The Golden Age of Oil and Gas Producers

The Golden Age of Oil and Gas Producers

(Important Disclaimer at the Bottom)

You may not have heard about this in the news or from your financial advisor, but business has never been better for oil and gas producers. Profits are booming, commodity prices are rising, and growth at any cost has shifted to investor friendly debt paydown, share repurchases, and dividend increases.

It doesn’t hurt that the fundamental outlook for oil and gas remains strong. The confluence of un-economic ESG mandates, which are reducing investment and future supply, years of under-investment in oilfield services, and low levels of oil and DUC inventories has led to structural supply deficits that may not be resolved for years. With rising global demand and a floundering green transition, we may be in the early stages of the next oil super cycle.

Improving fundamentals have renewed interest in oil and gas equities, and a once left-for-dead sector is seeing share prices rising. Yet even with recent outperformance versus the market, oil and gas investments remain extraordinarily attractive. Share prices remain lower than the last time oil and gas prices were at current levels, with potential for significant catch-up to broader market performance:

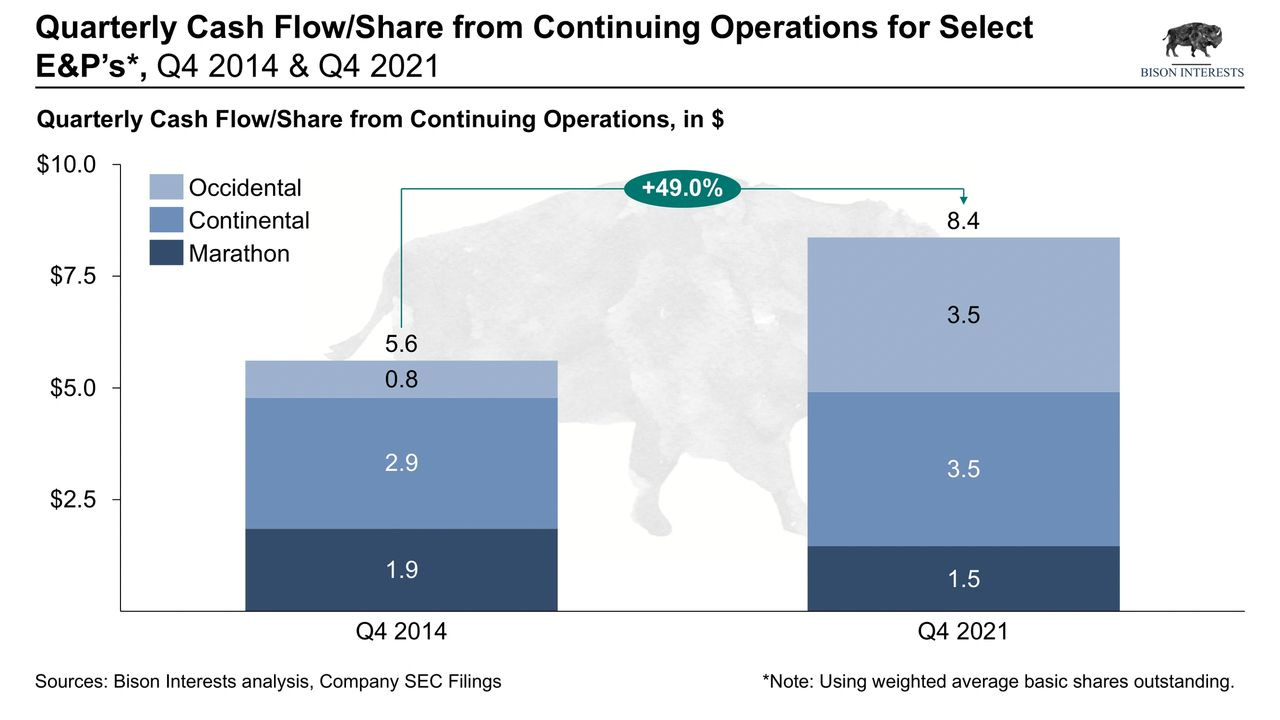

Consistent with this longer-term share performance lag, oil and gas equity valuations have gotten cheaper as increases in share prices have been eclipsed by even larger increases in profits and cash flow. While rising commodity prices have undeniably been a tailwind for E&Ps, their business models and balance sheets have improved markedly since the last cycle high. This is the product of surviving through a challenging financial and operating environment, while shifting focus away from growth at any cost. As such, cash flows for E&Ps have increased materially from levels achieved in 2014, a time with a similar oil price:

Oil and gas producers are more profitable, per share, than they were the last time oil prices were this high. It is likely that these numbers are indicative of broader sector level cash flow improvements. It is the Golden Age for Oil and Gas Producers.

