The Glut is Over: Waha Hub Natural Gas

The Glut is Over: Waha Hub Natural Gas

(Important Disclaimer at Bottom)

The Glut is Over: Waha Hub Natural Gas Supply Falls Below Pipeline Capacity; Deficit May Continue for Years

Importance and Relevance:

Waha Hub gas supply has swung from a years-long glut to a deficit that may persist.

This has implications for midstream gathering, processing, and transportation companies, oil and gas producers, and the broader North American market for natural gas, including chemicals, utilities, and LNG exporters.

This shift is poorly understood and may not be fully factored into valuations of assets or companies.

Associated Natural Gas from Shale Oil in the Permian

The Waha Hub is a natural gas supply hub located at the crossroads of the Permian producing region in West Texas and Southeast New Mexico. The majority of the natural gas produced in the region is “associated gas,” the byproduct of oil-focused drilling operations in the Permian. Permian producers have been less focused on gas economics due to the prolific oil production from wells in the region. Improvements in technologies and efficiencies spurred an area production boom over the past decade. This boom brought with it rapid Permian natural gas production growth, even though the local gas price has sometimes been near or below zero.

Gross natural gas production in the Permian more than doubled between 2014 and 2020. In March 2014, production averaged 5.4 billion cubic feet per day(Bcf/d). This number rose to 13 Bcf/d in January 2020. This rapid increase in production resulted in a transportation bottleneck because takeaway capacity—i.e., the ability to transport oil and gas out of the region via pipelines, trucks, and rails—could not keep up with production. This bottleneck has widened over the past few years as continued oversupply and attractive economics brought major pipeline construction and capacity additions to the Permian. Today, expectations of future production drop due to COVID-19 while major pipelines begin commercial operation. Accordingly, new Permian fundamentals have ushered in an era of more competitive Waha Hub prices.

Henry Hub Natural Gas Basis

Henry Hub is a natural gas distribution hub and pipeline system in Louisiana that connects nine interstate and four intrastate systems. The natural gas price at Henry Hub, also known as the basis price, is the benchmark for natural gas prices in the United States. The difference between the natural gas price at Henry Hub and the natural gas price at a delivery point elsewhere in the country is known as the natural gas basis differential.

The widening or narrowing of natural gas basis differentials between regional natural gas hubs and Henry Hub (i.e., the basis) is often an indicator of changing market dynamics. The basis narrowed at many trading hubs in the first half of 2020 relative to the first half of 2019. The basis at key demand hubs (which are generally near population centers) narrowed primarily because of weather-related factors, and the basis at some supply hubs (which are generally near production areas) narrowed because of decreases in natural gas production. Declines in economic activity related to COVID-19 and associated mitigation efforts further narrowed the basis at both demand and supply hubs.

Waha Hub Natural Gas Basis Differential

Historically, Waha Hub has traded at a discount to Henry Hub. The explanationfrom the U.S. Energy Information Administration (“EIA”) for this discount involves the overproduction of natural gas in the Permian and resulting dearth in takeaway capacity in the last decade. As shown in the chart below, during periods of increased Permian production, the natural gas basis differential between these hubs widens.

Throughout 2019 the natural gas basis differential at Waha Hub was wide, reaching nearly $3.00/MMBtu lower than Henry Hub prices in April 2019. In the first half of 2020, the basis narrowed as a result of low crude oil prices and reduced associated natural gas production in the Permian Basin. Additional pipeline takeaway capacity completed in the past year has also helped support higher prices at Waha, further narrowing the natural gas basis differential.

