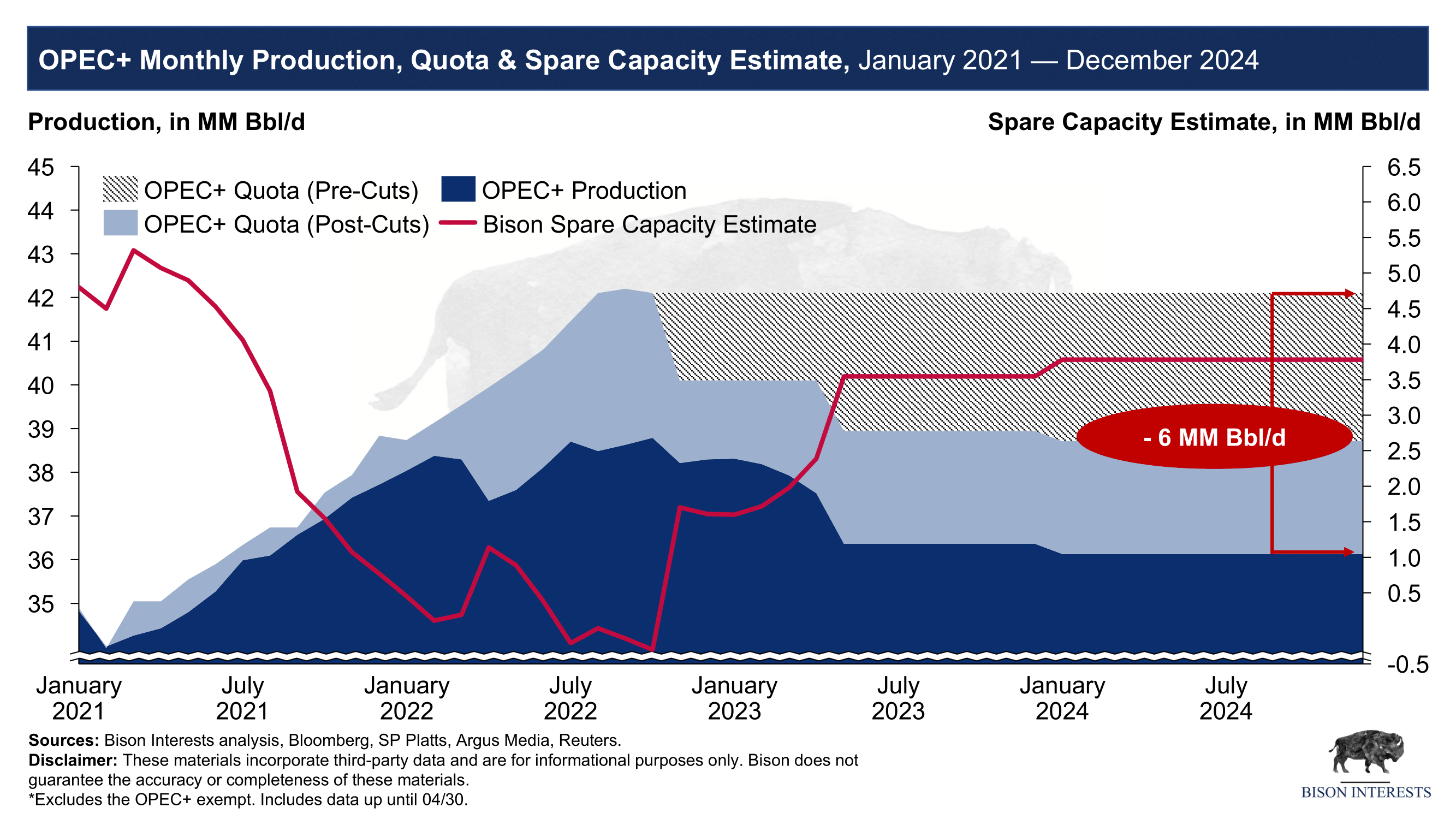

With Saudi Arabia’s voluntary production cut in effect as of July and further production cuts scheduled for January of next year, OPEC+ will have slashed production quotas 4 times in a short period—having agreed to cuts of 2MM bbl/d last year and 1.6MM bbl/d just last month. To the extent that these cuts are implemented by member countries, world oil markets may be meaningfully undersupplied from pre-cut expectations:

If there isn't a severe recession, global oil demand will likely continue to grow to new all-time highs. And even if there were a recession, it is likely that OPEC+ members would swiftly cut production to support oil prices, as they have historically.