Key Changes Led to Improved Profitability for E&Ps

Since commodity prices were roughly the same in 2014 & 2021, differences in profitability may be attributable to fundamental improvements. Structural costs have been substantially reduced and capital efficiency has improved, despite services cost inflation. Capital is being redirected from 2014 style growth-at-any-cost budgets to 2022 style shareholder returns via debt paydown, buybacks and dividends. And for Canadian companies, the weak local currency is accentuating these factors. These drivers of higher cash flow are discussed below.

Structural Reduction in Costs from Previous Cycle Highs

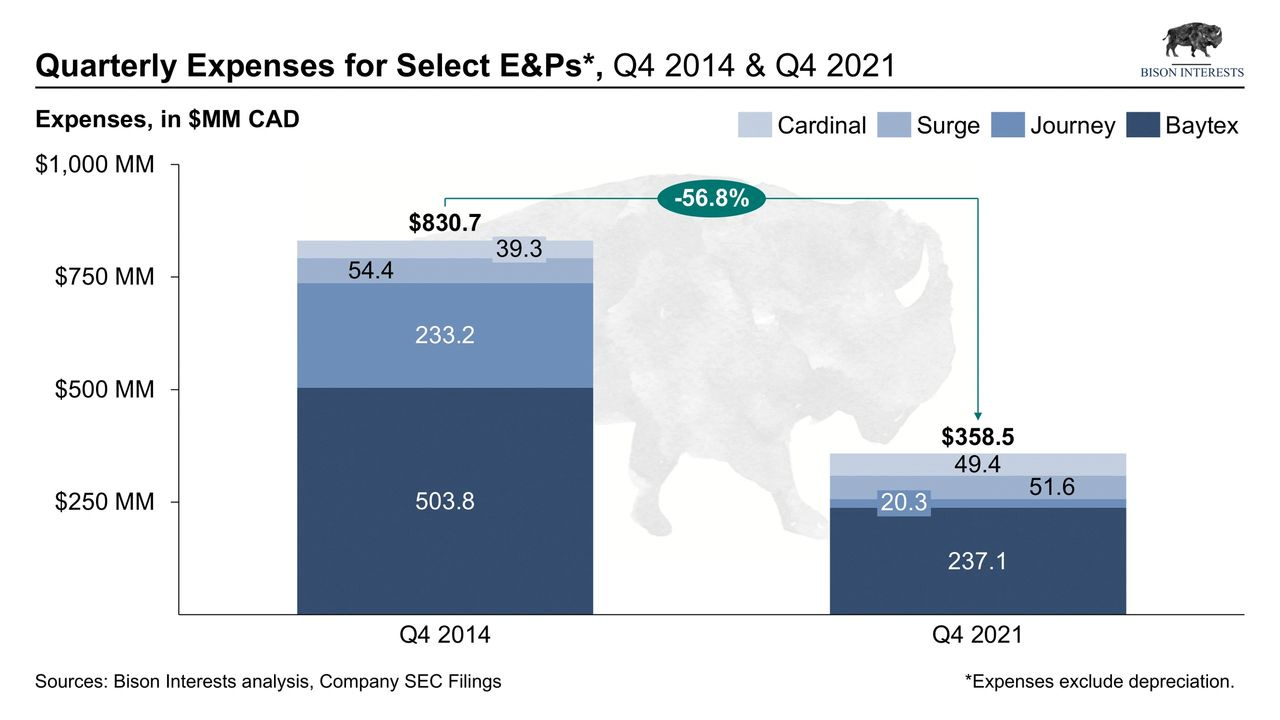

While E&P cash flows have been bolstered by higher oil prices, they have also benefitted from structural fixed cost reductions over the years since the 2014 oil price crash. Examples of these include headcount reductions for administrative roles and the integration of new technologies such as remote monitoring, AI facilitated forecasting and budgeting, etc [1].