Post-COVID Natural Gas Supply and Demand Outlook

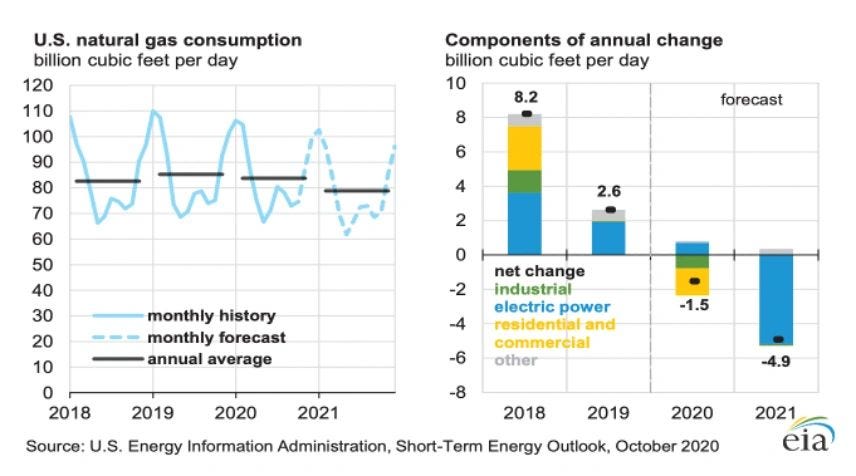

The EIA forecasts that U.S. dry natural gas production will decrease 3.67% from 89.9 Bcf/d in 2020 to 86.6 Bcf/d in 2021. Monthly average U.S. gas production is expected to fall from a record 96.2 Bcf/d in November 2019 to 85.5 Bcf/d in February 2021 and begin to rise in the second quarter of 2021 in response to higher natural gas and crude oil prices.

The EIA also forecasts that U.S. natural gas consumption will average 82.7 Bcf/d in 2020 (a 2.7% decline from 2019) and 79.1 Bcf/d in 2021 (a 4.3% decline from 2020). This forecast is based on the expectation that rising natural gas prices that reduce demand for natural gas in the electric power sector and reduced manufacturing activity will reduce consumption in the industrial sector.

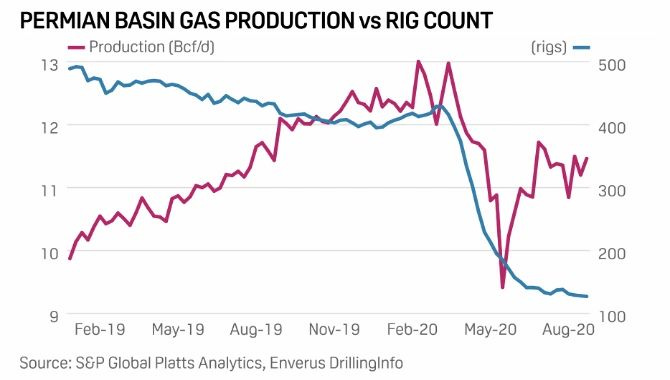

Permian natural gas production averaged 10.45 Bcf/d in August 2020. While the EIA doesn’t provide specific forecast numbers for gas production in the Permian, the EIA expects that relative to production in other U.S. regions, Permian production will decline the most in the short term. The EIA points to low crude oil prices and reduced associated natural gas output from oil-directed rigs. This is supported by the chart below that depicts the relationship between Permian basin gas production and rig count: the sharp decrease in the number of oil rigs since March is correlated with reduced natural gas production in the Permian.

In the search for post-COVID forecasts, we came across a Permian natural gas production outlook from Rystad Energy. Rystad forecasts production falling from 13 Bcf/d in 2020 to 11 Bcf/d in June 2021. Rystad also forecasts gas production surpassing 14 Bcf/d in the first quarter of 2022 and 16 Bcf/d in the first quarter of 2023 (assuming $45 WTI in 2020 and $50 in 2021 to 2023). While industry sentiment ubiquitously acknowledges that the pandemic has set back production, a recently released RBN Energy report along with comments from an industry executive we interviewed lead us to believe that Rystad’s production outlook is optimistic.

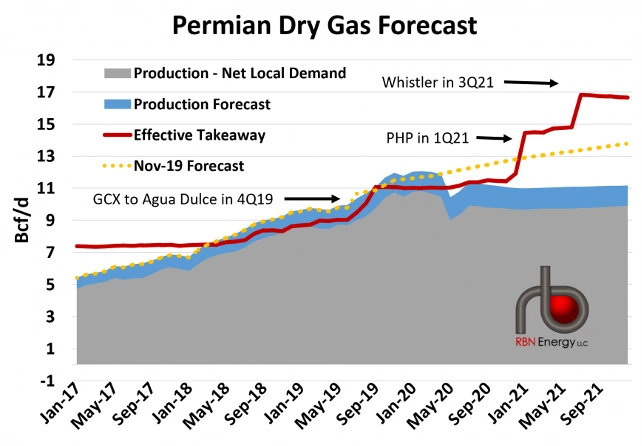

Finally, Sufficient Takeaway Capacity: Available Transportation and Upcoming Projects

The chart below from RBN Energy visualizes historic and forecasted Permian natural gas supply and capacity through 2021. After years of oversupply, Permian natural gas production and capacity reached an equilibrium in September 2020. RBN’s view is that current takeaway capacity is 11–13 Bcf/d depending on outages and that there is an additional 4.1 Bcf/d of capacity coming online next year. This aligns with EIA statements and other industry reports. With production currently at 10.45 Bcf/d and expected to remain flat through 2021, we are entering an era where the Permian has ample (and possibly even excess) gas pipeline capacity.

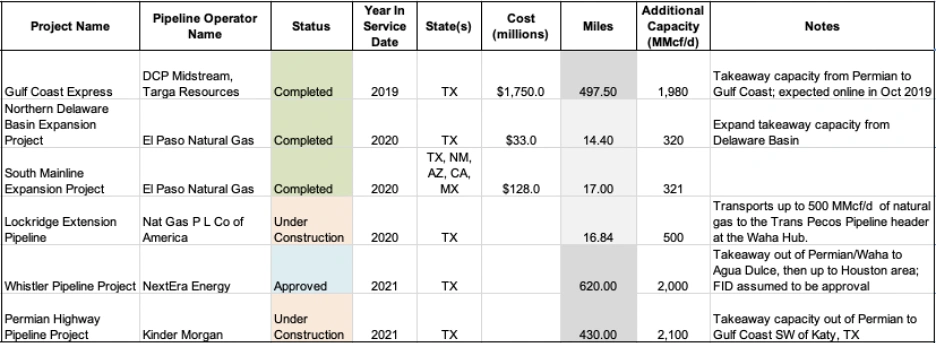

As of September 2020, the Permian Highway Pipeline (“PHP”) project and the Whistler project are the two remaining pipeline construction projects moving ahead with in-service dates of the first quarter of 2021 and the third quarter of 2021, respectively. The Whistler project is a pipeline that will run from the Waha Header, Coyanosa to Agua Dulce, Texas. The PHP project is Kinder Morgan’s 430 mile, 42” pipeline that will run from Waha Hub to Katy, Texas. These two pipeline projects will add 4.1 Bcf/d of takeaway capacity out of Waha Hub, and this is expected to ease constraint concerns for years.

Outbound takeaway pipeline capacity will reach 17.5 Bcf/d in 2022 upon completion of the Whistler and PHP projects. Rystad Energy suggests this is enough to accommodate the increasing gas production in the Permian through the mid-2020s with Artem Abramov, head of shale research, stating that “in a $45-50 WTI world, there will be a need for new gas takeaway projects from the Permian as early as 2023-2024. [...] If these projects are not approved early enough, the basin might end up with another period of degradation in local differentials and potentially increased gas flaring.”

An Improving Waha Hub Basis

Until early summer 2020, Permian production consistently exceeded pipeline takeaway capacity, and this excess lead to low in-basin prices. However, market fundamentals in the region have since shifted due to the price collapse in oil, a pullback in investment, lower capex by producers, and voluntary shut-ins. As gas production in the region slumped, natural gas prices in the Permian Basin for Cal ‘21 rallied substantially.

source: AEGIS, Bloomberg

Aegis Energy expressed that forward prices “are now consistent with a future where Permian is likely to have ample outbound capacity over the next few years. The Waha discount is very close to the pipeline tariff of $0.45 to send gas from West Texas to the Texas Gulf Coast.” Additionally, S&P Market Intelligence forward basis swaps on futures contracts suggest that the market expects basis prices to be narrow at most hubs through the end of the year. In the third week of September, the price at Waha Hub reached a high of $1.52/MMBtu, which was 54¢/MMBtu lower than the Henry Hub price. The price at the Waha Hub was $1.39/MMBtu, 35¢/MMBtu lower than the Henry Hub price as of September 23, 2020.

