Small-Cap E&Ps: Compelling Opportunity

Small-Cap E&Ps: Compelling Opportunity

(Important Disclaimer at the Bottom)

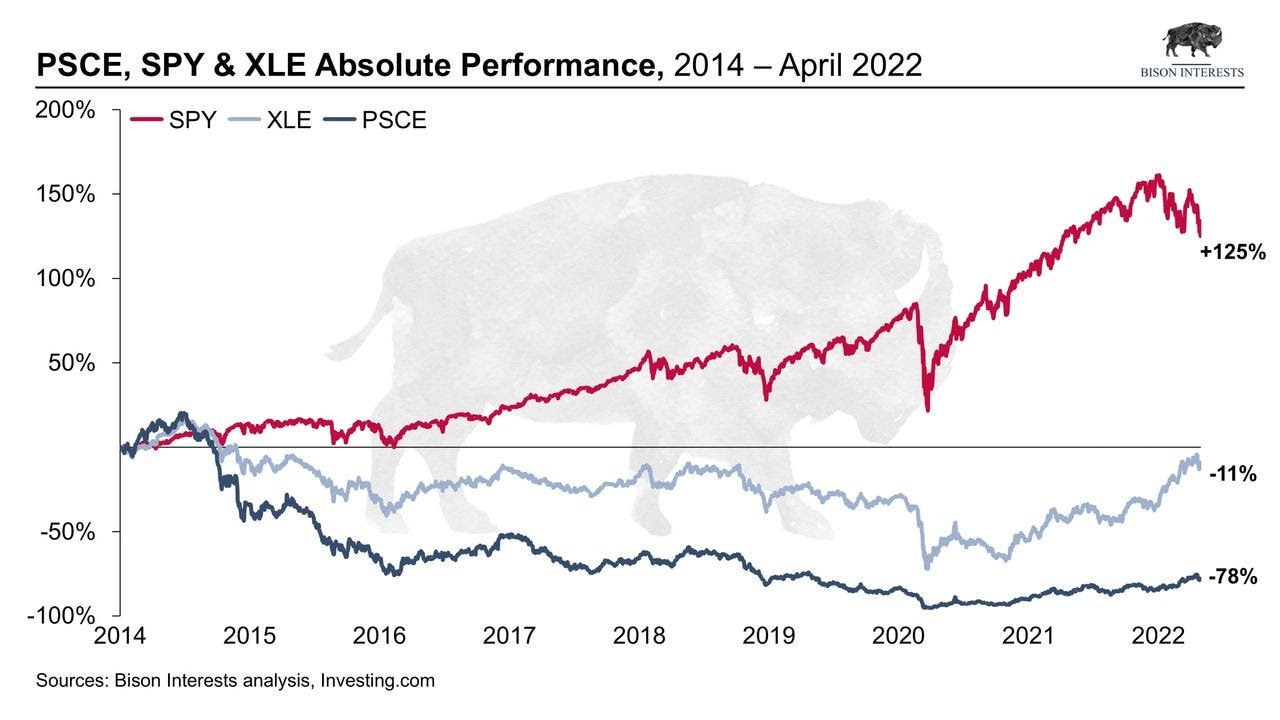

In the Golden Age of Oil and Gas Producers, one group stands out as particularly attractive for prospective investment: small cap oil and gas producers (E&Ps). Share prices for small cap E&Ps have been hit particularly hard since the last oil bull market in 2014, despite improving fundamentals in line with their large cap counterparts:

As can be seen above and despite a similar oil price today as in 2014, share prices for small cap E&P’s (PSCE), have materially lagged both the large cap oil and gas equity index (XLE), as well as the broader market. While the late 2021/2022 bull market in oil equities was well reflected in XLE, PSCE's performance lagged in this time frame. As such, small cap oil and gas equity performance has the potential to catch up to both large cap equities and the broader market, and small cap E&P’s may outperform across various market conditions.

Small cap E&P equity under-performance has been exacerbated by multiple compression, despite improved fundamentals. In our previous white paper, The Golden Age of Oil and Gas Producers, we demonstrated that E&Ps are—on aggregate—better businesses as compared to during their previous cycle highs in 2014. E&P's are benefitting from structural cost reductions and increased capital efficiency, resulting in better margins in a similar oil price regime. And while these companies have substantially outperformed the broader market recently, profits have increased faster than share prices. As a result of uneconomic divestment from the industry, multiples have compressed compared to previous cycle highs, despite improved fundamentals:

As the oil bull market continues, small cap oil and gas equity multiples are increasingly likely to revert to their long-term average levels. Because these are further away from their historical average valuations than their larger cap counterparts, they have more upside performance potential. This is supported by fundamentals: small caps have, on average, a higher cost of production per barrel than large caps, implying greater torque to higher prices. In a rising commodity price environment, small caps undergo faster free cash flow growth than large caps, and assuming constant cash flow multiples, share prices should appreciate faster. This is likely a conservative assumption, as investors have traditionally assigned a premium multiple to faster growing businesses.