Now with leaner cost structures, these businesses have become more survivable in the event of another oil price downturn, while generating more cash flow at higher oil and gas prices. Below is a chart highlighting the change in quarterly expenses, which have been normalized to exclude depreciation and one-time occurrences, of four indicative smaller oil and gas producers in quarters with similar average realized oil:

Capital Efficiency

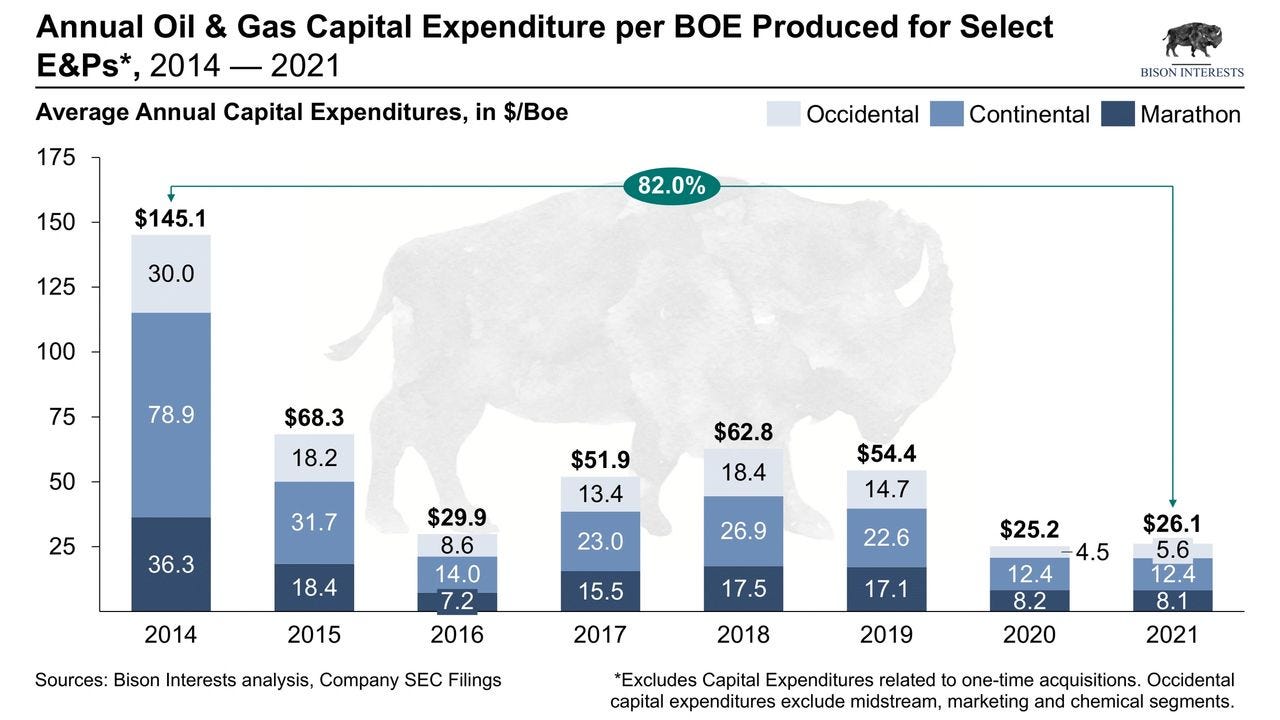

E&P cash flows are also benefitting from increased capital efficiency: current cycle investment is substantially lower, and associated declines in production have been muted. Unlike the deluge of capital spending in the years leading up to the 2014 crash, E&Ps are remaining disciplined as prices rise. While higher commodity prices encourage higher levels of investment, E&Ps have remained focused on minimizing expenditures to return capital to shareholders via buybacks and dividends. Consequently, E&P capital efficiency has improved markedly, as can be seen below:

It is also worth noting that despite lower spending, production has not declined meaningfully, suggesting E&Ps are doing a better job at allocating scarce capital to higher-return projects, while also benefitting from prior investment. And capital expenditure restraint, particularly with regards to new drilling, is self-reinforcing: lower investment today reduces future supply, which perpetuates higher prices.

Additional Upside to Canadian E&Ps: Weak Canadian Dollar

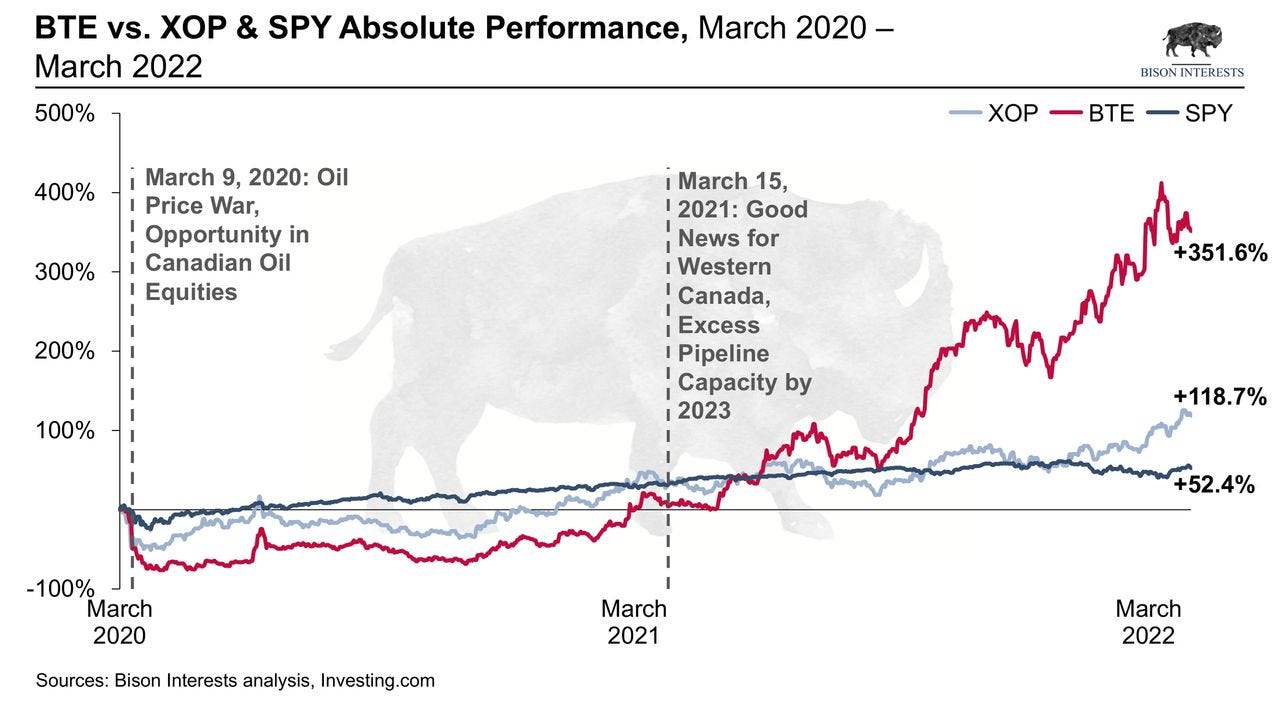

In this new Golden Age for oil and gas producers, Canadian E&P’s shine particularly bright. This is likely no surprise to you, as we pounded the table on Canadian E&P’s in March 2020, and again in March 2021, each time having identified a specific catalyst likely to improve fundamental performance and send share prices higher. Baytex Energy, a portfolio company which was exposed to both catalysts, has outperformed relevant benchmarks during this period:

Foreign exchange effects on revenue are a key driver for higher Canadian producer cash flows: a weaker Canadian dollar (CAD) versus US dollar (USD) denominated commodities increases revenues and margins. This effect is contributing to higher free cash flow, which is helping the companies’ equities outperform, and may continue as the Canadian dollar remains weak.

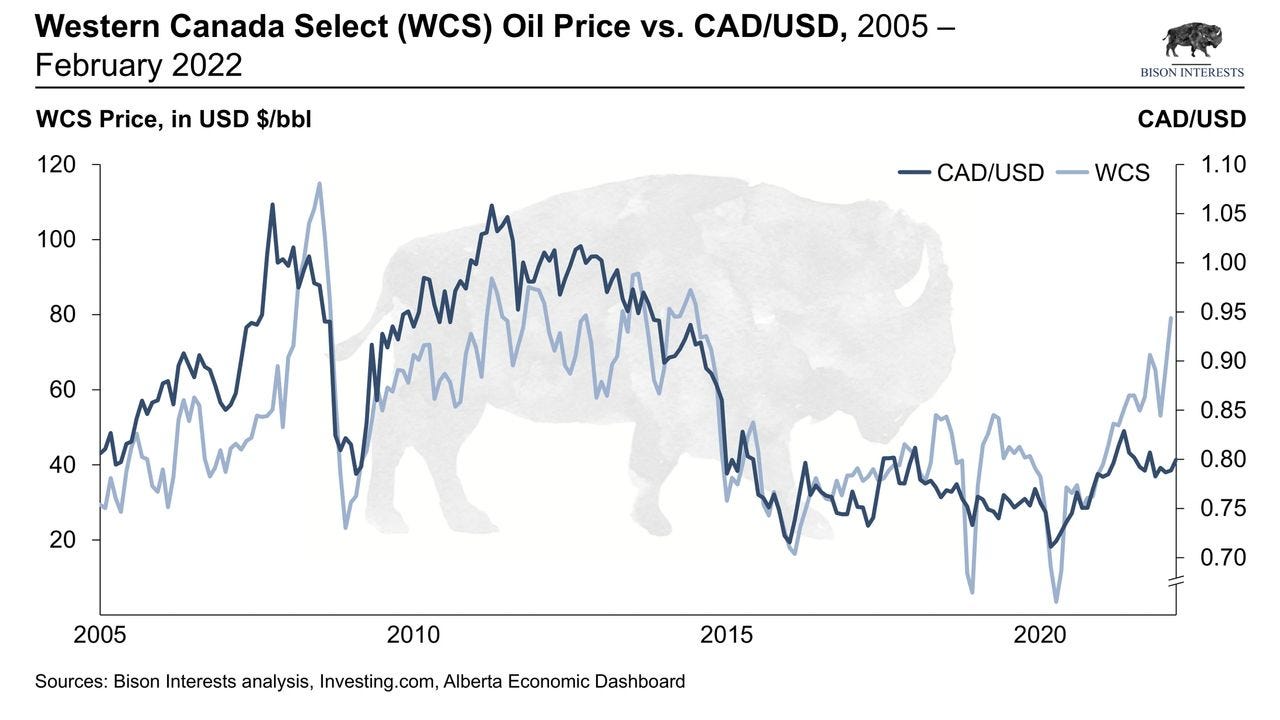

Oil and gas are important to Canada’s economy, having contributed 5% to its GDP on average from 2000 onwards [2]. When oil prices are high, demand for the CAD increases – as more CAD dollars are needed to buy the same quantity of oil - which causes Canada’s current account balance to improve and their currency to strengthen. This effect is magnified because the US is the largest buyer of Canadian oil—comprising 61% of all its imports in 2020—and oil sales make up a large part of Canada’s revenue [3]. Higher oil prices also increase Canadian E&Ps’ cash flow and propensity to invest domestically, which props up the Canadian dollar. Historically, the correlation between oil prices and the CAD/USD has been strong, as can be seen below:

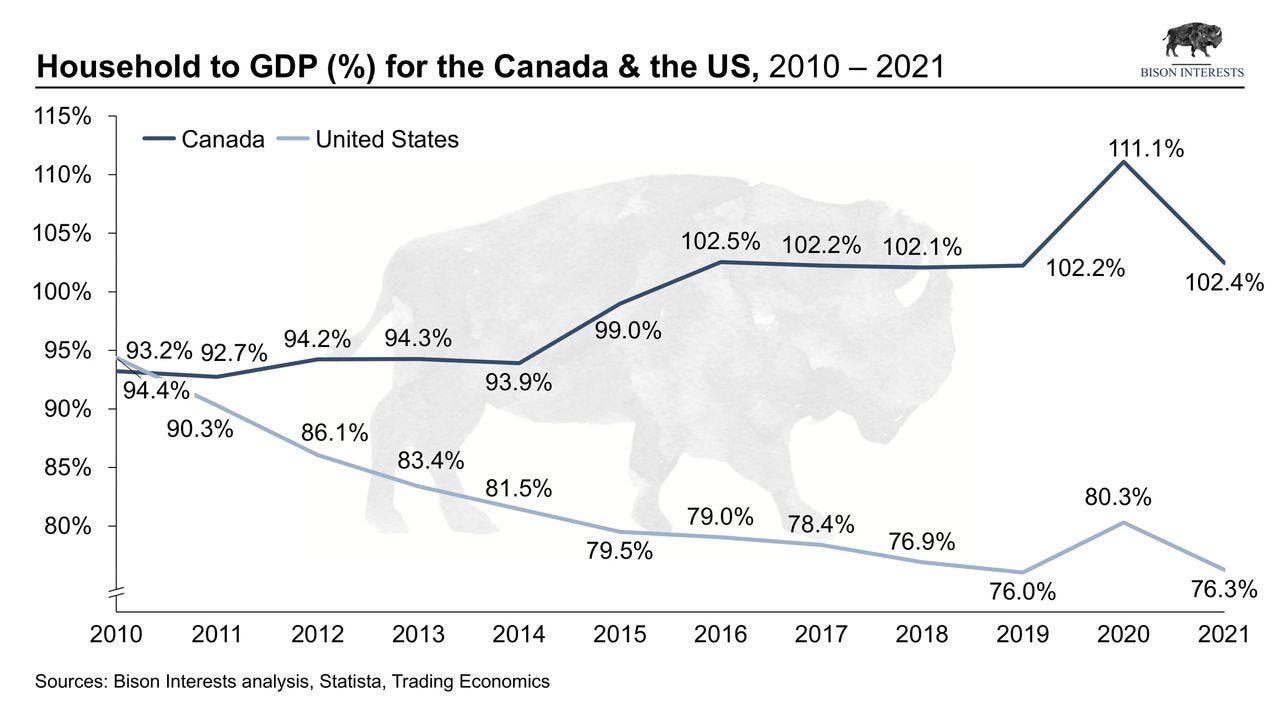

However, the CAD/USD exchange ratio appears to have diverged from their historic correlation with WCS prices following the April 2020 market crash—which may be partially attributable to stricter and longer pandemic measures and lockdowns. Conservative covid policy necessitates liberal monetary and fiscal policy to cushion the associated economic fallout, and so Canada’s monetary base (M0) expanded nearly 260% between March 2020 and January 2022 [4]. This likely strongly devalued the currency and may have overshadowed any strengthening effects from higher oil prices. Other factors, such as large GDP contraction (-5.4%) and high household debt-to-GDP (102% as of 2021) may be weighing down the currency as well [5]:

While a languishing Canadian dollar exacerbates inflation and presents challenges for the Canadian economy, it has also been a tailwind for Canadian E&Ps: Canadian oil producers sell most of their production in USD, but their costs are denominated in CAD. This effect boosts cashflow, as E&Ps revenues benefit from a weaker CAD when USD dollar sales are converted; historically this was not the case as higher oil prices would beget a strengthening CAD, thereby offsetting the FX gain for E&Ps. This cycle, Canadian E&Ps are benefitting from both higher oil prices and a weakening CAD. Few are paying attention to this, and as the divergence between oil prices and the CAD continues, this is likely to bolster E&P cashflows even further.

Estimation of Factor Impact on Cash Flows

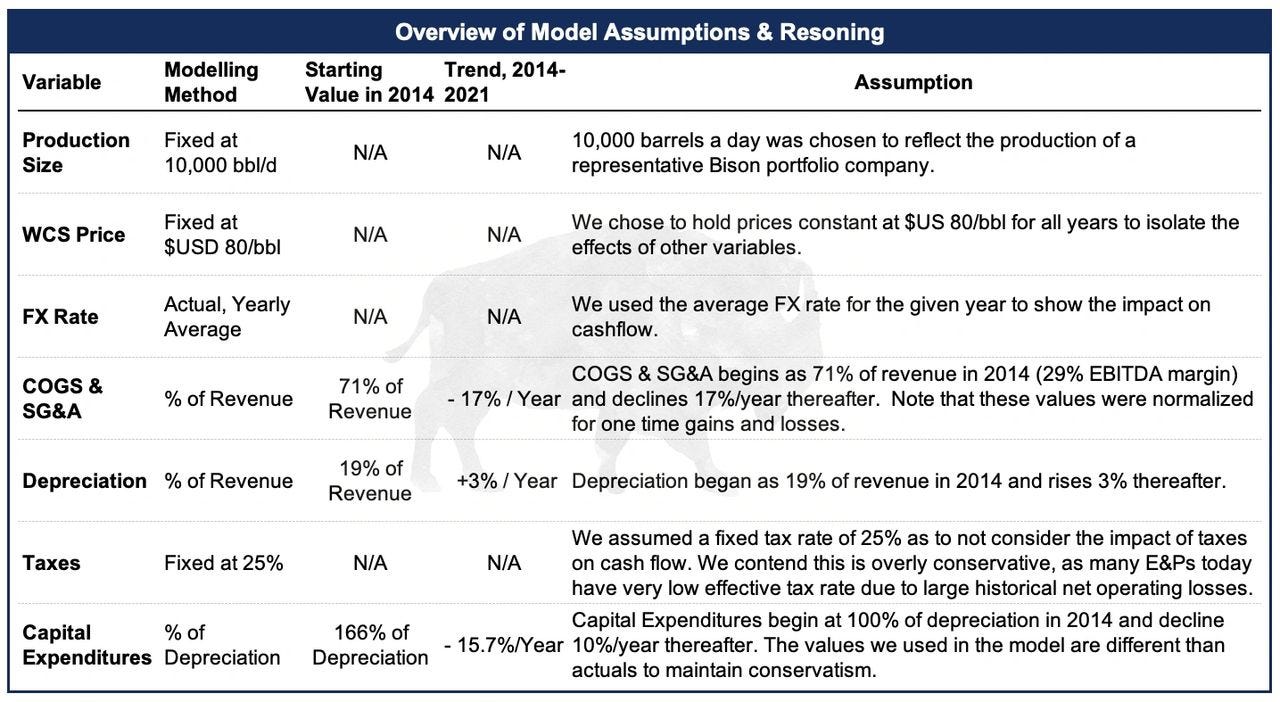

To illustrate these effects of a weaker CAD, and lower costs and capital expenditure for Canadian E&Ps, we modeled the change in cash flow for a hypothetical 10,000 bbl/d oil-only producer between Q4 2014 and Q4 2021. We used empirical data from five similar sized, Canadian producers as a basis for our assumptions of margin changes, depreciation, and capital expenditures in this model [6].

While we acknowledge that this methodology is far from perfect given our small sample size, which does not account for idiosyncratic factors, the purpose of this analysis is to illustrate the directional impact that these factors may have on E&P cash flows, and why these factors have potential to move higher from here even without higher oil prices.

Below a brief overview of our assumptions and reasoning:

Using these assumptions, we observed that the cash flow of a hypothetical 10,000 bbl/d producer, assuming 80$ WCS and actual FX rates, may be at least 3x higher than that of 2014:

As can be seen above, despite the similar commodity pricing environment as in 2014, Canadian E&Ps may generate significantly higher cash flows due to poorly understood currency effects, structural cost reductions and lower capex. For this reason, Canadian E&Ps remain exceptionally cheap and are likely to outperform moving forward, especially as oil prices continue to rise.