Conclusion

Waha Hub’s local natural gas production and pipeline capacity has shifted from surplus to deficit. Prolific associated natural gas production and insufficient pipeline capacity in this region have led to low in-basin prices for years. But now, as COVID-19-related production declines and additional pipeline capacity comes online, we are seeing much stronger in-basin prices and a considerably improved basis differential. Next year, the PHP and Whistler projects are set to add 4.1 Bcf/d of capacity, and we’ll get a chance to see if market fundamentals have attracted an adequate amount of transportation or if the additional capacity will risk the Permian of becoming overpiped.

Key Points

1. Significant changes to Permian natural gas fundamentals have occurred since March 2020’s oil price collapse due to production shut-ins, lower capex by producers, and changing future production expectations. These factors, in addition to new pipeline capacity, have put upward pressure on in-basin prices in recent months.

2. Natural gas production in this region is currently 10.45 Bcf/d, down more than 10% from 2020’s high and the consensus view is that production is to remain flat through June 2021. Beyond this, Rystad Energy has a bullish gas production outlook where the Permian reaches 14 Bcf/d in the first quarter of 2022, and 16 Bcf/d in the first quarter of 2023). However, RBN Energy and an industry executive we interviewed are much less optimistic about the short-to-medium term production in this region.

3. Current takeaway capacity in the Permian is 11–13 Bcf/d, depending on the source and current outages. The remaining major pipelines being constructed in the Permian are expected to increase total takeaway capacity to 17.5 Bcf/d in 2022. The consensus view is that this should accommodate increasing gas production in the basin at least through the next 2–3 years. Rystad Energy expressed that there may be a need for new gas takeaway projects from the Permian as early as 2023–2024 (assuming $45-50 WTI).

4. The Waha Hub natural gas basis differential has improved considerably. With slumping Permian gas production and ample outbound capacity for the next few years, the price differential between Waha Hub and Henry Hub has narrowed substantially, from nearly -$3.00/MMBtu in 2019 to under -$1.00/MMBtu since COVID began. Permian natural gas futures for Cal ‘21 have rallied as well. The current price at Waha Hub is $1.39/MMBtu, 35¢/MMBtu lower than the Henry Hub price as of September 23, 2020.

Variant View

There is a strong likelihood that the Permian will be overpiped to a further extent than previously thought. While takeaway capacity can be reasonably estimated with publicly available information, the current uncertainty in the oil and gas industry makes production forecasts far less certain. Current natural gas production in the Permian has leveled out to 10.5 Bcf/d and lowering rig counts may result in natural gas production growth stopping or even reversing for the first time in years. The consensus on a short-to-medium term outlook for Permian natural gas production is a broad range. While Rystad Energy may be overestimating their Permian production estimates, it can be useful to analyze their stance that pipeline capacity in the Permian will accommodate natural gas production through 2023–2024 even in a high-end production forecast.

This may lead to capacity far exceeding natural gas production through the mid-to-late 2020s. With current takeaway capacity at 11–13 Bcf/d and 17.5 Bcf/d planned to be online by the end of next year, we are in uncharted territory. This could be further exacerbated when factoring in delayed pipeline projects that may resume in a partial economic recovery. This leaves open the possibility of an “overpiped” Permian for the medium-to-long term.

Important Disclaimer:

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

Additional Figures:

Figure 1: Recently Completed & Upcoming Pipeline Projects in the Permian. Source: Bison, EIA

Figure 2: Top 24 Dry Natural Gas Producers in Texas, 2018. Source: Texas RRC

Sources:

Analysis: Sputtering Permian Basin gas production lifts Waha cash, forward prices

Permian gas output will rise, but flaring could increase from 2023 if Covid-19 delays new pipelines

Permian region crude oil prices have increased with additional pipeline takeaway capacity

“In the first half of 2020, about 5 Bcf/d of natural gas pipeline capacity entered service

To Many’s Dismay, Permian Produces More Gas and Condensate Instead of Oil and Profits

Kinder Morgan temporarily halts work on part of Permian Highway

Analysis: Permian supply concerns push SoCal winter gas prices toward record highs

The Permian Basin is getting gassier as wells age and oil output declines

Scrambling For Permian Crude Takeaway Options As Available Pipeline Capacity Vanishes

Permian Oil and Gas Growth Stalls As New Pipes Come Online, Altering Market Dynamics

https://www.rrc.state.tx.us/media/50413/top32producers2018.pdf