Permian Basin Consolidation Continues with Permian Resources’ Acquisition of Earthstone Energy

One week after Earthstone Energy (NYSE: ESTE) closed on its acquisition of Novo, Permian Resources (NYSE: PR) announced that it is acquiring Earthstone. The pro forma entity will be one of the largest Permian-focused oil & gas producers, with production of ~300,000 boe/d. This is the latest in a series of Permian transactions, is the first buyout of a Permian publicly traded company in some time, and continues the trend of rising Permian transaction multiples. The implications of this deal for other publicly traded Permian oil & gas producers should not be overlooked.

Transaction Analysis

Permian Resources will issue ~211MM shares to Earthstone shareholders in this transaction, or 1.446 PR shares per ESTE share. This effectively values ESTE at $18.64, representing a ~15% premium to their pre-deal closing price. This is the first buyout of a publicly traded Permian producer in some time, and this particular transaction has important implications for Vital Energy (NYSE: VTLE). More on this below.

At the time of the deal announcement, the Permian Resources stock issued to Earthstone shareholders values Earthstone equity at approximately $2.7 billion. Adding the ~$1.8 billion of net debt assumed by Permian Resources puts the transaction value at approximately $4.5 billion:

Permian Resources Acquisition & Implications

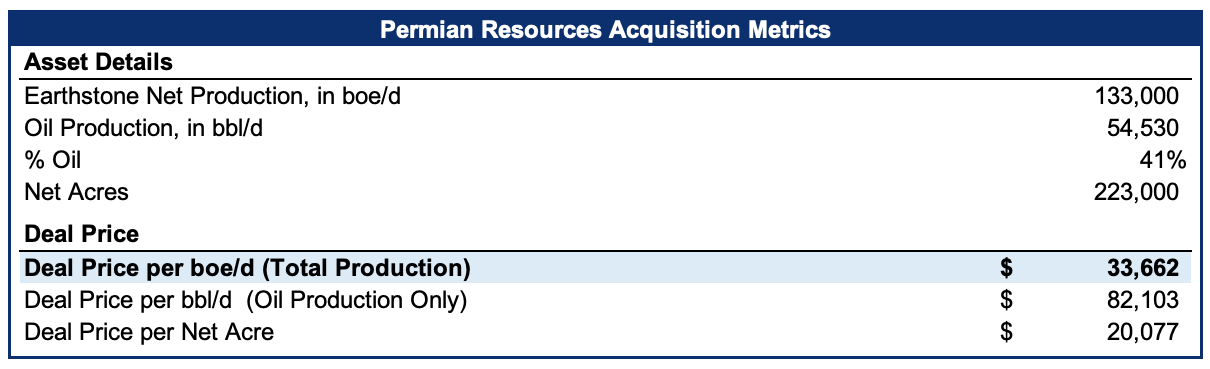

Permian Resources’ disclosure shows it buying ~133,000 boe/d (41% oil) effective in Q4 2023 (baking in some production growth without accounting for the capex). This production comes with 223,000 net Permian acres. This implies a deal price of $33,662/boe/d for Earthstone, $82,103/bbl/d or ~$20,077 per net acre:

While this deal price is in line with other recent Permian transactions and lower than some of the highest-priced deals, it is the first Permian public equity buyout in a while, is funded entirely with PR shares, and is at a premium. None of these have been common in small-cap E&P buyouts. Additionally, Earthstone’s market valuation did not fully reflect its inventory of high-return drilling locations in the Permian, with an EV/EBITDA multiple of ~3.0x and an EV/PDP of 0.9x.

Implications for Vital Energy

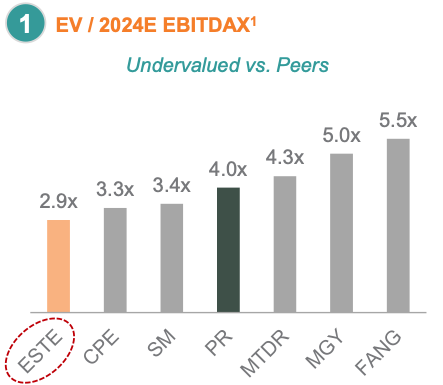

Permian Resources says it is buying Earthstone for ~3.0x EV/EBITDA in its deal announcement, while consensus estimates suggest that ESTE was trading closer to ~3.5x. In either case, pre-deal Earthstone was inexpensive compared to most of its peers.

However, Vital Energy, which has a higher oil weighting and a similar amount of Permian acreage nearby to PR, still trades near 2x EV/EBITDA! We estimate that this transaction’s valuation implies nearly 90% upside to Vital Energy’s share price, as can be seen below:

Considering Earthstone’s lower valuation compared to its peers besides Vital, the above scenario may represent the low end of what Vital could transact at in a similar deal. By the same token, it is also worth considering what more expensive transactions like Civitas’ acquisition of private assets in the Permian could imply for Vital (at the time, a 264% premium to VTLE’s price) for a better understanding of the possible range of outcomes.

It is remarkable that moderately priced transactions display substantial implied upside to Vital’s share price. We believe this is an indication that VTLE is too heavily discounted in the public market. And with the rapid pace of consolidation in the Permian and rising deal valuations, the opportunity to buy these assets in public markets on a discounted basis may not be available for much longer.

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not investment recommendations and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises own shares in Vital Energy (NYSE: VTLE) and may buy or sell shares without any further notice.

Thanks for the reply and the great analysis you provide on this sector - agree wholeheartedly on VTLE..

Great article Josh. Good deal for PR. While XOM & CVX with other majors are chasing ESG crap the other more shareholder (NOT stakeholder) minded companies are closing lucrative deals.