Multiple Re-Expansion Could Generate Additional Upside

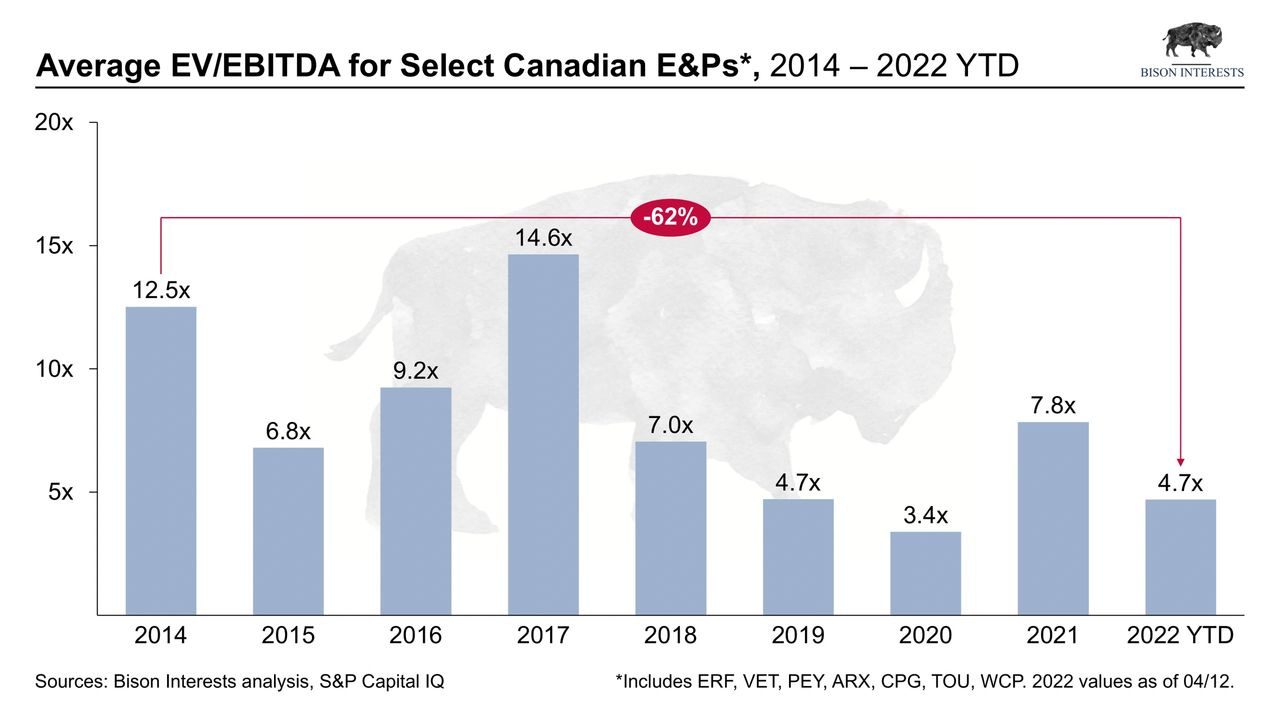

The implications of higher cash flows in a similar commodity price environment due to foreign exchange effects, structural fixed cost reduction and lower capital expenditures are profound for E&Ps, particularly those in Canada. These seem to be overlooked by the market, indicated by E&P EV/EBITDA multiple compression between 2014 and 2021, despite a similar commodity pricing and higher and EBITDA growth:

Bison believes that this phenomenon has occurred largely for non-economic reasons. While some of the historical multiple compression observed can be explained by capital leaving the sector following the 2008 and 2014 price crashes, a likely contributor is the prominent ESG movement, which has artificially restricted the availability of capital and increased the regulatory burden to the industry.

Historically, institutions would pile into high-cash-flow-yielding oil and gas equities, particularly during inflationary periods where the broader market appears to be rolling over. However, self-imposed ESG mandates have driven many institutions and allocators—who would had been the largest investors in this sector—to reduce investments in oil and gas, while some have banned oil and gas investments altogether and/or are actively divesting. The priorities of institutions and their fiduciaries appear to have shifted away from profit maximization as they continue to sell off their best-performing investments, which has driven down oil and gas equity valuations to historic lows:

Despite the ongoing rally in energy equities they remain meaningfully undervalued, and investor interest remains comparatively low to previous cycle highs. As such, there may be substantial upside to oil equities, even if they were only to revert to their mean composition percentage of the index. As oil and gas equity cash flows become too costly to ignore and investors begin to re-prioritize returns over moral posturing, capital continues to trickle back into the industry, potentially reflating valuation multiples. Combined with higher and growing cash flows, this could galvanize a significant re-rate in oil equities, particularly in Canada. And even if institutional capital does not return, continually increasing dividends and equity buybacks could drive strong returns for years to come in the new Golden Age of oil and gas producers

.

Sources

[1] Sources: Offshore Technology & Seven Lake Technologies

[2] Source: Statistics Canada

[3] Source: EIA

[4] Source: Statistics Canada

[5] Sources: Data Commons & Statista

[6] Note: Capital expenditures excluded outliers, and costs were normalized to exclude non-recurring cash costs, impairment and depreciation.

Important Disclaimer: Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.