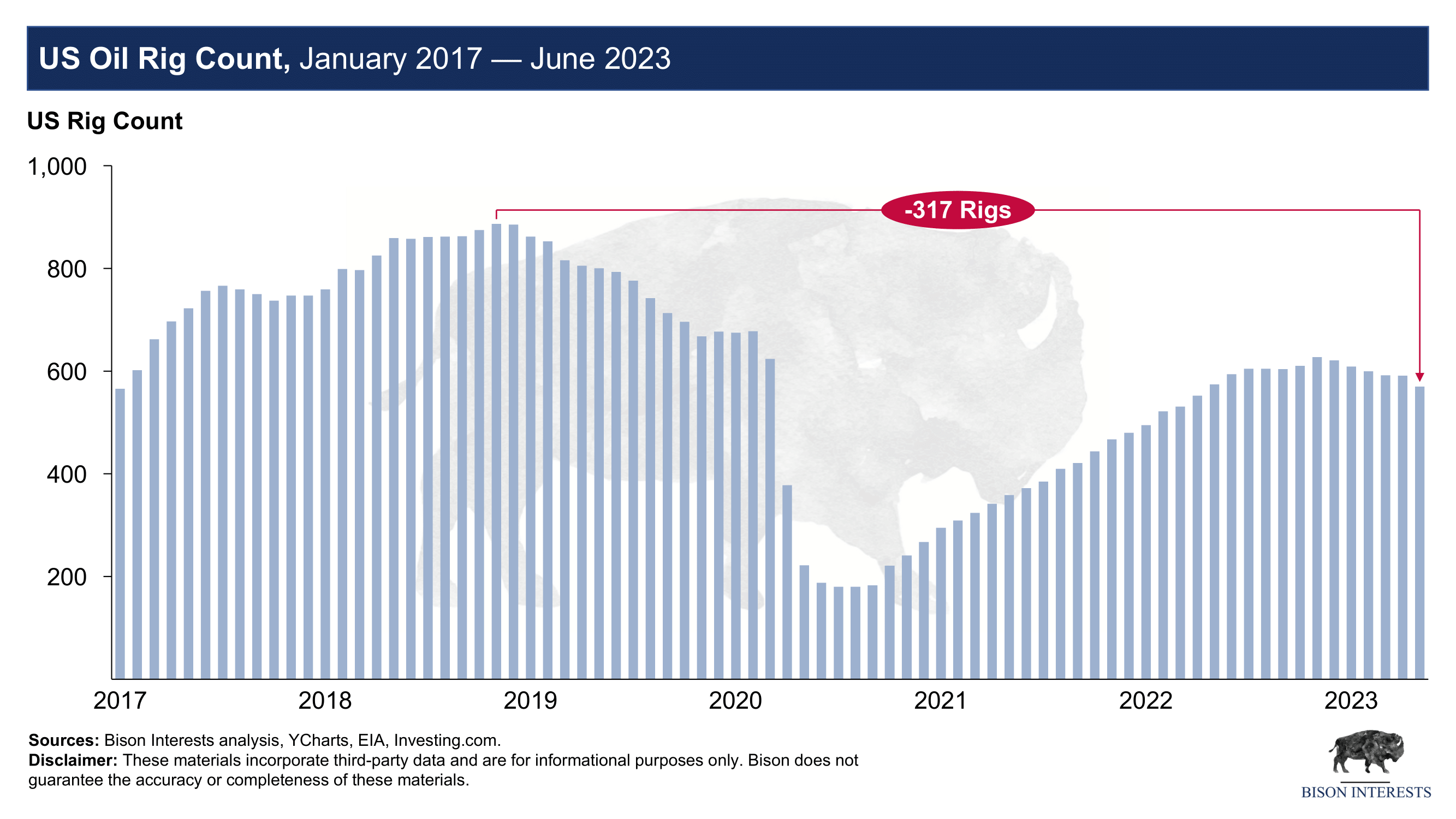

Against a backdrop of rising demand it is unlikely that sufficient new net supply of oil is going to be brought to world markets, due to limited investment in exploration, falling rig counts, rising geopolitical tensions, and other factors. In OPEC+ countries, repeated production cuts are indicative of declining spare production capacity, while in the U.S, shale producers have limited ability to bring new supply even if oil prices rise dramatically—a likely motivation for Saudi Arabia’s voluntary production cut:

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice.