Recession Fears Mean Opportunity In The Oil Market

Source: Brian Feroldi

Oil market sentiment is nearing lows not seen since Covid 19 – a time when government lockdowns collapsed oil demand and fears of full storage sent oil prices briefly negative. Since peaking in June 2022 following Russia’s invasion of Ukraine oil prices are down 40% amid recession fears, despite rising global demand, rapidly depleting oil inventories and a tight physical market:

Extended periods of weak price action tend to shift investor sentiment, irrespective of underlying fundamentals. Essentially, price drives narrative. However, these disconnects between fundamentals and sentiment offer opportunities to outperform the market, as discussed by Warren Buffett, Howard Marks and other all-time-great investors. This is particularly true when fundamentals are improving while valuations remain low due to widespread negative sentiment.

In times like these, where negativity and fear are pervasive, we find it helpful revisit fundamentals and alternative data. Below is a series of considerations on the oil market and recession fears. We have no ability to predict the future, but we are assessing these and other factors in our analysis of the oil market and our evaluations of the fundamental values of related equities.

Negative Sentiment is Consensus

Negative oil sentiment has gotten so extreme that the forward oil price implied by futures markets is currently 30% lower than consensus estimates. According to Goldman Sachs, the investment bank which we credit with the chart below, this consensus/futures gap falls into the 98th percentile throughout history:

Source: Goldman Sachs

It is worth noting that statistical analysis by Goldman indicates that the spot price usually ends up at or above the consensus forward price for oil, consistent with the risk premium in futures markets. While we are not relying on this, it is worth considering what has happened historically when the futures curve has been this far below consensus expectations—oil prices rose substantially. History doesn’t repeat, but it does rhyme.

