Sandridge’s Accretive Acquisition Confirms Improved Capital Allocation

Sandridge’s Accretive Acquisition Confirms Improved Capital Allocation

Sandridge Energy (NYSE: SD) recently acquired working interest in 26 wells in the Northwest Stack play producing net 500 boe/d (30% oil). The net effective purchase price for the working interest was $11.25MM, subject to minor closing adjustments, or $22,500/boe/d. This was an accretive acquisition for SandRidge, confirming its improved capital allocation that was recently demonstrated through a dividend and share repurchase program. SandRidge’s acquisition also compares favorably to recent larger, more richly-priced oil and gas deals. More on this below.

SandRidge Acquisition Analysis:

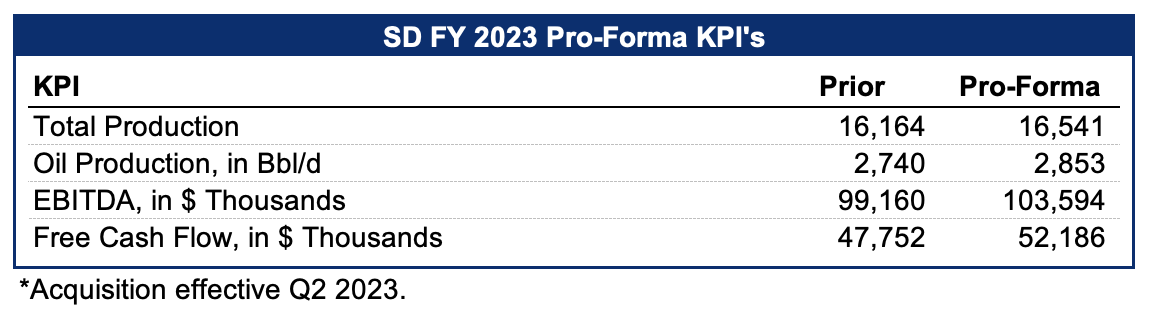

Having only increased its working interest in wells it was already operating, we estimate that Sandridge’s decline profile remains unchanged following this transaction. However, the production added was 30% oil, which is higher than Sandridge’s oil weighting before this deal. Below is a breakdown of the production, cash flow and free cash flow added:

In addition to increasing the oil weighting of SandRidge’s production, this transaction is also highly accretive to their cash flow. Although only effective as of April 1st, we estimate that this deal will add ~$4.4M to FY 2023 free cash flow assuming $75 WTI and $3 Henry Hub gas. The cash flow contribution from this acquisition will be likely be higher in 2024 as Sandridge benefits from a full year of incremental production and potentially higher commodity prices, offset by some production decline. The acquisition looks likely to achieve payback in under 2 years, which is compelling.

Demonstration of Improved Capital Allocation:

While 500 boe/d is only 3% of SandRidge’s pro-forma production, this deal is further confirmation of SandRidge’s improved capital allocation. After two years of building net cash on its balance sheet while maintaining nearly flat production, SandRidge has recently paid out a large special dividend, instituted a small regular dividend, and increased its approved share repurchase program. With this small accretive deal, SandRidge is demonstrating another likely use of free cash flow going forward.

This could mark the beginning of a series of small, highly accretive deals by SandRidge. Many small deals add up, and historically, cost-effective roll-up strategies have done very well in oil & gas bull markets. This is particularly true for roll-ups done at a smaller scale, as smaller deals have historically traded at a discount in M&A markets. And with Sandridge’s large cash balance and tax shield from net operating losses, this type of strategy is certainly worth pursuing and reasonably likely to succeed in creating value.

Looking Ahead for SandRidge:

Though small compared to Sandridge’s expected production of ~16,500 boe/d in 2023, this deal was highly accretive, improving Sandridge’s overall production profile. More importantly, now that Sandridge has entered the M&A market and is returning capital via buybacks and dividends, prior investor concerns regarding capital allocation have been alleviated. With a capital allocation strategy now clearly communicated to investors, and a regular dividend, the discount on Sandridge’s shares associated with uncertain uses of capital may diminish.

Important Disclaimer: Opinions expressed herein by the author, Josh Young, are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises owns shares of Sandridge Energy (NYSE: SD) and may buy or sell shares without any further notice.

Prefer they keep the cash and keep doing the deals

Wouldn't it have made more sense of this acquisition was done elsewhere with higher liquids %?