Small cap equities offer protection in a bear market as well. With WTI at $110/bbl and natural gas above $7.5/MMBtu, many of these companies are experiencing prices well over their cost of production. Should oil and gas prices fall materially from here, which we believe is unlikely over the medium term given the strong macroeconomic landscape, these companies would likely remain profitable. In fact, after several quarters of substantial cash flow generation coupled with limited capital expenditures, many smaller E&P’s have historically low or rapidly falling levels of debt, and significant cash balances, which could act as a buffer should commodity prices fall materially.

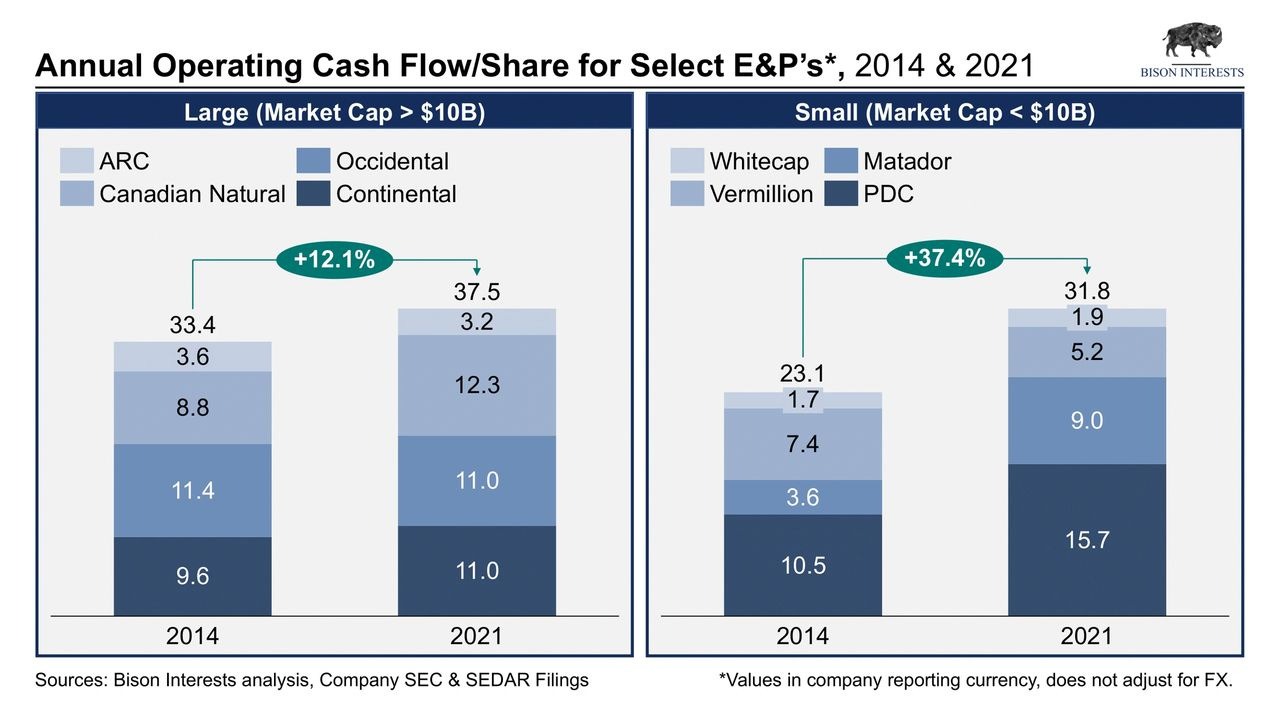

The markedly lower valuation multiples and material underperformance of small cap equities vs. large since 2014 are inconsistent with fundamentals, as indicated by the trajectory of their cash flow, adjusted for share count, over the same period:

The above chart was made using a basket of Canadian and US small and large cap E&Ps. While this is a small sample set, it does give an indication of the direction of cash flow over this period. And because average oil prices were higher in 2014 than 2021, but are now in line with current prices, this may understate improvements in profitability. Therefore, small cap equities have seen profitability improvements in line with their larger counterparts, and thus significantly lower valuations are unwarranted. If small cap E&P equities were to trade in line with their larger cap peers, this would imply significant share price appreciation for many of the equities.

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.