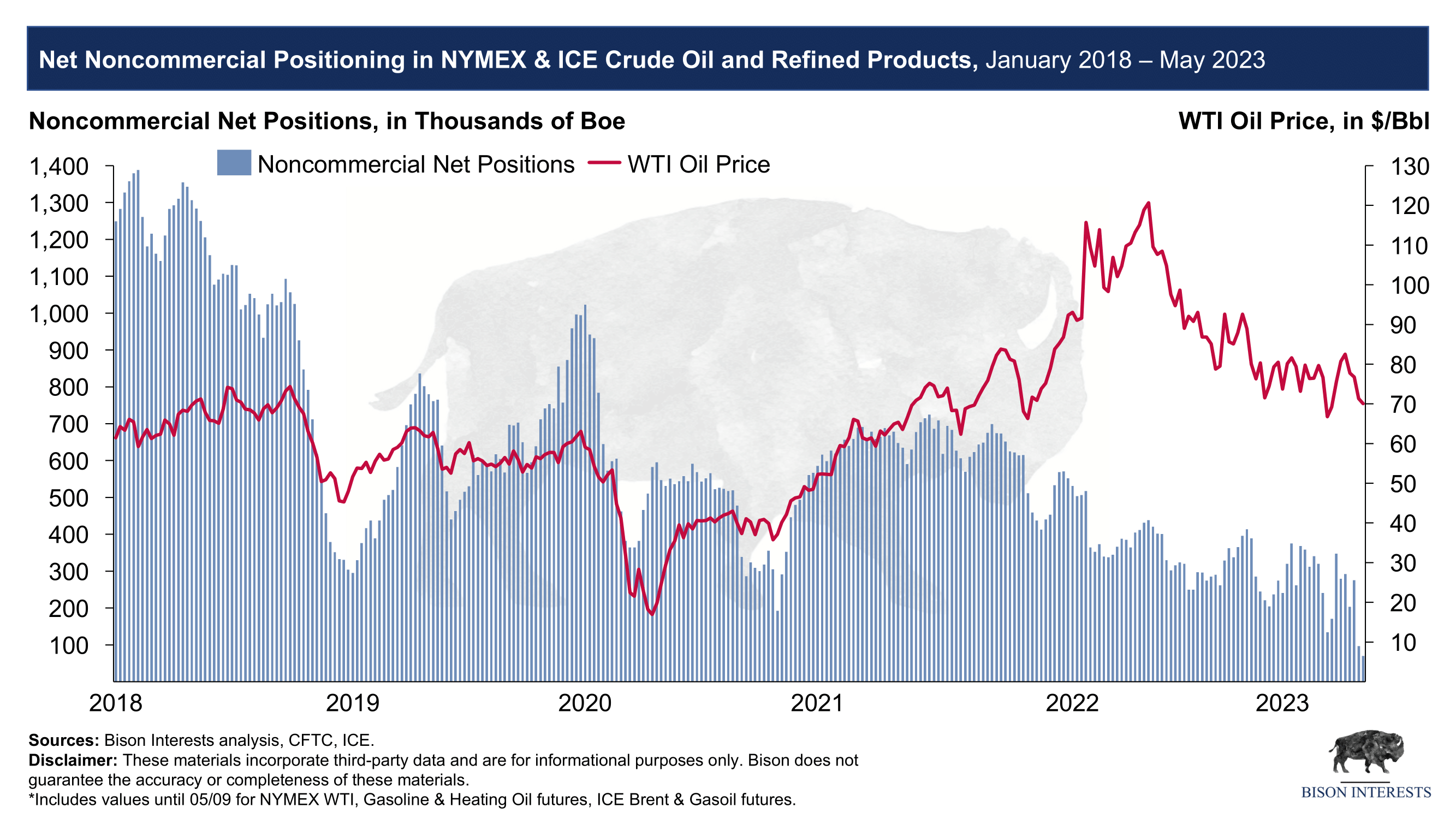

Declining Speculative Interest May Portend A Reversal

Hedge funds and other “non-commercial” entities that speculate on oil prices in the futures markets are close to being net short oil futures, which did not even come close to happening during the depths of Covid. Speculative net interest in oil and refined products on both the NYMEX and ICE has now reached historic lows:

Declining Speculative Interest May Portend A Reversal

Sentiment among investors has gotten so negative that they have flooded the market with 249MM paper barrels since mid-April [1]. This was one of the most rapid net position liquidations ever, and in consideration of this massive build in paper barrels, oil prices have held up surprisingly well.

Declining speculative interest in oil futures is indicative of negative sentiment amongst investors and speculators but is not necessarily reflective of oil market realities. In this instance, “paper” oil futures appear disconnected from physical oil markets, which are currently very tight—as indicated by rapidly declining inventories, addressed below. Eventually, physical market dynamics will determine the trajectory of oil prices, as “paper” oil will need to be matched by physical supply, especially if sentiment rebounds and net positioning improves.

Energy & Recessions

The prevailing narrative lacks nuance: “if there’s a recession, oil demand will drop materially, the world will be oversupplied, and prices will fall.” Not only do we disagree with this perspective from fundamental standpoint, which we address below, but it is worth considering that energy equities historically have performed well up until a recession:

As can be seen above, even if we are nearing a recession, oil prices and related equities might do quite well first, as they have in past cycles. The implications are two-fold: 1) those that are bearish on the broader economy shouldn’t necessarily be bearish on oil and associated equities, and 2) even if a recession is looming, it may not come for some time, considering energy underperformance to date.

Easy Money Policy May Jolt Oil Prices Higher

The financial system is already buckling under the pressure of higher interest rates, as evidenced by the recent collapse of several regional banks. At the same time, white-hot inflation we saw last year appears to be rolling over, at least for now:

These two factors may provide the necessary cover for the Federal Reserve to pause raising interest rates, and eventually start lowering them, which it has been under pressure to do for some time now. Considering these factors, the most recent federal funds rate increase may have been one of the last in the recent series of aggressive rate hikes.

As the Federal Reserve moves towards looser monetary policy, it is worth considering that prior periods like these have coincided with higher oil prices:

Global Demand is Still Running Hot

It is helpful to remember that oil demand is on a steady, rising trajectory, despite the shorter term oriented prevailing narratives found in news headlines:

Source: IEA

As can be seen in the above chart from the IEA, global oil demand has historically grown predictably by about 1% and is already rapidly reverting to its pre-covid trajectory. That longer term demand trend is not likely to subside any time soon, with most of the world’s future oil demand likely to come from highly populated developing countries that make up a large and increasing share of the global population. As these developing countries see increased per capita GDP, their populations increase their standard of living, which begets higher energy consumption:

US Freight Recession Already Impacting Demand

In the last recession of 2008-2009, oil demand was down 1.6%. And in 2020, right after the world had come to a standstill due to covid lockdown, oil demand only fell by 9.3% and nearly fully recovered by the following summer [2]. The implication is that even in the face of a potential recession oil demand may be more resilient than consensus expectations.

While analysts ponder the risk of a broader recession that could negatively impact oil demand, it is easy to miss that a shipping and trucking recession is already underway. This recent slump in freight demand has put pressure on diesel demand, an oil product:

Transportation activity is a key indicator used in predicting and evaluating economic downturns. Considering the decline in freight activity for nearly a year now it is possible that we’re nearing the end of that aspect of the recession, and the oil demand weakness that has been prominently featured in oil market headlines and forecasts.

Oil and diesel appear to already be pricing in this massive decline in freight activity. While it is difficult to tell when freight demand will stabilize and recover, recent improvements in US retail sales data are promising while recession expectations are peaking:

Oil Supply is Disappointing

Against a backdrop of steadily rising demand, supply continues to disappoint. In the U.S shale is likely to continue delivering some growth, although it may be lower than consensus expectations of around 0.6 MM bbl/d[3]. Shale oil well productivity gains have peaked, and the trend to drilling longer laterals on less prospective land is increasing production decline rates and threatening supply stability. This is driving up the cost of production and reducing a potential source of incremental oil supply.

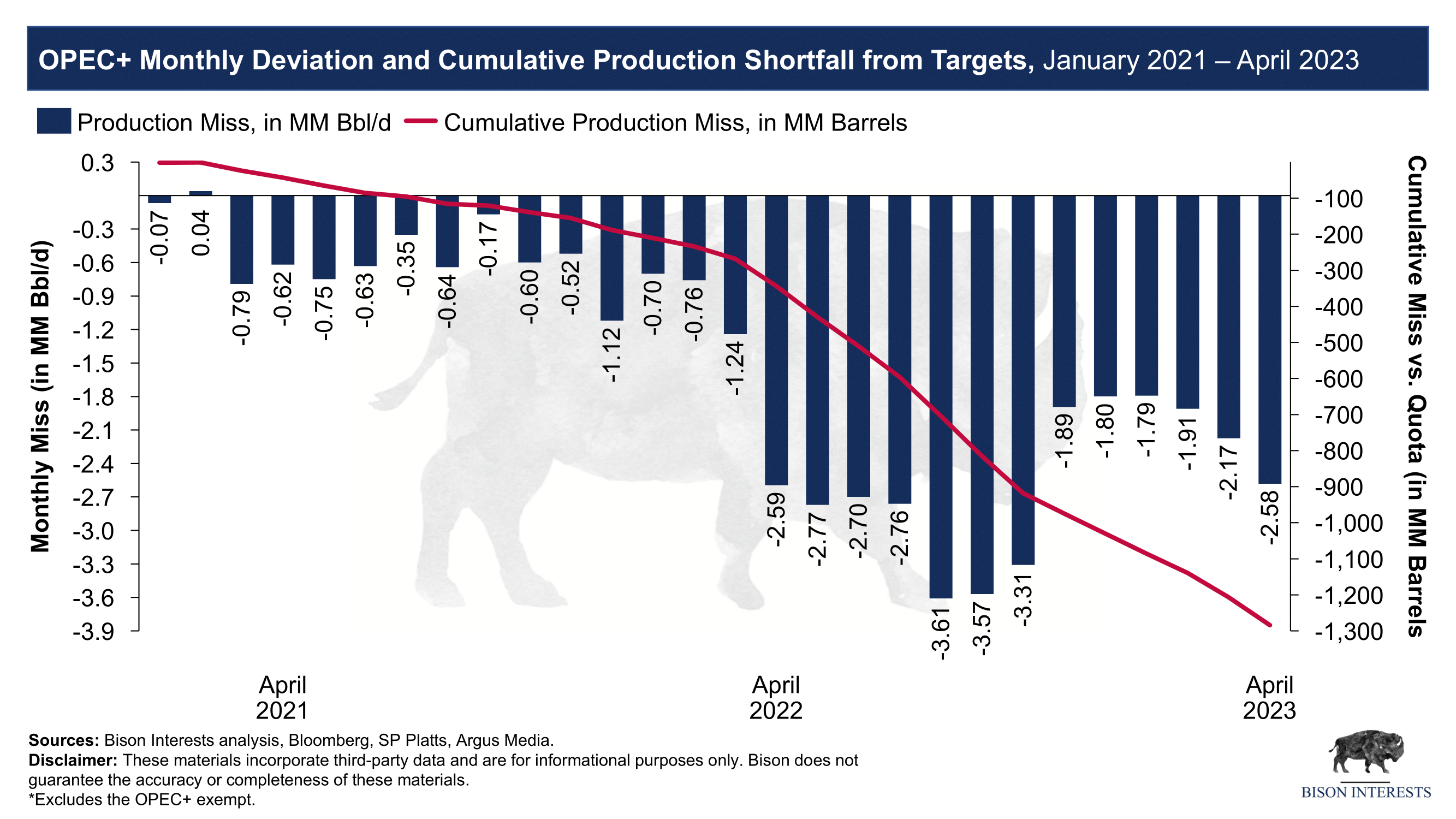

On the OPEC+ front, production has been below quota levels and expectations for some time now, validating our spare capacity analysis:

OPEC+ announced in April that it was voluntarily cutting oil production by 1.66MM bbl/d, including a 0.5MM bbl/d production cut from Russia. Despite concerns of lack of follow through on this cut, data is showing that OPEC+ exports are down roughly in line with their announced production cuts so far.

It is worth noting that not only has OPEC+ been missing versus self-imposed production targets, but their total level of output has also been declining. The implications of declining OPEC+ production are profound, as the market may be undersupplied later this year by as much as 4.6MM bbl/d from pre-cut expectations:

As a result of supply disappointments in both OPEC+ and non-OPEC countries, global onshore oil inventories are being rapidly depleted, even prior to these OPEC+ cuts:

Inventory levels are among the most important metrics to monitor in the oil market, as these reflect shifting physical market supply/demand dynamics that ultimately play into the physical clearing price for oil, beyond the gyrations of the oil futures markets.

Historically, rapid oil inventory draws have been correlated with higher oil prices and rapid oil inventory builds with periods of lower oil prices, but not necessarily in that order. With oil inventories that built in late 2022 now rapidly being depleted to meet production shortfalls, the global oil and refined products inventory picture is promising.

The Big Picture: Oil Market Deficit in Late 2023

As a result of tepid global oil production growth and stronger than expected demand, the world is likely to shift from slight oversupply in 2022 to meaningful undersupply in the second half of 2023:

News headlines and the market price action remain fixated on a potential recession and negative implications for oil prices, while the underlying physical oil market fundamentals are rapidly improving. As world oil markets move into a deep deficit, any potential demand destruction from a recession may be fully offset by lower supply.

Opportunities in Oil & Gas Equities

Pervasive negative sentiment for oil and gas investments presents an opportunity with select oil producer equities at exceptionally low valuations. Ironically, the fundamental picture for many of these equities have improved despite declines in their share prices. Specifically, while fear driven selling of oil and gas equities has forced share prices lower balance sheets have improved, and cost structures have been rationalized.

The result is some small cap equities trading at less than 2 times forward EBITDA, while generating enormous free cash flow at current suppressed prices:

These low valuations present an opportunity to invest at a discount, with upside from reversion to historical averages. There is even more upside from rapidly improving fundamentals, as the companies pay down debt, minimize capex and improve operations.

With that said, oil equities are not simply a directional bet on oil prices. Many are highly profitable in the current price environment and have other catalysts that may lead to re-valuation. Notably, there is an oil & gas industry M&A boom that is already underway. Despite the material volatility associated to rapid shifts in investor sentiment and recent price declines, the fundamentals are compelling.

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice.

Great overview. You, Nuttall, Kuppy, Tony Greer, and J Polomny are my go to guys on this area of the market. Thanks for the fantastic summary.

"Hedge funds and other “non-commercial” entities that speculate on oil prices in the futures markets are close to being net short oil futures, which did not even come close to happening during the depths of Covid."

Considering the strength of the fundamentals, wouldn't the above scenario increase the risk of short squeeze in the second half of 2023?